404

+1-313-307-4176

Liquid Chromatography Market Report

Liquid Chromatography Market Size, Share, Trend, Forecast, Competitive Analysis, and Growth Opportunity: 2024-2031.

Liquid Chromatography Market is segmented by Technique Type (HPLC, Ion Chromatography, Flash, Membrane, and Other Techniques), by Component Type (Instrument/Skid, Consumables, Software, and Other Components), by System Type (Single-Use Systems and Multi-Use Systems),by End-Use Industries Type (Pharmaceutical, Biotechnology, Academic, Chemicals, Environmental Testing, CROs [Contract Research Organizations], Government Research, Hospitals & Clinical Trials, Agricultural, Food & Beverages, and Other End-Use Industries), and by Region (North America [The USA, Canada, and Mexico], Europe [Germany, France, The UK, and Rest of Europe], Asia-Pacific [China, Japan, India, and Rest of Asia-Pacific], and Rest of the World [Latin America, Middle East, and Others]).

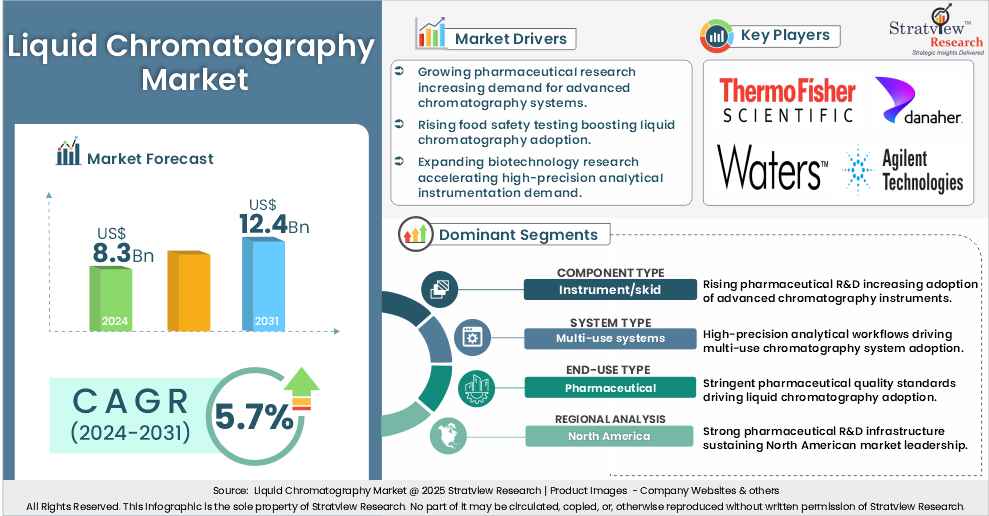

“The liquid chromatography market size was US$ 8.3 billion in 2024 and is likely to grow at a healthy CAGR of 5.7% in the long run to reach US$ 12.4 billion in 2031”.

Want to get a free sample? Register Here

Introduction

Liquid chromatography (LC) is a powerful analytical technique used to separate, identify, and quantify the components of a mixture in liquid form. It operates on the principle of differential partitioning between a mobile phase (liquid) and a stationary phase (typically a solid or liquid supported on a solid). The technique is extensively used in laboratories and industrial settings for analyzing complex mixtures, ranging from pharmaceutical formulations and biological samples to food products and environmental matrices.

The liquid chromatography market is experiencing significant growth driven by the increasing demand for precise analytical tools across diverse end-use industries. One of the primary drivers is the expanding pharmaceutical and biotechnology industries, where liquid chromatography plays a crucial role in drug development, quality control, and regulatory compliance. Moreover, rising research & development activities in academic institutions and government laboratories are contributing to sustained market demand.

Technological advancements such as high-performance liquid chromatography (HPLC), ion chromatography, flash chromatography, membrane chromatography, and other specialized techniques have enhanced the sensitivity, efficiency, and throughput of analysis, making liquid chromatography indispensable in modern analytical laboratories. In particular, the adoption of single-use systems in biopharmaceutical production and the growing use of automated and software-integrated systems are transforming workflow capabilities and boosting productivity.

Furthermore, increasing regulatory scrutiny regarding product safety and environmental quality is propelling the need for accurate testing solutions, further strengthening the adoption of liquid chromatography across industries like food & beverages, environmental testing, agriculture, and clinical diagnostics. The rise of contract research organizations (CROs), especially in emerging markets, is another factor accelerating demand, as companies outsource complex analytical tasks to save time and reduce costs.

Recent Market JVs and Acquisitions:

A considerable number of strategic alliances, including M&As, JVs, etc., have been performed over the past few years:

Recent Product Development:

|

Segmentations |

List of Sub-Segments |

Segments with High-Growth Opportunity |

|

Technique-Type Analysis |

HPLC, Ion Chromatography, Flash, Membrane, and Other Techniques |

HPLC is estimated to be the dominant type of the liquid chromatography market during the forecast period. |

|

Component-Type Analysis |

Instrument/Skid, Consumables, Software, and Other Components |

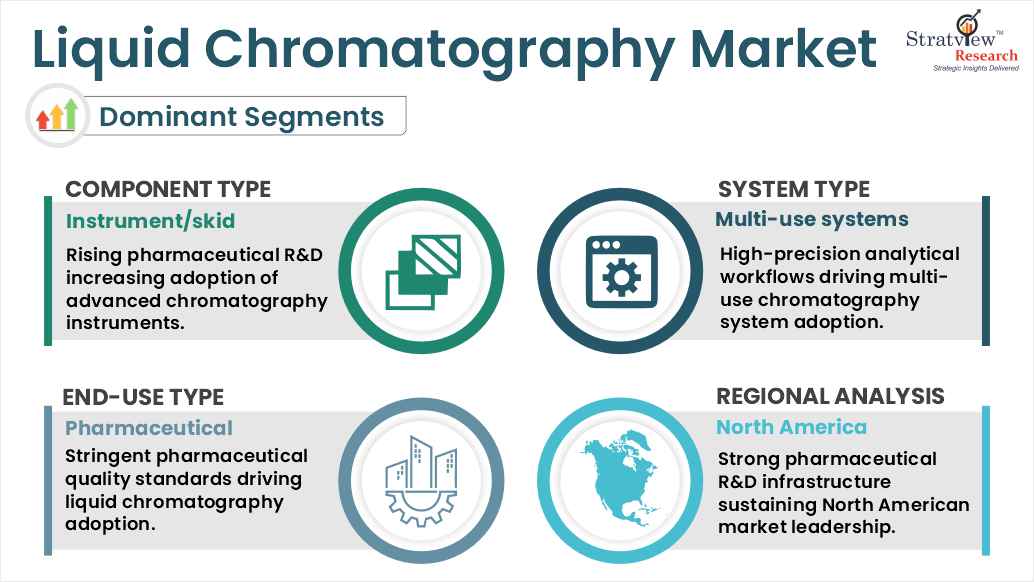

Instrument/skid is expected to hold the major share by component type, while software is projected to witness the fastest growth during the forecast period. |

|

System-Type Analysis |

Single-Use Systems and Multi-Use Systems |

Multi-use systems are anticipated to be the dominant system type, whereas single-use systems are poised to experience the most rapid growth throughout the forecast period. |

|

End-Use Industries -Type Analysis |

Pharmaceutical, Biotechnology, Academic, Chemicals, Environmental Testing, CROs [Contract Research Organizations], Government Research, Hospitals & Clinical Trials, Agricultural, Food & Beverages, and Other Industries |

The pharmaceutical industry is likely to be the dominant end-use industry of the market during the forecast. |

|

Regional Analysis |

North America, Europe, Asia-Pacific, and The Rest of the World |

North America is projected to maintain its market dominance throughout the forecast period, while Asia-Pacific is expected to record the fastest growth rate. |

“HPLC is expected to be the most widely used technique of the liquid chromatography market over the forecast period.”

Based on technique type, the liquid chromatography market is segmented as HPLC, ion chromatography, flash chromatography, membrane chromatography, and other techniques. High-Performance Liquid Chromatography (HPLC) is projected to be the most preferred technique in the liquid chromatography market over the forecast period, and several key factors underpin this dominance.

HPLC's position as the most preferred technique in the liquid chromatography market stems from its unmatched analytical capabilities and adaptability to diverse industry needs. Unlike specialized techniques such as ion chromatography (limited to charged species) or flash chromatography (primarily for preparative purification), HPLC delivers exceptional resolution, sensitivity, and quantitative accuracy across a vast range of compounds. This versatility makes it indispensable for applications demanding rigorous quality control and complex mixture analysis. Its ability to detect trace impurities down to 0.01% levels, critical in pharmaceuticals and food safety, far surpasses alternatives in routine analytical workflows.

The technique's breadth of applications solidifies its commercial dominance. In pharmaceuticals, HPLC is embedded in drug development, stability testing, impurity profiling, and bioequivalence studies, forming the backbone of regulatory submissions to agencies like the FDA. For instance, it is the gold standard for establishing drug shelf life by quantifying degradants under accelerated stability conditions. Beyond pharma, HPLC serves critical roles in clinical diagnostics (e.g., HbA1c testing for diabetes), forensic toxicology (drug detection in biological samples), and food safety (pesticide residue analysis). This cross-industry applicability contrasts sharply with niche techniques like membrane chromatography, which are confined to specific bioprocessing steps. The expanding scope of clinical research, particularly for complex biologics like monoclonal antibodies, further amplifies HPLC's utility, driving its adoption in contract research organizations and biotech firms.

By Component Type

“Instrument/skid is expected to be the dominant component type, while software is projected to achieve the highest growth rate over the forecast period.”

By component type, the liquid chromatography market is segmented as instrument/skid, consumables, software, and other components. Instrument/skid dominates the liquid chromatography (LC) market largely because it forms the foundation of analytical workflows. These physical systems, comprising pumps, detectors, autosamplers, and columns, are essential for performing separations in laboratories across pharmaceuticals, biotechnology, environmental monitoring, and diagnostics. The high adoption rate among pharmaceutical and biotech firms, driven by stringent regulatory requirements, increasing R&D spending, and the proliferation of techniques like UHPLC and LC-MS, reinforces this dominance. Moreover, these instruments often demand substantial capital investment and upkeep, further anchoring their large share in the overall LC market.

The software segment, often referred to as Liquid Chromatography Software (LCS), stands out as the fastest-growing component. This rapid expansion is propelled by the rising demand for high-throughput screening, automation, and complex data management in modern laboratories. As LC systems become more sophisticated and generate increasingly voluminous and intricate datasets, especially in hyphenated systems like LC-MS and UHPLC, the necessity for advanced software tools intensifies.

In addition, software solutions are becoming more indispensable due to regulatory agencies such as the FDA and EMA, which demand rigorous data traceability and compliance. Cloud-based, server-enabled platforms, and AI-enhanced analytics are gaining traction owing to their ability to streamline workflows, optimize method development, and ensure high data quality. As labs across biotech, environmental, food safety, and clinical diagnostics industries undertake complex, large-scale analyses, the value and growth of chromatography software continues to climb.

By System Type

“Multi-use systems are expected to be the primary drivers of market demand, while single-use systems are projected to exhibit the faster growth during the forecast period.”

Based on system type, the liquid chromatography market is segmented into single-use systems and multi-use systems. Multi-use systems are expected to remain the dominant system type in the market because they offer high precision, reproducibility, and flexibility across a wide range of analytical applications. Widely used in research, quality control, and large-scale biopharmaceutical production, multi-use systems like HPLC/UHPLC deliver superior quantitative accuracy and resolution, qualities essential in regulated environments. These systems also support extended lifecycles and diverse workflows, making them a cost-effective and reliable choice for labs that require dependable performance across varied analytical needs.

Single-use systems are projected to be the fastest-growing system type in the market over the forecast period. Their appeal lies in enabling rapid deployment, reduced risk of cross-contamination, and elimination of time-intensive cleaning and validation processes. Biopharma manufacturers, especially those working with biologics such as monoclonal antibodies and vaccines, find these attributes crucial, it allows them to scale up flexibly while reducing both capital and operational costs. Moreover, single-use platforms align naturally with modern manufacturing trends like modular production and disposable bioprocessing, gaining strong adoption in mid-scale and clinical production settings.

By End-Use Industries Type

“The pharmaceutical industry is projected to be the major demand generator for liquid chromatography during the forecast period.”

The liquid chromatography market serves a diverse range of end-use industries, including pharmaceuticals, biotechnology, academic research, chemicals, environmental testing, contract research organizations (CROs), government research, hospitals & clinical trials, agriculture, food & beverages, and other end-use industries. The pharmaceutical industry stands out as the largest end-use category in the liquid chromatography (LC) market because it relies on LC throughout every stage of drug development, from discovery and development to quality control and regulatory approval. LC systems such as HPLC and UHPLC are indispensable for analyzing active pharmaceutical ingredients (APIs), excipients, impurities, metabolites, and degradation products. These methods ensure drug safety, efficacy, potency, and purity, which is essential for compliance with stringent regulations from agencies like the FDA and EMA.

Advances in biopharmaceuticals, such as monoclonal antibodies, gene therapies, and complex biologics, have further amplified the need for high-performance LC techniques. These molecules require sophisticated separation and detection capabilities, often combining LC with mass spectrometry (LC–MS) to dissect and monitor biomolecules, post-translational modifications, and low-abundance impurities. The precision, high sensitivity, and reproducibility of LC are thus critical in both the identification of promising therapeutic compounds and ensuring process consistency during scale-up and commercialization.

Want to get more details about the segmentations? Register Here

Regional Analysis

“North America is expected to retain its leading market position over the forecast period, while Asia-Pacific is poised to emerge as the fastest-growing region.”

North America remains a dominant force in the liquid chromatography market due to its well-established pharmaceutical and biotech industries, advanced research infrastructure, and strong regulatory environment. Major global players such as Thermo Fisher, Agilent, Waters, Shimadzu, and Bio-Rad are headquartered or have significant operations in this region, bolstered by robust lab infrastructure and high public and private R&D investment. In addition, stringent FDA regulations require rigorous analytical testing, further reinforcing North America's lead in high-performance liquid chromatography adoption.

Asia-Pacific is emerging as the fastest-growing region in the LC market. The region's rapid economic development, especially in China, India, Japan, and Southeast Asia, has led to significant growth in healthcare infrastructure, pharmaceutical manufacturing, and big-data–driven analytical capabilities. Government initiatives aimed at enhancing biotech and life-sciences industries, alongside rising environmental monitoring and food safety requirements, are driving broader LC adoption.

The market is highly consolidated, with over 50 players. Most of the major players compete in some of the governing factors, including price, product offerings, regional presence, etc. The following are the key players in the liquid chromatography market.

Here is the list of the Top Players (Based on Dominance)

Note: The above list does not necessarily include all the top players in the market.

Are you the leading player in this market? We would love to include your name. Please write to us at [email protected]

This report provides market intelligence most comprehensively. The report structure has been kept so that it offers maximum business value. It provides critical insights into market dynamics and will enable strategic decision-making for existing market players as well as those willing to enter the market. The following are the key features of the report:

The liquid chromatography market is segmented into the following categories.

Liquid Chromatography Market, by Technique Type

Liquid Chromatography Market by Component Type

Liquid Chromatography Market by System Type

Liquid Chromatography Market by End-Use Industry Type

Liquid Chromatography Market by Region

With this detailed report, Stratview Research offers one of the following free customization options to our respected clients:

Company Profiling

Competitive Benchmarking

Custom Research: Stratview Research offers custom research services across industries. In case of any custom research requirement related to market assessment, competitive benchmarking, sourcing and procurement, target screening, and others, please send your inquiry to [email protected]

The report is delivered digitally through our online portal. Buyers receive login credentials from our team to access the report and may update their credentials at any time after the initial login.

Delivery timelines depend on the status of the report:

For the most accurate delivery timeline, please contact us to confirm the current status of the report.

Yes. You may request a complimentary preview of the report through a video conference with our team.

Yes. The scope of the report can be fully customized to align with your specific research objectives and information requirements.

Please contact us at [email protected], and our team will be happy to discuss your requirements and propose a tailored solution.

Yes. Selected sections of the report can be purchased separately based on your requirements. Please contact us at [email protected] to discuss your needs.

Yes, AI can help gather publicly available information, but its outputs are only as reliable as the data it accesses. Stratview Research reports are built using validated data, extensive primary interviews with industry stakeholders, and the expertise of our experienced research team.

Additionally, many critical insights, including market dynamics, competitive intelligence, and industry-specific trends, are not publicly available and therefore cannot be captured through AI alone.

Liquid chromatography (LC) is an analytical technique used to separate, identify, and quantify components in a liquid mixture by passing it through a column packed with a solid stationary phase, using a liquid mobile phase to carry the sample. The components of the mixture move at different speeds depending on their interactions with the stationary and mobile phases, allowing for their separation.

The liquid chromatography market is estimated to grow at a CAGR of 5.7% over the forecasted years to reach US$ 12.4 billion in 2031.

North America is the largest market for liquid chromatography, due to its advanced pharmaceutical and biotechnology industries, strong research infrastructure, strict regulatory requirements, and early adoption of cutting-edge technologies. Major manufacturers, high R&D spending, and a strong presence of academic and clinical laboratories further reinforce the region's leading position in this market.

Asia Pacific is currently the fastest-growing region in the global liquid chromatography market. This growth is driven by several factors, including expanding pharmaceutical and biotechnology industries, increased investments in research & development, and the adoption of advanced analytical technologies. Countries like China and India are leading this surge due to their large populations, rising healthcare expenditures, and supportive government initiatives aimed at enhancing healthcare infrastructure and research capabilities. Additionally, the integration of artificial intelligence (AI) with high-performance liquid chromatography (HPLC) systems is enhancing data analysis and operational efficiency, further propelling market growth in the region.

The liquid chromatography market is experiencing strong growth driven by advancements in high-performance and ultra-high-performance systems, integration of automation and AI for improved efficiency, rising demand in pharmaceuticals and biotechnology for drug development and biomolecule analysis, increasing applications in food safety and environmental monitoring, and rapid adoption in emerging economies due to expanding healthcare and industrial industries.

Agilent Technologies Inc., Bio-Rad Laboratories, Biotage, Bruker Corporation, Danaher Corporation, GL Sciences Inc., Knauer Wissenschaftliche Geräte GmbH, Merck Group, PerkinElmer Inc., Repligen Corporation, Sartorius AG, SCION Instruments, Shimadzu Corporation, Thermo Fisher Scientific Inc., Tosoh Corporation, and Waters Corporation are the key players in the liquid chromatography market.

The pharmaceutical industry stands out as the largest end-use industry segment in the liquid chromatography market. This dominance stems from its extensive reliance on LC techniques, such as HPLC and UHPLC, across every stage of drug development, including routine quality control, impurity analysis, stability testing, and regulatory compliance. Pharmaceutical and biotech companies command the major share of the liquid chromatography market, driven by heavy R&D investment, increasing demand for biologics, and stringent standards from global health regulators.

WE ACCEPT