404

+1-313-307-4176

EV Power Module Market Analysis | 2025-2031

EV Power Module Market Size, Share, Trends, Dynamics, Forecast, & Growth Analysis: 2025-2031

EV Power Module Market is segmented by Propulsion Type (BEV and HEV), by Vehicle Type (LV and M&HCV), by Application Type (Inverter, On-Board Charger, and DC-DC Converter), by Technology Type (IGBT, SiC, and GaN), by Voltage Type (Less than 750V and 750V to 1200V), and by Region (North America [The USA, Canada, and Mexico]; Europe [Germany, France, The UK, Italy, Russia, and Rest of Europe]; Asia-Pacific [China, Japan, India, South Korea, and Rest of Asia-Pacific]; and Rest of the World [Brazil, Argentina, and Others]).

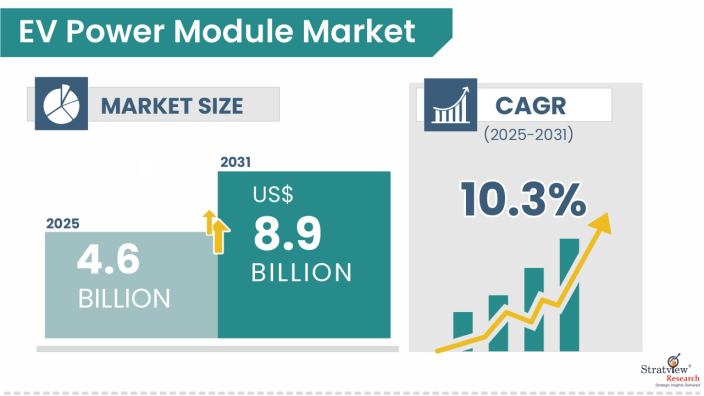

The EV power module market size was USD 4.6 billion in 2025 and is likely to grow at a CAGR of 10.3% during 2025-2031 to reach USD 8.9 billion in 2031.

Want to know more about the market scope? Register Here

The EV power module is a vital component in electric vehicles, playing a central role in converting and managing electric power between the battery and the motor to ensure optimal performance and efficiency. It typically consists of advanced semiconductor devices such as IGBTs (Insulated Gate Bipolar Transistors) or MOSFETs (Metal-Oxide-Semiconductor Field-Effect Transistors), which enable high-speed switching and precise control over power flow. These modules are critical for the functioning of key systems like traction inverters, DC-DC converters, and onboard chargers.

With the global shift to electric mobility, demand for compact, high-efficiency EV power modules is rising. These modules handle high voltage and current with minimal loss, aided by technologies like SiC and double-sided cooling. By reducing system size and weight, they enable longer ranges and faster charging, making them essential to next-gen EV innovation.

A considerable number of strategic alliances, including M&As, JVs, etc., have been performed over the past few years:

|

Segmentations |

List of Sub-Segments |

Segments with High-Growth Opportunity |

|

Propulsion-Type Analysis |

BEV and HEV |

BEVs hold a larger market share and are expected to remain the dominant and faster-growing segment. |

|

Vehicle-Type Analysis |

LV and M&HCV |

LV is anticipated to contribute a larger share of the EV power module market. |

|

Application-Type Analysis |

Inverter, On-Board Charger, and DC-DC Converter |

Inverters hold the largest share, while on-board chargers are projected to grow rapidly with EV expansion. |

|

Technology-Type Analysis |

IGBT, SiC, and GaN |

IGBT remains the dominant technology due to cost-effectiveness and maturity |

|

Voltage-Type Analysis |

Less than 750V and 750V to 1200V |

The 750V to 1200V segment is anticipated to grow faster with demand for high-voltage EV architectures. |

|

Region Analysis |

North America, Europe, Asia-Pacific, and The Rest of the World |

Asia-Pacific is the dominant region, while North America is the fastest-growing. |

“BEV is likely to remain the larger and faster-growing propulsion type of the market during the forecast period.”

The EV power module market is segmented into BEVs and HEVs. The global shift toward full electrification, regulatory support, and OEM strategies that increasingly favor BEVs over HEVs. BEVs require high-capacity power modules to support fully electric propulsion, fueling demand for advanced, high-voltage systems. In contrast, HEVs rely on smaller modules due to their limited electric range and shared powertrain with internal combustion engines, resulting in comparatively lower demand for power modules.

“LV is likely to remain the larger and faster-growing vehicle type of the market during the forecast period.”

The EV power module market is segmented into LV and M&HCV. Light vehicles are expected to account for a larger share of the market, primarily due to the significantly higher production and sales volumes of passenger EVs worldwide. Rapid electrification of LV portfolios by major automakers is driving widespread integration of power modules in compact and mid-size EVs. Moreover, the faster adoption of BEVs in the passenger segment—supported by urban mobility trends and government incentives—continues to fuel demand in this category.

“Inverter is expected to remain the largest application type, whereas the on-board charger is likely to experience the fastest growth during the forecast period.”

The market is segmented into inverter, on-board charger, and DC-DC converter. Inverters hold the largest share of the market, as they are essential for converting DC power from the battery into AC power to drive the electric motor, making them a critical component in every electric vehicle. On the other hand, on-board chargers are projected to witness rapid growth, driven by the expanding EV market and rising demand for efficient, fast, and reliable charging solutions. As charging infrastructure advances and consumer expectations for shorter charging times increase, on-board chargers are becoming increasingly vital, fueling their market expansion.

“IGBT is likely to remain the dominant technology of the market over the next five years.”

The market is segmented into IGBT, SiC, and GaN. IGBT remains the dominant technology due to its cost-effectiveness, proven reliability, and widespread adoption in existing EV designs. Its technological maturity and established manufacturing processes make it the preferred choice for many automakers, despite emerging alternatives like SiC and GaN gaining traction.

As EV system voltages increase, SiC is expected to gain popularity due to its superior efficiency and high-temperature performance in high-voltage applications. Meanwhile, GaN is in the emerging stage, offering advantages in compactness and high-frequency switching, but it is currently limited to lower-voltage segments and niche applications.

“The Asia-Pacific is expected to be the dominant region, whereas North America will be the fastest-growing region.”

In terms of region, the market is segmented into North America, Europe, Asia-Pacific, and RoW. Asia-Pacific is expected to be the dominant region due to its large-scale EV manufacturing, supportive government policies, and strong consumer demand, especially in countries like China, Japan, and South Korea. Meanwhile, North America is projected to be the fastest-growing region, driven by increasing EV adoption, expanding charging infrastructure, and growing investments in electric mobility technologies.

Know the high-growth countries in this report. Register Here

The market is highly concentrated, with over 30 players globally. Most of the major players compete in some of the governing factors, including price, service offerings, regional presence, etc. Some of the major players provide a complete range of services. The following are the key players in the EV power module market.

Here is the list of the Top Players (Based on Dominance)

Note: The above list does not necessarily include all the top players in the market.

Are you the leading player in this market? We would love to include your name. Please write to us at [email protected]

This report provides market intelligence most comprehensively. The report structure has been kept so that it offers maximum business value. It provides critical insights into market dynamics and will enable strategic decision-making for existing market players as well as those willing to enter the market. The following are the key features of the report:

This report studies the market, covering a period of 12 years of trends and forecasts. The report provides detailed insights into the market dynamics to enable informed business decision-making and growth strategy formulation based on the opportunities present in the market.

The EV power module market is segmented into the following categories.

By Propulsion Type

By Vehicle Type

By Application Type

By Technology Type

By Voltage Type

By Region

With this detailed report, Stratview Research offers one of the following free customization options to our respected clients:

Company Profiling

Competitive Benchmarking

Custom Research: Stratview Research offers custom research services across sectors. In case of any custom research requirement related to market assessment, competitive benchmarking, sourcing and procurement, target screening, and others, please send your inquiry to [email protected].

EV power module technology refers to the integration of semiconductor devices like IGBT, SiC, or GaN used to manage and convert electrical energy within electric vehicles. These modules are crucial for functions such as motor control, battery charging, and energy conversion. They enable efficient power flow, reduced energy loss, and compact system design in EVs.

The EV power module market is estimated to grow at a CAGR of 10.3% by 2031, driven by rising EV adoption, demand for high-efficiency power electronics, and advances in semiconductor technologies.

The EV power module market is estimated to reach USD 8.9 billion in 2031.

The Asia-Pacific region holds the largest market share in the EV power module market due to the presence of leading EV manufacturers, robust supply chains, strong government support for electrification, and high consumer demand, especially in countries like China, Japan, and South Korea.

Infineon Technologies, OnSemi, Fuji Electric Co., Ltd., and STMicroelectronics are the leading players in the market.

WE ACCEPT