3D printing is transforming aerospace manufacturing by reducing production time, cutting material waste, and enabling lighter, more efficient aircraft components. Widely adopted across structural, interior, and propulsion systems, the technology is driving innovation, sustainability, and cost optimization, with strong growth projected through 2030.

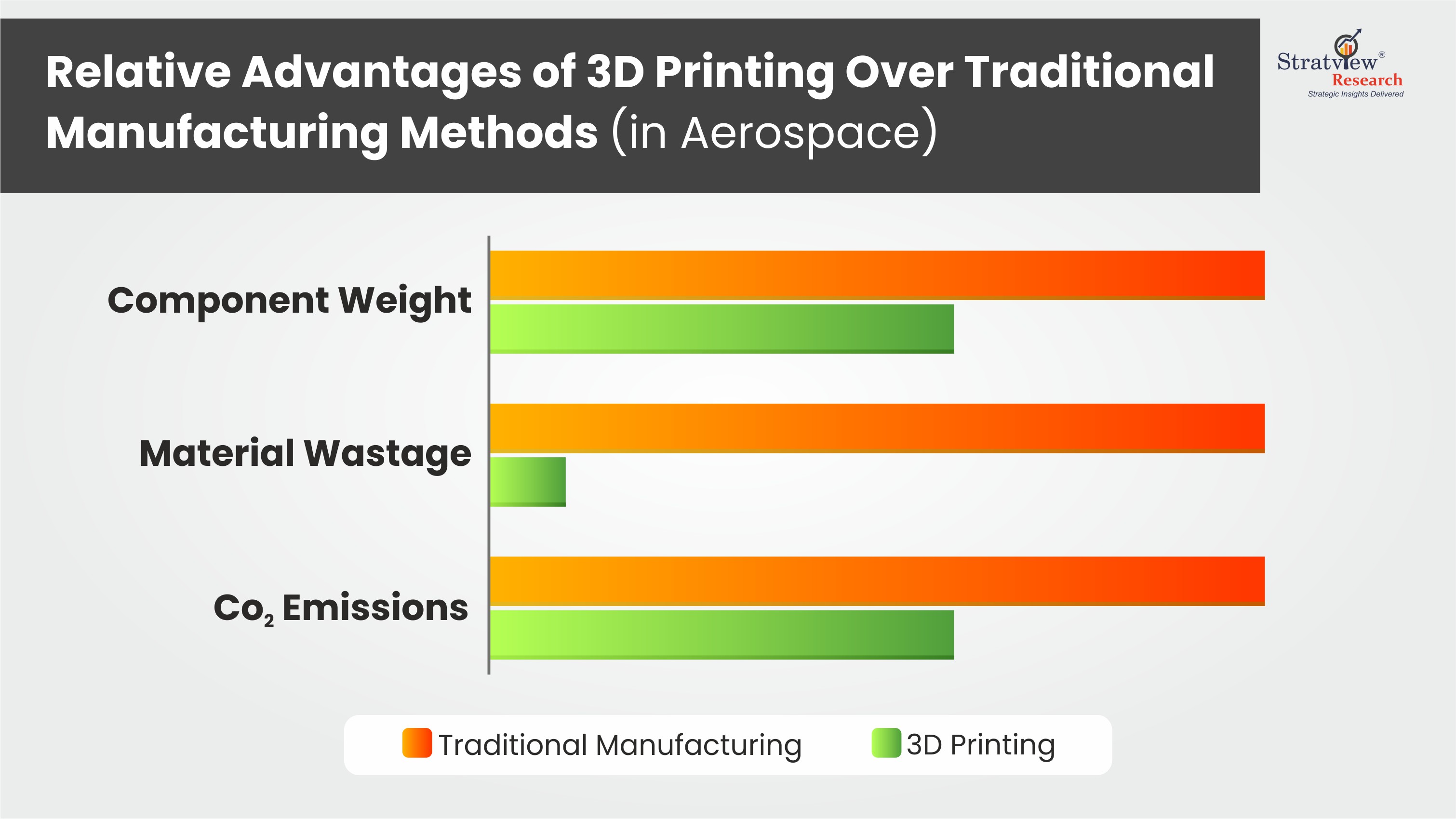

Imagine a technology capable of reducing the production time for aircraft components from 6 months to just a few weeks, offering up to 90% reduction in material waste and 40–50% weight savings. 3D Printing (3DP), as everyone might have already guessed, has indeed been nothing short of a technological miracle for several industries, including aerospace.

Being one of the earliest adopters of 3DP, the aerospace industry was among the first to implement it in high volume and is currently the biggest shareholder of the 3DP market in terms of application (around 15-20%), according to Stratview Research.

3D Printing in Action:

Immediately after its commercial debut in the 1980s, 3DP started finding applications in military aircraft and was also able to build a presence in the commercial aerospace industry within half a decade. The initial applications were majorly limited to testing and prototyping only, until the development of methods like Selective Laser Sintering (SLS) during the late 2000s, which allowed the use of materials like flame retardant resins, thus widening the spectrum of its applications.

Presently, along with its existing penetration in processes like tooling and prototyping, 3DP has also penetrated all major segments of aircraft component manufacturing, including structural, interior, and propulsion. Common applications include engine components, ducts, support brackets, electrical housings, etc.

Employing 3D printing not only reduces the production time and component weight but also offers significant energy savings (reduced CO2 emissions thus) and a reduced number of parts. According to a study conducted by the Embry-Riddle Aeronautical University, employing 3D printing technologies for aerospace component manufacturing offers at least a ~40% reduction in CO2 emissions and energy consumption as compared to traditional methods. A significant impact is made in terms of fuel savings and the achieved lightweight. According to Protolabs Network, manufacturing a single component using 3DP can reduce the lifetime fuel consumption of an aircraft by up to 5%. Luckily, in all modern aircraft, the number of 3D-printed parts is well above just one. Wide-body aircraft like the B787, B777, and variants of the A350 family, all claim to have an average of 500+ 3D-printed parts per aircraft, most of which are used in propulsion systems.

Fig 1. Relative Advantages of 3D Printing Over Traditional Manufacturing in Aerospace

Among the benchmarks that exhibit the heavy usage of 3DP in the aerospace industry is the GE9X engine, which incorporates ~300 3D-printed parts (of which ~80% are engine blades, made of Titanium Alumide), and was designed specifically for B777X jets.

The interest for incorporating 3DP is equally high among OEMs and other nodes in the supply chain and, as of 2024, ~90% of aerospace companies use 3DP, including leading commercial aircraft makers (Airbus, Boeing, Bombardier, and Embraer) and engine suppliers (GE Aviation, Pratt & Whitney, Rolls-Royce, Safran, etc.).tra

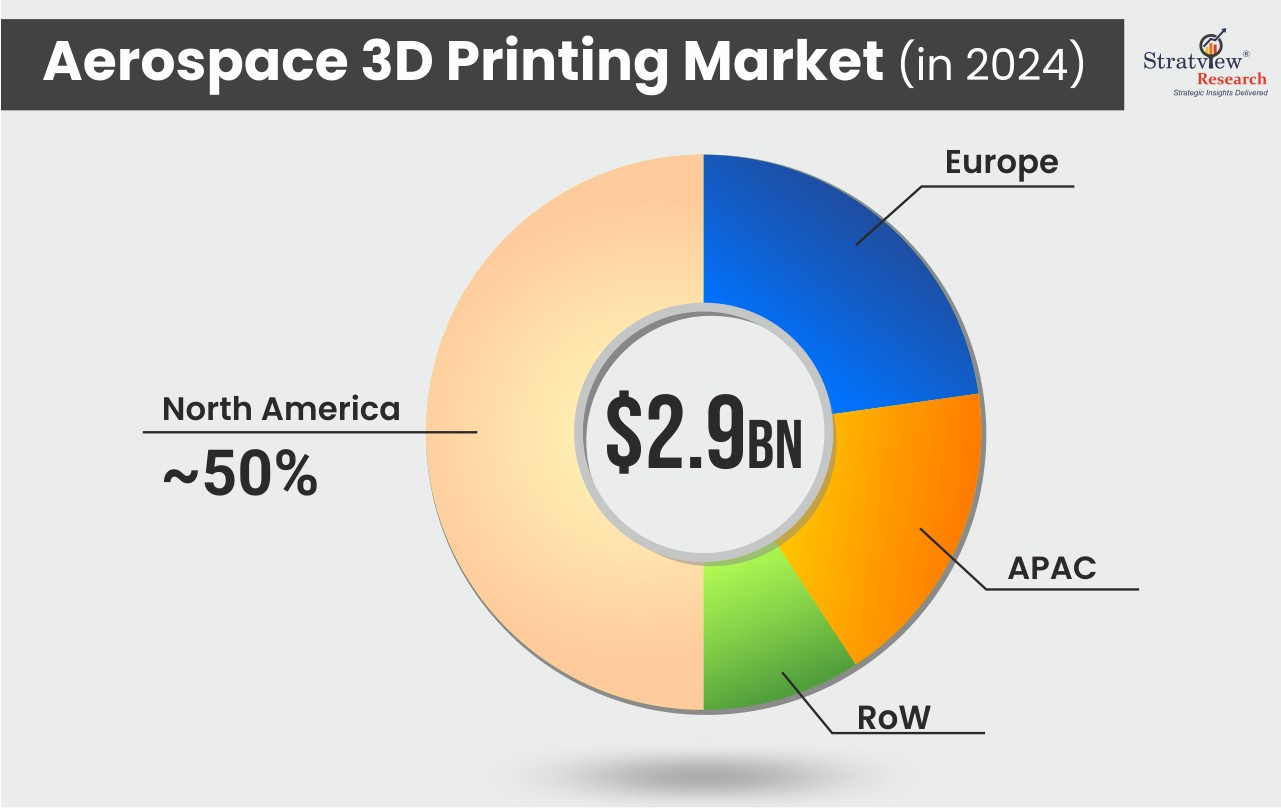

A majority of the above-mentioned players have a presence in both the global aerospace manufacturing hubs, i.e. North America (NA), and Europe. But, driven by the presence of raw material suppliers and a stronger presence of the top 2 aircraft engine manufacturers, i.e. GE Aviation and Pratt & Whitney, the NA region establishes itself as the leader in the aerospace 3DP market, with ~30% share, according to Stratview Research.

While within the NA region, the US remains the undisputed leader; the potential of technologically-advanced neighboring countries like Canada to become a global leader in this space, is also worth a discussion.

North America: Cruising at the Highest Altitude

The dominance of NA in the aerospace 3DP market is expected to be maintained for at least another decade and will be primarily driven by factors like the increasing fleet size (both regional and global), the presence of players having strong experience in 3DP, and the high R&D expenditure for 3DP.

Currently maintaining the largest commercial aircraft fleet, the NA commercial fleet is expected to grow annually at a rate of 1.5% during 2023–43, according to Boeing. This translates to ~8,000 new aircraft deliveries in the next two decades. Globally, an addition of ~44,000 new aircraft is expected by 2043.

While the number of deliveries is higher for the APAC region as compared to NA; growth in the global fleet size will still contribute to NA’s growth in aerospace 3DP because the majority of the demand from the APAC region will be emanating from China and India; none of which have state of the art capabilities in aerospace 3DP and will thus rely on existing expertise only.

China, though a leader in the overall 3DP market globally and well-positioned to be a leader in aircraft manufacturing in the next decade; has not yet indicated extensive use of 3DP in any of its active aircraft programs.

A significant amount of R&D has also been taking place among the US-based players, which can be inferred from the continuous investments and also from the volume of patent applications being received in the 3D printing space. According to Globaldata, during 2021-2023, among the companies involved in aerospace 3DP, the highest volume of 3DP-related patent applications were received from RTX, Raytheon Technologies, and GE Aviation, respectively, all of which are US-based.

Fig 2. Aerospace 3D Printing Market 2024: $2.9 Billion with North America Leading at ~50% Share

Notable investments in capacity expansion are being made frequently, which is also a strong indication of the growing demand in the US.

For instance, in March 2024, GE Aviation announced a $650 million investment to scale its 3D-printed jet engine production and mentioned that ~$550 million from that investment would flow to US facilities and partners.

Then in July 2024, GE Aviation again announced an investment of $1 billion, mentioning that the majority of this investment would be utilized in the development of its benchmark LEAP engines.

Sufficient support is being received by the regulatory authorities as well for the increased adoption of 3DP in aerospace, and, for the past 7-8 years, the FAA and the EASA have been jointly holding workshops every year to educate the concerned supply chain nodes about the standards required for 3D-printed components. Although much work still needs to be done in this area since only a few of available materials have been approved so far for aircraft components.

Path Ahead:

Although revolutionary, 3D printing has notable constraints in producing a complete aircraft. First, mass production through 3D printing does not have the advantage of the cost savings that traditional manufacturing methods provide, resulting in a high cost per part despite larger quantities being produced. Furthermore, only a limited number of 3D printing materials have been approved for use in aerospace, limiting the variety of components that can be securely manufactured. These limitations of 3D printing prevent it from being feasible for full-scale aircraft production. However, due to the increasing adoption of the technology for prototyping and making lightweight & complex individual parts, 3D printing depicts great potential for growth within the aerospace sector. It is expected that the Aerospace 3D Printing market will reach around USD 2.9 billion by 2024 and hit USD 7.2 billion by 2030, growing with a healthy CAGR of around 17% (according to Stratview Research).

Subscribe to our newsletter

Related Articles:

The Blazing Speed of Advancements in 3D Printing of Composites

Didn’t find what you were looking for?

Tell us about your requirements

(Our team usually responds within a few hours)