404

+1-313-307-4176

Connected Cars Market Report

Connected Cars Market Size, Share, Trend, Forecast, Competitive Analysis, and Growth Opportunity: 2025-2032

Connected Cars Market by Service Type (Telematics, Navigation, Remote Diagnostics, Multimedia Streaming, OTA Updates, eCall & Emergency Assistance, and Other Services), by Form Factor (Embedded, Integrated, and Tethered), by Platform (Android Auto, Apple CarPlay, MirrorLink, and Other Platforms), by Connectivity (Cellular, DSRC (Dedicated Short Range Communication), and Satellite), and by Region (North America [The USA, Canada, and Mexico], Europe [Germany, France, The UK, Russia, and Rest of Europe], Asia-Pacific [China, Japan, India, and Rest of Asia-Pacific], and Rest of the World [Brazil, Saudi Arabia, and Others]).

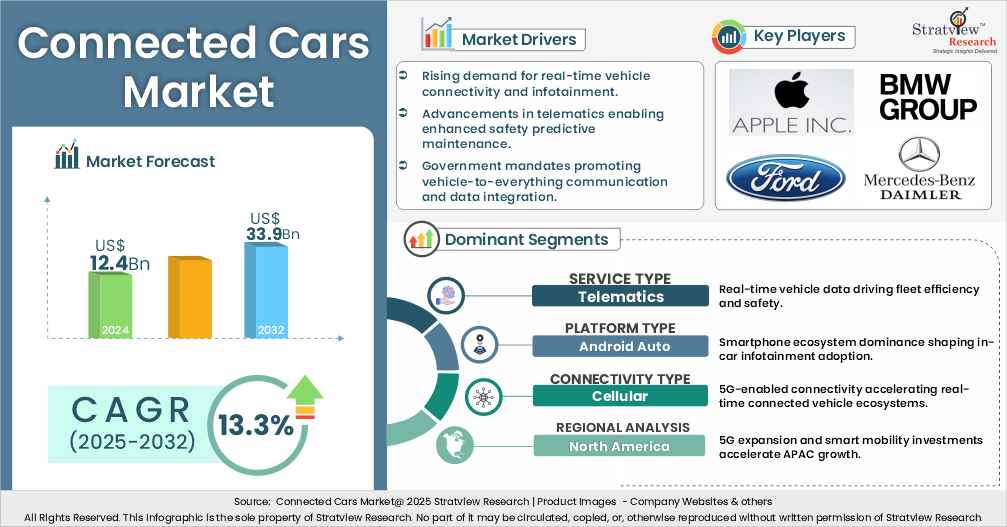

“Connected cars market size was US$12.4 billion in 2024 and is likely to grow at a decent CAGR of 13.3% in the long run to reach US$33.9 billion in 2032”.

Want to get a free sample? Register Here

Introduction

Connected cars are vehicles equipped with internet connectivity and communication technologies that enable them to interact with other devices, vehicles, infrastructure, and networks. These vehicles integrate advanced hardware and software solutions to support features such as real-time navigation, remote diagnostics, telematics, infotainment, vehicle-to-everything (V2X) communication, and over-the-air (OTA) updates. By leveraging sensors, embedded modules, and smartphone integration platforms, connected cars enhance driver convenience, passenger safety, and overall vehicle efficiency while laying the foundation for autonomous mobility.

The connected cars market has witnessed rapid growth in recent years, driven by rising consumer demand for smart mobility, increasing regulatory mandates for safety and telematics, and the growing adoption of 4G and 5G technologies. Automakers are increasingly partnering with technology providers to integrate connected platforms, while mobility service operators are utilizing connected solutions to optimize ride sharing, fleet management, and usage-based insurance models. Furthermore, the rise of electric vehicles (EVs) and autonomous driving technologies is accelerating the deployment of connected systems, making them a central element of the automotive industry’s digital transformation. With advancements in IoT, artificial intelligence, and cloud computing, the market is poised to expand significantly, offering new revenue streams for OEMs, suppliers, and service providers.

Recent Market JVs and Acquisitions:

A large number of strategic alliances, including M&As, JVs, etc., have been performed over the past few years:

Recent Product Development:

The companies are focusing their product development efforts on AI-powered voice assistants in regional languages, predictive maintenance systems adapted for driving conditions, advanced vehicle tracking solutions for fleet management, and digital payment integration for fuel and toll services. Some of the recent product developments are:

|

Segmentations |

List of Sub-Segments |

Segments with High-Growth Opportunity |

|

Service Type Analysis |

Telematics, Navigation, Remote Diagnostics, Multimedia Streaming, OTA Updates, eCall & Emergency Assistance, Other Services |

Telematics currently dominates the market, while OTA Updates are expected to witness the highest growth. |

|

Form Factor-Type Analysis |

Embedded, Integrated, Tethered |

Embedded solutions hold the largest market share, whereas Integrated systems are anticipated to grow fastest. |

|

Platform-Type Analysis |

Android Auto, Apple CarPlay, MirrorLink, Other Platforms |

Android Auto dominates due to widespread Android smartphone adoption, while Apple CarPlay is expected to experience significant growth. |

|

Connectivity-Type Analysis |

Cellular, DSRC, Satellite |

Cellular connectivity is expected to lead the connected car market throughout the forecast period. |

|

Region Analysis |

North America, Europe, Asia-Pacific, and The Rest of the World |

North America holds a significant share of the dairy enzymes market, whereas the Asia-Pacific region is likely to grow at the fastest rate. |

By Service Type

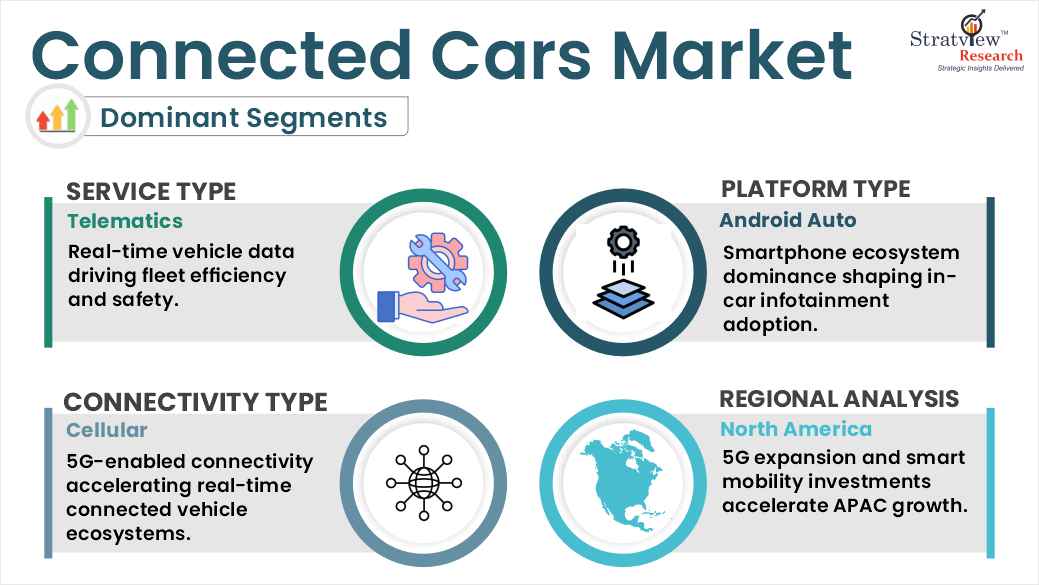

“The Telematics segment is expected to witness continued market leadership during the forecast period.”

Based on service, the market is segmented into telematics, navigation, remote diagnostics, multimedia streaming, OTA updates, eCall & emergency assistance, and other services.

Telematics is currently the dominant service segment, as it provides real-time monitoring of vehicle health, predictive maintenance, fuel efficiency tracking, fleet management solutions, and insurance telematics. Fleet operators, logistics companies, and insurance providers are increasingly using telematics to optimize operational efficiency, reduce costs, and enhance safety standards.

Whereas OTA Updates represent the fastest-growing service segment, driven by automakers’ need to remotely upgrade vehicle software, improve infotainment systems, fix security vulnerabilities, and introduce new features without requiring dealership visits. The rapid adoption of OTA services is also fueled by the increasing integration of advanced driver assistance systems (ADAS) and smart infotainment systems in both passenger and commercial vehicles, reflecting a shift toward smarter and more connected mobility. Ride-sharing services also contribute to connectivity growth, as platforms leverage vehicle connectivity for dynamic fleet management, route optimization, and real-time data sharing with passengers and drivers.

By Form Factor

“Embedded solutions are expected to maintain market dominance while Integrated systems will experience the fastest growth during the forecast period.’’

The connected cars market is segmented by form factor into Embedded, Tethered, and Integrated solutions. Embedded systems dominate the market because they are pre-installed by automakers into vehicles’ hardware, offering seamless connectivity without relying on external devices. These systems enable uninterrupted access to telematics, navigation, infotainment, safety alerts, and vehicle diagnostics, making them highly reliable for both passenger and commercial vehicles.

Integrated systems are emerging as the fastest-growing segment, combining multiple functions such as navigation, infotainment, vehicle diagnostics, and smartphone integration into a single platform. These systems appeal to consumers looking for a unified, high-tech in-car experience. Tethered systems, which rely on external devices like smartphones for connectivity, have a smaller market share due to limited convenience, but they remain popular in entry-level vehicles due to low costs. The growth of integrated systems is further accelerated by increasing consumer demand for premium and mid-range vehicles equipped with advanced features, as well as the rise of smart mobility solutions in urban areas.

By Platform Type

“Android Auto dominates due to widespread Android smartphone adoption, while Apple CarPlay is expected to experience significant growth.”

Connected car platforms include Android Auto, CarPlay, and MirrorLink. Android Auto currently dominates the market due to the widespread adoption of Android smartphones, broad app compatibility, and ease of integration with vehicle infotainment systems. This platform allows users to access navigation, music, communication apps, and other features directly from the car’s dashboard, improving convenience and safety.

CarPlay, Apple’s platform, is the fastest-growing segment, fueled by the rising penetration of iPhones and the growing preference among consumers for iOS-compatible vehicles. MirrorLink, though still present in select models, has limited adoption due to its smaller smartphone compatibility and slower market uptake. The popularity of multi-platform infotainment systems in new vehicles reflects automakers’ efforts to cater to diverse consumer preferences, enhance in-car user experience, and drive differentiation in the competitive automotive market.

Want to get more details about the segmentations? Register Here

By Connectivity Type

“Cellular connectivity remains the dominant technology in the connected cars market, whereas DSRC is expected to experience the most rapid expansion.”

The connectivity segment is divided into cellular and DSRC. Cellular connectivity dominates the market, leveraging the widespread availability of 4G networks and the ongoing rollout of 5G technology. Cellular networks allow vehicles to communicate in real-time with cloud services, navigation platforms, fleet management systems, and infotainment apps, enabling smart, connected mobility across cities and highways.

DSRC is the fastest-growing connectivity segment, supported by government initiatives to promote vehicle-to-everything (V2X) communication and intelligent transport systems (ITS). DSRC offers low-latency, high-speed communication between vehicles, roadside infrastructure, and pedestrians, which is critical for traffic safety, congestion management, and the development of autonomous driving technologies. The growth of DSRC is expected to accelerate as smart city projects and automotive safety regulations increasingly mandate V2X-enabled infrastructure and vehicles.

Regional Analysis

“North America holds a significant share of the connected cars market, whereas the Asia-Pacific region is likely to grow at the fastest rate.”

North America currently holds the largest share of the connected cars market, supported by strong technology adoption, robust automotive infrastructure, and regulatory initiatives promoting vehicle safety. The presence of leading automakers such as General Motors, Ford, and Tesla, combined with collaborations with technology giants like Google, Apple, and Qualcomm, has created a mature connected mobility ecosystem. The U.S. is at the forefront of deploying advanced telematics, over-the-air (OTA) updates, and autonomous driving trials, fueled by extensive 4G and 5G network coverage. Additionally, government mandates such as eCall and vehicle safety standards further drive adoption across both passenger and commercial vehicles.

Asia-Pacific is emerging as the fastest-growing region in the connected cars market, with rapid growth driven by large-scale automotive production, rising consumer demand for smart mobility, and government initiatives supporting intelligent transportation systems. China, Japan, South Korea, and India are at the center of this expansion, with strong contributions from automakers like Toyota, Hyundai, Honda, and SAIC, alongside technology players such as Huawei and Baidu. The rising penetration of 5G networks, growing investments in electric vehicles (EVs), and increasing adoption of ride-sharing and mobility-as-a-service (MaaS) platforms are accelerating connected car deployments. Furthermore, supportive policies around smart cities and V2X communications are strengthening the region’s leadership in next-generation mobility.

The connected cars market is moderately consolidated. Most of the major players compete in some of the governing factors, including technology innovation, service portfolio, regional presence, and strategic partnerships. The following are the key players in the connected cars market.

Here is the list of the Top Players (Based on Alphabetical order)

Note: The above list does not necessarily include all the top players in the market.

Are you the leading player in this market? We would love to include your name. Please write to us at [email protected]

This report provides market intelligence most comprehensively. The report structure has been kept so that it offers maximum business value. It provides critical insights into market dynamics and will enable strategic decision-making for existing market players as well as those willing to enter the market. The following are the key features of the report:

The global connected cars market is segmented into the following categories.

Connected Cars Market by Service Type

Connected Cars Market, by Form Factor Type

Connected Cars Market, by Platform Type

Connected Cars Market by, Connectivity Type

Connected Cars Market by Region

With this detailed report, Stratview Research offers one of the following free customization options to our respectable clients:

Company Profiling

Competitive Benchmarking

Custom Research: Stratview Research offers custom research services across sectors. In case of any custom research requirement related to market assessment, competitive benchmarking, sourcing and procurement, target screening, and others, please send your inquiry to [email protected]

The report is delivered digitally through our online portal. Buyers receive login credentials from our team to access the report and may update their credentials at any time after the initial login.

Delivery timelines depend on the status of the report:

For the most accurate delivery timeline, please contact us to confirm the current status of the report.

Yes. You may request a complimentary preview of the report through a video conference with our team.

Yes. The scope of the report can be fully customized to align with your specific research objectives and information requirements.

Please contact us at [email protected], and our team will be happy to discuss your requirements and propose a tailored solution.

Yes. Selected sections of the report can be purchased separately based on your requirements. Please contact us at [email protected] to discuss your needs.

Yes, AI can help gather publicly available information, but its outputs are only as reliable as the data it accesses. Stratview Research reports are built using validated data, extensive primary interviews with industry stakeholders, and the expertise of our experienced research team.

Additionally, many critical insights, including market dynamics, competitive intelligence, and industry-specific trends, are not publicly available and therefore cannot be captured through AI alone.

Connected car market refers to the automotive technology segment involving vehicles equipped with internet connectivity, telematics systems, and digital services that enable communication between vehicles, infrastructure, and mobile devices, providing enhanced safety, navigation, entertainment, and fleet management capabilities.

The connected cars market is estimated to grow to reach US$ 33.9 Billion in 2032, growing from USD 12.4 billion in 2024 driven by driven by increasing adoption of advanced telematics, rising demand for in-vehicle connectivity and infotainment, rapid deployment of 5G networks, regulatory mandates for safety and eCall systems, and growing integration of electric and autonomous vehicles.

The connected cars Market is estimated to grow at a CAGR of 19.1% by 2032, driven by increasing smartphone penetration, rising consumer demand for advanced automotive technologies, government digitization initiatives, and growing emphasis on vehicle safety and connectivity features.

Key market drivers include rapidly expanding smartphone penetration, increasing consumer demand for in-vehicle entertainment and connectivity, government initiatives promoting smart mobility, growing commercial vehicle fleet management needs, rising disposable income levels, and expanding telecom infrastructure supporting vehicle connectivity solutions.

Apple Inc., BMW Group, Daimler AG (Mercedes-Benz), Ford Motor Company, General Motors, Google LLC, Hyundai Motor Company & Kia Corporation, Tesla, Inc., Toyota Motor Corporation, Volkswagen Group are the leading players in the connected cars market.

WE ACCEPT