404

+1-313-307-4176

Automotive Brake System Market Report

Automotive Brake System Market Size, Share, Trend, Forecast, Competitive Landscape & Growth Opportunities: 2025-2032

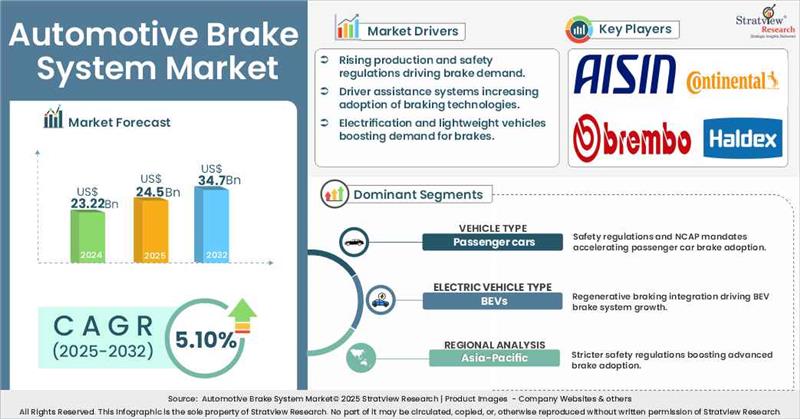

"automotive brake system market size was USD 23.22 billion in 2024.”

Want to get a free sample? Register Here

Have a look at the sales opportunities presented by the automotive brake system market in terms of growth and market forecast.

Automotive Brake System Market Data & Statistics

|

Market Statistics |

Value (in USD Billion) |

Market Growth (%) |

|

Annual Market Size in 2023 |

USD 22.18 billion |

|

|

Annual Market Size in 2024 |

USD 23.22 billion |

YoY Growth in 2024: 4.7% |

|

Annual Market Size in 2025 |

USD 24.5 billion |

YoY Growth in 2025: 5.5% |

|

Annual Market Size in 2032 |

USD 34.7 billion |

CAGR 2025-2032: 5.10% |

|

Cumulative Sales Opportunity during 2025-2032 |

USD 235.54 billion |

|

|

Top 10 Countries’ Market Share in 2024 |

USD 18.58 billion + |

> 80% |

|

Top 10 Company’s Market Share in 2024 |

USD 11.61 billion to USD 16.25 billion |

50% - 70% |

What is automotive brake system systems?

Brake systems are a critical component of vehicle safety, providing control and ensuring reduced stopping distances in both passenger and commercial vehicles. As governments worldwide implement mandates for technologies such as Anti-lock Braking Systems (ABS), Electronic Stability Control (ESC), and Automatic Emergency Braking (AEB), The automotive brake system market is poised for substantial growth driven by rising vehicle production, stringent safety regulations, and growing consumer demand for advanced driver-assistance systems (ADAS). As OEMS are integrating electronic and regenerative braking solutions into their product lines, the surge in Battery Electric Vehicles (BEVs) and hybrid models will also accelerate the demand for regenerative and brake-by-wire systems.

Stringent Government Regulations regarding road safety:

High Costs of implication:

Global Push for Mandatory AEB Systems:

|

Segmentations |

List of Sub-Segments |

Segments with High-Growth Opportunity |

|

Brake Type Analysis |

Disc Brake and Drum Brakes |

Disc Brakes is projected to be the fastest growing segment during the forecast period. |

|

Technology Type Analysis |

ABS, ESC, TCS, EBD and AEB |

Traction control system (TCS) is estimated to be the fastest growing segment during the forecast period. |

|

Vehicle Type Analysis |

Passenger Cars, Light Commercial Vehicles, Trucks, Buses |

Passenger cars are anticipated to be the fastest-growing segment for the Automotive Brake System market during the forecast period. |

|

Electric Vehicle Type Analysis |

Battery Electric Vehicles (BEVs), Plug-in Hybrid Electric Vehicles (PHEVs) |

BEVs are expected to be the dominant segment in the market during the forecast period. |

|

Regional Analysis |

North America, Europe, Asia-Pacific, South America, Middle East & Africa, and The Rest of the World |

Asia-Pacific is expected to be the dominant and fastest-growing region over the forecasted period. |

“Passenger cars segment is projected to be the fastest-growing segment during the forecast period.”

“Battery Electric Vehicles (BEVs) segment to register highest CAGR during the forecast period.”

Want to get more details about the segmentations? Register Here

“Asia Pacific is expected to be the dominant and fastest-growing region over the forecasted period.”

Most of the major players compete in some of the factors, including price, service offerings, regional presence, etc. The following are the key players in the automotive brake system market -

Note: The above list does not necessarily include all the top players in the market.

Are you a leading player in this market? We would love to include your name. Please write to us at [email protected]

This report provides market intelligence most comprehensively. The report structure has been kept so that it offers maximum business value. It provides critical insights into market dynamics and will enable strategic decision-making for existing market players as well as those willing to enter the market.

The following are the key features of the report:

|

Market Study Period |

2019-2032 |

|

Base Year |

2024 |

|

Forecast Period |

2025-2032 |

|

Trend Period |

2019-2023 |

|

Number of Tables & Figures |

>100 |

|

Number of Segments Analysed |

5 (Brake Type, Technology Type, Vehicle Type, Electric Vehicle Type and Region) |

|

Number of Regions Analysed |

4 (North America, Europe, Asia-Pacific, Rest of the World) |

|

Countries Analysed |

15 (The USA, Canada, Mexico, Germany, France, Italy, The UK, China, Japan, India, Brazil, Saudi Arabia, Rest of Europe, Rest of APAC, and Rest of the World) |

|

Free Customization Offered |

10% |

|

After Sales Support |

Unlimited |

|

Report Presentation |

Complimentary |

|

Market Dataset |

Complimentary |

|

Further Deep Dive & Consulting Services |

10% Discount |

This report studies the market, covering a period of 15 years of trend and forecast. The report provides detailed insights into the market dynamics to enable informed business decision-making and growth strategy formulation based on the opportunities present in the market.

The automotive brake system market is segmented into the following categories:

By Brake Type

By Technology Type

By Vehicle Type

By Electric Vehicle Type

By Region

With this detailed report, Stratview Research offers one of the following free customization options to our respected clients:

Company Profiling

Competitive Benchmarking

Custom Research: Stratview Research offers custom research services across industries. In case of any custom research requirement related to market assessment, competitive benchmarking, sourcing and procurement, target screening, and others, please send your inquiry to [email protected]

The report is delivered digitally through our online portal. Buyers receive login credentials from our team to access the report and may update their credentials at any time after the initial login.

Delivery timelines depend on the status of the report:

For the most accurate delivery timeline, please contact us to confirm the current status of the report.

Yes. You may request a complimentary preview of the report through a video conference with our team.

Yes. The scope of the report can be fully customized to align with your specific research objectives and information requirements.

Please contact us at [email protected], and our team will be happy to discuss your requirements and propose a tailored solution.

Yes. Selected sections of the report can be purchased separately based on your requirements. Please contact us at [email protected] to discuss your needs.

Yes, AI can help gather publicly available information, but its outputs are only as reliable as the data it accesses. Stratview Research reports are built using validated data, extensive primary interviews with industry stakeholders, and the expertise of our experienced research team.

Additionally, many critical insights, including market dynamics, competitive intelligence, and industry-specific trends, are not publicly available and therefore cannot be captured through AI alone.

The automotive brake system market comprises the technologies, components, and systems used to slow down or stop a vehicle. These systems include mechanical, hydraulic, pneumatic, and electronic components such as disc and drum brakes, ABS, ESC, and advanced safety features like AEB. Brake systems are vital for vehicle safety and performance, and their evolution is driven by technological advancements, safety regulations, and increasing vehicle production.

The forecasted value for the market is US$ 34.7 billion in 2032.

Automotive brake system market size was USD 23.22 billion in 2024 and is expected to grow from USD 24.5 billion in 2025 to USD 34.7 billion in 2032, witnessing an impressive market growth (CAGR) of 5.10% during the forecast period (2025-2032).

The key drivers of the automotive brake system market include: • Stringent vehicle safety regulations mandating ABS, ESC, and AEB systems. • Rising demand for high-performance and electric vehicles, necessitating advanced braking solutions. • Technological innovations, including electronic and regenerative braking systems. • Growing adoption of disc brakes in passenger and commercial vehicles. • Increased construction and agricultural activity, boosting demand for off-highway brake systems.

Asia-Pacific is expected to be the dominant and the fastest-growing region of the automotive brake system market over the forecasted period, led by countries like China, Japan, and India. This dominance is due to high vehicle production rates, rapid urbanization, and government initiatives enforcing stricter safety standards.

WE ACCEPT