404

+1-313-307-4176

Aerospace 3D Printing Market | 2026-2034

Aerospace 3D Printing Market Size, Share, Trend, Forecast, Competitive Landscape & Growth Opportunities: 2026-2034

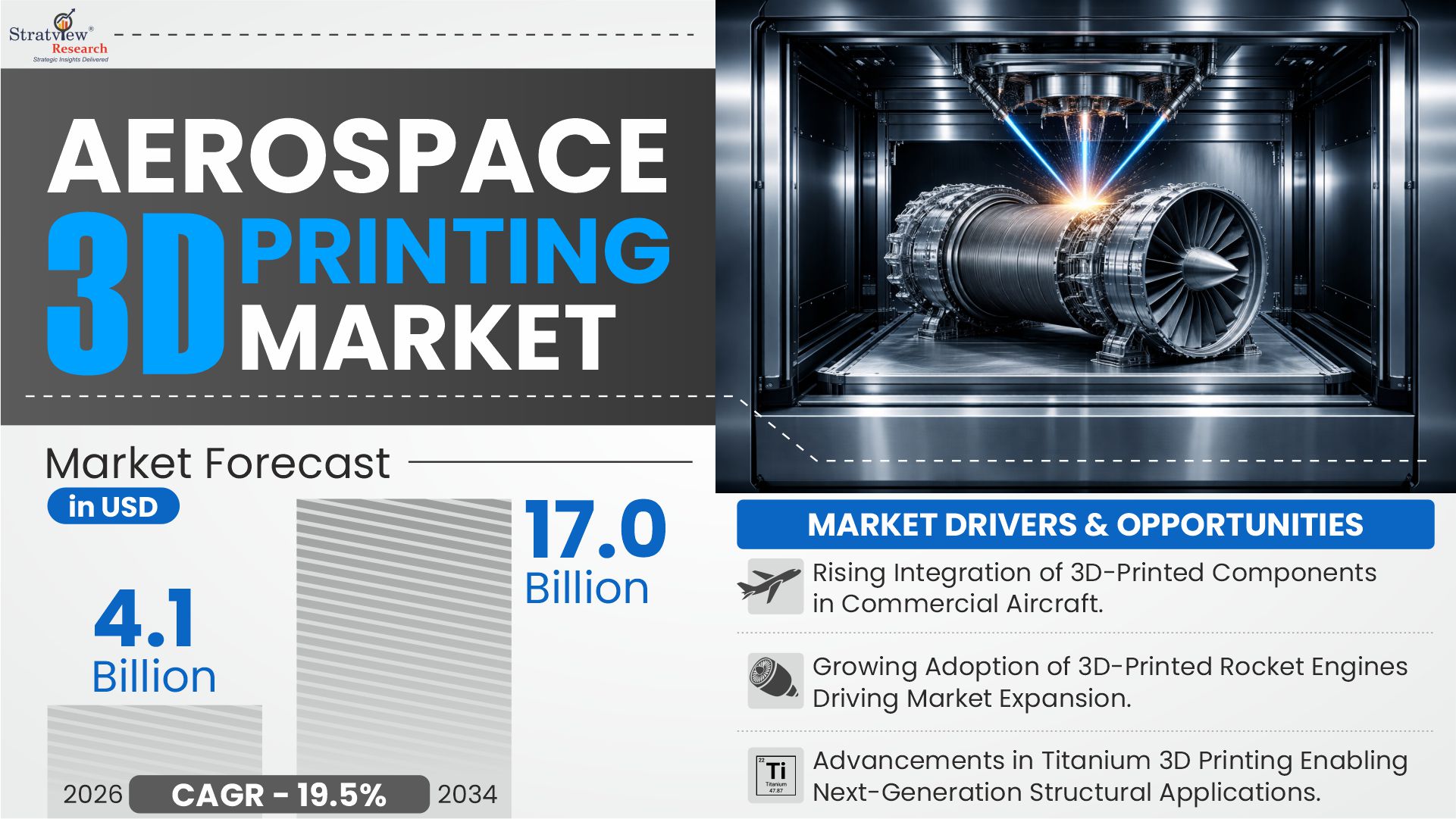

"Aerospace 3D printing market size was USD 3.4 billion in 2025."

The market size in 2024 was USD 2.8 billion. In 2025, the market experienced a YoY growth of 20.7% to reach a value of USD 3.4 billion.

The market is expected to reach USD 4.1 billion in 2026, witnessing an annual growth of 20.5%.

The market size will reach USD 17.0 billion in 2034, witnessing a market growth (CAGR) of 19.5% during the forecast period of 2026-2034.

The annual demand for aerospace 3D printing was USD 3.4 billion in 2025 and is expected to reach USD 4.1 billion in 2026, reflecting a year-over-year (YoY) growth of 20.5% compared with 2025.

During the forecast period (2026-2034), the aerospace 3D printing market is expected to grow at a CAGR of 19.5%. The annual demand will reach USD 17.0 billion in 2034.

During 2026-2034, the aerospace 3D printing industry is expected to generate a cumulative sales opportunity of USD 83.6 billion, reflecting strong long-term revenue visibility and sustained adoption across commercial aviation, defense, and space applications.

Want to get a free sample? Register Here

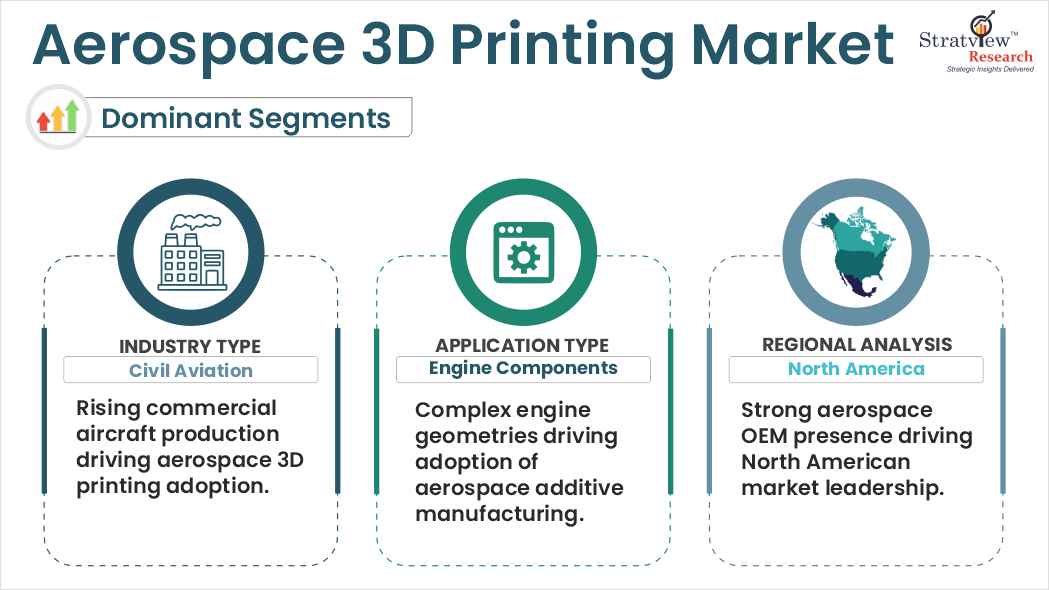

North America dominates the market, whereas Asia-Pacific is expected to grow at the fastest pace during the forecast period.

By vertical type, services segment is likely to remain dominant and the fastest-growing type in the foreseeable future.

By industry type, civil aviation accounts for the maximum share of the market during the forecast period.

By application type, engine components are expected to account for the largest share of the aerospace 3D printing market.

Have a look at the sales opportunities presented by the aerospace 3D printing market in terms of growth and market forecast.

|

Aerospace 3D Printing Market Data & Statistics |

||

|

Market Statistics |

Value (in USD Billion) |

Market Growth (%) |

|

Annual Market Size in 2024 |

USD 2.8 billion |

- |

|

Annual Market Size in 2025 |

USD 3.4 billion |

YoY Growth in 2025: 20.7% |

|

Annual Market Size in 2026 |

USD 4.1 billion |

YoY Growth in 2026: 20.5% |

|

Annual Market Size in 2034 |

USD 17.0 billion |

CAGR 2026-2034: 19.5% |

|

Cumulative Sales Opportunity during 2026-2034 |

USD 83.6 billion |

- |

|

Top 10 Countries’ Market Share in 2025 |

USD 2.7 billion+ |

> 80% |

|

Top 10 Companies’ Market Share in 2025 |

USD 1.8 billion - USD 2.3 billion |

50% - 70% |

Aerospace 3D printing, also known as additive manufacturing in aerospace, refers to the process of producing aircraft and spacecraft components layer-by-layer using advanced materials such as titanium alloys, aluminum, and high-performance polymers. This technology enables the manufacturing of complex geometries, reduced material waste, and optimized structures that are not feasible with traditional aerospace component manufacturing technologies.

Aerospace 3D printing is widely used across commercial aviation, defense, and space applications to produce lightweight aerospace components, improve fuel efficiency, and streamline production processes. As a result, additive manufacturing is becoming a critical enabler of next-generation aircraft manufacturing and is influencing the future of the global aerospace additive manufacturing market.

Rising Integration of 3D-Printed Components in Commercial Aircraft

The growing integration of additive manufacturing in commercial aircraft production is a key driver accelerating the aerospace 3D printing market. Leading OEMs such as Airbus and Boeing are increasingly deploying 3D-printed components across platforms, including narrow-body and wide-body aircraft, to improve efficiency and reduce production complexity.

For instance, Airbus produces over 25,000 3D-printed parts annually and has achieved up to 40% weight reduction and 80–85% lead time reduction in select components, while Boeing has integrated additive manufacturing into structural brackets, ducts, and cabin components across its aircraft programs. Additionally, GE Aerospace has deployed 3D-printed fuel nozzles in LEAP engines, consolidating 20+ parts into a single component.

This increasing adoption is driven by the need for lightweight structures, fuel efficiency, and faster production cycles, with modern aircraft already incorporating 1,000+ additively manufactured parts. As OEMs continue to scale serial production and certification of 3D-printed components in line with regulatory frameworks such as FAA and EASA, additive manufacturing is expected to become an integral part of next-generation aircraft manufacturing, supporting sustained market growth.

Growing Adoption of 3D-Printed Rocket Engines Driving Market Expansion

The rapid adoption of additive manufacturing in rocket propulsion systems is emerging as a significant growth driver for the aerospace 3D printing market, particularly driven by the expansion of commercial space programs globally. Companies such as Agnikul Cosmos, Relativity Space, and Rocket Lab are increasingly developing 3D-printed rocket engines and components to improve production speed and design efficiency.

For instance, Agnikul successfully tested its fully 3D-printed semi-cryogenic “Agnite” engine in 2026, while Relativity Space has demonstrated the capability to manufacture up to 85% of its Terran rocket structure using additive manufacturing, and Rocket Lab extensively utilizes 3D printing for its Rutherford engines. These advancements highlight the growing industry shift toward highly integrated, additively manufactured propulsion systems.

Additive manufacturing enables the production of complex rocket engines as single-piece structures, eliminating welds and reducing part count, which significantly lowers failure risks and production timelines. In several cases, engine production timelines have been reduced from months to less than a few weeks, supporting rapid launch cycles and scalability. This trend is expected to accelerate adoption across global space and defense programs, reinforcing additive manufacturing as a critical enabler of next-generation aerospace manufacturing.

Advancements in Titanium 3D Printing Enabling Next-Generation Structural Applications

The advancement of titanium-based additive manufacturing is creating significant long-term opportunities in the aerospace 3D printing market, particularly for structural and load-bearing applications. For instance, Airbus is actively scaling the use of Directed Energy Deposition (DED) technology for manufacturing large titanium components, enabling substantial reductions in material waste compared to traditional machining processes.

This evolution is expected to expand additive manufacturing beyond small components toward primary aircraft structures, where high buy-to-fly ratios have historically limited efficiency. As OEMs accelerate the industrialization of titanium 3D printing, suppliers are expected to benefit from rising demand for advanced materials, high-performance printing systems, and specialized post-processing solutions, supporting long-term market growth.

|

Segmentations |

List of Sub-segments |

Dominant/Fastest Growing Segment |

|

Vertical Type Analysis |

Hardware, Software, Material, and Services |

Services segment is likely to remain dominant and the fastest-growing type in the foreseeable future. |

|

Industry Analysis |

Civil Aviation, Military Aircraft, and Spacecraft |

Civil aviation accounts for the maximum share of the market during the forecast period. |

|

Application Analysis |

Engine Components, Structural Components, and Space Components |

Engine components are expected to account for the largest share of the aerospace 3D printing market. |

|

Regional Analysis |

North America, Europe, Asia-Pacific, and the Rest of the World. |

North America dominates the market, whereas Asia-Pacific is expected to grow at the fastest pace during the forecast period.

|

"Civil Aviation Leads Demand as Aircraft Production and Fleet Modernization Accelerate"

Based on industry, the market is categorized into civil aviation, military aircraft, and spacecraft, representing the primary end-use domains of 3D printing in the aviation and defense sectors. The civil aviation segment accounts for the largest share of the aerospace 3D printing market, supported by increasing commercial aircraft deliveries, fleet modernization programs, and stringent fuel efficiency requirements.

Aircraft manufacturers are increasingly integrating 3D-printed components to reduce structural weight, enhance performance, and streamline supply chains. This adoption reflects how additive manufacturing is being used to address both operational efficiency and sustainability goals, reinforcing its growing importance in commercial aerospace production.

"Engine Components Segment Dominates with High Adoption in Complex and High-Performance Parts"

In terms of application, the market is segmented into engine components, structural components, and space components, highlighting diverse use cases of aerospace additive manufacturing technologies. The engine components segment is expected to contribute the largest share, due to the high complexity, performance requirements, and cost sensitivity of propulsion systems.

Additive manufacturing enables the production of intricate geometries and internal cooling channels that are not feasible through conventional methods. It also supports part consolidation, reducing assembly requirements and improving reliability. For instance, GE Aerospace has successfully deployed 3D-printed fuel nozzles in commercial jet engines, consolidating multiple components into a single unit and improving overall engine efficiency. This demonstrates the practical advantages of additive manufacturing in high-performance aerospace applications.

Want to get more details about the segmentations? Register Here

"North America Maintains Leadership While Asia-Pacific Emerges as the Fastest-Growing Market"

The market is segmented into North America, Europe, Asia-Pacific, and the Rest of the World, reflecting global adoption trends of aerospace 3D printing technologies. North America dominates the market, supported by the presence of leading aerospace OEMs, advanced manufacturing infrastructure, and strong investments in research and development.

In contrast, Asia-Pacific is expected to witness the fastest growth, driven by expanding aviation markets, increasing defense spending, and growing investments in domestic aerospace manufacturing capabilities. Countries such as China and India are actively strengthening their additive manufacturing ecosystems, positioning the region as a key growth engine in the global aerospace additive manufacturing market.

Most of the major players compete in some of the factors, including price, service offerings, and regional presence, etc. The following are the key players in the aerospace 3D printing market–

EnvisionTEC GmbH

GE Aerospace

Hoganas AB

Materialise NV

Oerlikon Group

Renishaw plc

Stratasys Ltd.

The Trumpf Group

Note: The above list does not necessarily include all the top players in the market.

Are you a leading player in this market? We would love to include your name. Please write to us at [email protected]

March 2026 – Agnikul Cosmos Demonstrates Rapid Manufacturing of 3D-Printed Booster Engine

Agnikul Cosmos successfully 3D printed and test-fired a single-piece booster rocket engine within just seven days, compared to traditional manufacturing timelines of 6–7 months, highlighting a 90–97% reduction in production time.

The engine, manufactured as a fully integrated structure without welding or assembly, reduces failure points and improves repeatability, enabling faster and more reliable production cycles.

This advancement supports the company’s plan to scale up to 25–30 launches per year, demonstrating how additive manufacturing is enabling high-frequency, responsive launch capabilities in the commercial space sector.

August 2025 – Breakthrough in 3D-Printed Titanium Fuel Tanks Validates Space-Grade Additive Manufacturing

A joint team, including the Korea Aerospace Research Institute (KARI), successfully developed a 3D-printed titanium (Ti64) fuel tank that passed critical durability testing, marking a world-first validation for space applications.

The tank, measuring 640 mm in diameter, withstood extreme operating conditions, including pressures up to 330 bar and cryogenic temperatures of −196°C, demonstrating its suitability for real-world aerospace environments.

Notably, the component required no additional coating or post-processing to meet space-grade standards, indicating a major leap toward direct-use additive manufacturing of high-pressure propulsion systems.

This report provides market intelligence most comprehensively. The report structure has been kept so that it offers maximum business value. It provides critical insights into market dynamics and will enable strategic decision-making for existing market players as well as those willing to enter the market.

The following are the key features of the report:

Market structure: Overview, industry life cycle analysis, supply chain analysis.

Market environment analysis: Growth drivers and constraints, Porter’s five forces analysis, SWOT analysis.

Market trend and forecast analysis.

Market segment trend and forecast.

Competitive landscape and dynamics: Market share, Service portfolio, New Product Launches, etc.

COVID-19 impact and its recovery curve.

Attractive market segments and associated growth opportunities.

Emerging trends.

Strategic growth opportunities for the existing and new players.

Key success factors.

|

Market Study Period |

2019-2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Trend Period |

2019-2024 |

|

Number of Tables & Figures |

>100 |

|

Number of Segments Analysed |

4 (Vertical Type, Industry Type, Application Type, and Region) |

|

Number of Regions Analysed |

4 (North America, Europe, Asia-Pacific, Rest of the World) |

|

Countries Analysed |

15 (The USA, Canada, Mexico, Germany, France, Italy, The UK, China, Japan, India, Brazil, Saudi Arabia, Rest of Europe, Rest of APAC, and Rest of the World) |

|

Free Customization Offered |

10% |

|

After Sales Support |

Unlimited |

|

Report Presentation |

Complimentary |

|

Market Dataset |

Complimentary |

|

Further Deep Dive & Consulting Services |

10% Discount |

The report provides detailed insights into the market dynamics to enable informed business decision-making and growth strategy formulation based on the opportunities present in the market.

The aerospace 3D printing market is segmented into the following categories:

By Vertical Type

Hardware

Software

Material

Services

By Industry Type

Civil Aviation

Military Aircraft

Spacecraft

By Application Type

Engine Components

Structural Components

Space Components

By Region

North America (Country Analysis: the USA, Canada, and Mexico)

Europe (Country Analysis: Germany, France, the UK, Russia, Spain, and the Rest of Europe)

Asia-Pacific (Country Analysis: China, Japan, India, South Korea, and Rest of Asia-Pacific)

Rest of the World (Sub-Region Analysis: Latin America, the Middle East, and Others)

This strategic assessment report provides a comprehensive analysis that reflects today’s aerospace 3D printing market realities and future market possibilities for the forecast period.

The report segments and analyzes the market in the most detailed manner to provide a panoramic view of the market.

This report offers high-quality insights and is the outcome of a detailed research methodology comprising extensive secondary research, rigorous primary interviews with industry stakeholders, and validation with internal databases and statistical tools.

More than 1,000 authenticated secondary sources, including company annual reports, industry publications, press releases, journals, and technical papers, were used to gather data.

Primary interviews were conducted with market participants across the value chain, including OEMs, suppliers, distributors, and industry experts to obtain both qualitative and quantitative insights.

With this detailed report, Stratview Research offers one of the following free customization options to our respectable clients:

Company Profiling

Competitive Benchmarking

Custom Research: Stratview Research offers custom research services across sectors. In case of any custom research requirement related to market assessment, competitive benchmarking, sourcing and procurement, target screening, and others, please send your inquiry to [email protected]

The report is delivered digitally through our online portal. Buyers receive login credentials from our team to access the report and may update their credentials at any time after the initial login.

Delivery timelines depend on the status of the report:

For the most accurate delivery timeline, please contact us to confirm the current status of the report.

Yes. You may request a complimentary preview of the report through a video conference with our team.

Yes. The scope of the report can be fully customized to align with your specific research objectives and information requirements.

Please contact us at [email protected], and our team will be happy to discuss your requirements and propose a tailored solution.

Yes. Selected sections of the report can be purchased separately based on your requirements. Please contact us at [email protected] to discuss your needs.

Yes, AI can help gather publicly available information, but its outputs are only as reliable as the data it accesses. Stratview Research reports are built using validated data, extensive primary interviews with industry stakeholders, and the expertise of our experienced research team.

Additionally, many critical insights, including market dynamics, competitive intelligence, and industry-specific trends, are not publicly available and therefore cannot be captured through AI alone.

The global aerospace 3D printing market was valued at USD 3.4 billion in 2025, driven by adoption in commercial aircraft, rocket engines, and space components.

The market is projected to grow at a CAGR of 19.5% during 2026–2034, reaching USD 17.0 billion by 2034, supported by the rising adoption of additive manufacturing across the aerospace sector.

North America currently leads due to the presence of major OEMs and advanced manufacturing infrastructure, while Asia-Pacific is emerging as the fastest-growing region, driven by China, India, and South Korea.

Engine components hold the largest share, followed by structural and space components, as additive manufacturing enables complex geometries, part consolidation, and enhanced performance.

The key end-use industries include civil aviation, military aircraft, and spacecraft, with civil aviation accounting for the largest share due to fleet modernization and commercial aircraft production.

Rising integration of 3D-printed aircraft components, adoption of 3D-printed rocket engines, and advancements in titanium additive manufacturing for structural applications are accelerating market growth.

Leading companies include 3D Systems Corporation, EOS GmbH, GE Aerospace, Materialise NV, Renishaw plc, Stratasys Ltd., and The Trumpf Group, actively driving innovation and production capabilities.

Expansion into primary aircraft structures, high-performance rocket propulsion systems, and adoption of titanium additive manufacturing are expected to unlock long-term market growth and revenue opportunities.

WE ACCEPT