404

+1-313-307-4176

Automotive Airbag Fabric Market Analysis | 2025-2031

Automotive Airbag Fabric Market Size, Share, Trends, Dynamics, Forecast, & Growth Analysis: 2025-2031

Automotive Airbag Fabric Market is segmented by Airbag Type (Driver Airbag, Passenger Airbag, Side Airbag, Knee Airbag, and Curtain Airbag), by Fabric Type (Flat Fabric and OPW Fabric), by Vehicle Type (Car, C/SUV, Pickup, Van, MPV, and Sports Car), by Coating Type (Coated Fabric and Uncoated Fabric), by Yarn Type (Polyamide Fabric and Polyester Fabric), and by Region (North America [The USA, Canada, and Mexico], Europe [Germany, France, The UK, Italy, Russia, and Rest of Europe], Asia-Pacific [China, Japan, India, and Rest of Asia-Pacific], and the Rest of the World [Brazil, Argentina, and Others]).

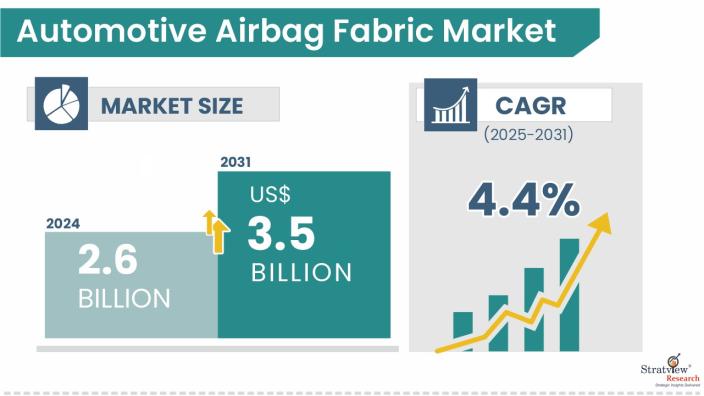

The automotive airbag fabric market size was USD 2.6 billion in 2024 and is likely to grow at a decent CAGR of 4.4% during 2025-2031 to reach USD 3.5 billion in 2031.

Wish to get a free sample? Click Here

Automotive airbag fabric refers to the specialized material used in the construction of airbags. The fabric is engineered to withstand the high forces and rapid inflation associated with airbag deployment. It is made from polyamide or polyester fibers, which are woven together to create a strong and flexible textile.

Airbags and airbag system designs have evolved significantly over the years. Despite various considerations of material options, polyamide 6.6 remains the material of choice for airbag fabrics. Performance and cost-benefit are the key drivers for using polyamide 6.6. Polyamide 6.6 has the highest capability in energy absorption. The balance between strength and elongation gives it unmatched suitability for airbags. The airbag fabrics are required to operate in a hostile environment in terms of thermal and mechanical energy absorption. Higher specific heat capacity enables polyamide 6.6 to have a higher melting point as compared to polyester. Hence, in case of an inflation event, airbags made from polyester yarn are more susceptible to melting as compared to polyamide 6.6.

Key drivers of the automotive airbag fabric market are the rising implementation of global vehicle safety regulations, increasing consumer awareness of safety features, and growing vehicle production, especially in emerging economies, such as China and India. The shift toward mandatory airbags in all vehicle types, including entry-level cars, is accelerating demand. Additionally, advancements in fabric technology for lighter, stronger, and more compact airbag systems are fueling market growth, along with the expanding adoption of side, curtain, and knee airbags for enhanced occupant protection.

Regulatory bodies such as the National Highway Traffic Safety Administration (NHTSA) in the U.S., Euro NCAP in Europe, and various Asian safety authorities are mandating the installation of airbags across all vehicle categories, including cars, trucks, and buses. This regulatory push is significantly increasing the demand for airbag systems, which in turn drives the need for high-performance and durable airbag fabrics. To ensure compliance with these stringent safety standards, manufacturers are increasingly adopting advanced airbag fabric materials that offer reliability and protection in critical crash scenarios.

A considerable number of strategic alliances, including M&As, JVs, etc., have been performed over the past few years:

In January 2023, Toray Industries, Inc. developed recycled nylon 66 recovered from silicone-coated airbag fabric scrap cuttings – Ecouse AMILAN™, which is an environmentally friendly product.

|

Segmentations |

List of Sub-Segments |

Segments with High-Growth Opportunity |

|

Airbag-Type Analysis |

Driver Airbag, Passenger Airbag, Side Airbag, Knee Airbag, and Curtain Airbag |

Curtain airbag is expected to be the dominant as well as the fastest-growing airbag type in the coming years. |

|

Fabric Range-Type Analysis |

Flat Fabric and OPW Fabric |

OPW fabric is anticipated to remain the dominant and faster-growing fabric type. |

|

Vehicle-Type Analysis |

Car, C/SUV, Pickup, Van, MPV, and Sports Car |

C/SUV is anticipated to remain the biggest demand generator for airbag fabrics in the years to come. |

|

Coating-Type Analysis |

Coated Fabric and Uncoated Fabric |

Coated fabric is expected to remain dominant, whereas uncoated fabric is estimated to see faster growth during the forecast period. |

|

Yarn-Type Analysis |

Polyamide Fabric and Polyester Fabric |

Polyamide is expected to remain the dominant yarn, whereas Polyester is estimated to be the faster-growing yarn type during the forecast period. |

|

Region Analysis |

North America, Europe, Asia-Pacific, and The Rest of the World |

The Asia-Pacific is expected to maintain its reign over the forecast period. |

“Curtain airbags are expected to remain dominant and will also be the fastest-growing in the market during the forecast period.”

Based on the airbag type, the market is segmented into driver airbag, passenger airbag, side airbag, knee airbag, and curtain airbag. Curtain airbags are highly effective in saving occupants from side-impact crashes. They are increasingly being used in developing nations, where frontal airbags already have an excellent penetration level in the automobile fleet. The penetration of curtain airbags in developed nations is significantly higher than that of developing nations like China and India. Approximately three meters of airbag fabric are used to develop one curtain airbag.

“OPW fabric accounted for the largest share in the market, and this category is also likely to register higher growth in the coming six years."

Based on the fabric type, the market is segmented into flat fabric and OPW fabric. OPW airbag fabrics have high elongation and tensile strength as compared to flat fabric, but they possess comparatively less hardness than flat fabric. The seamless nature of OPW provides increased reliability during airbag deployment and reduces the likelihood of tear or failure during airbag inflation. They are highly preferred in curtain airbags. They are engineered during the weaving stage and customized to meet the specific requirements of OEMs.

Flat fabrics are dominantly used in frontal airbags (driver and passenger airbags). All the major players in the market offer both OPW and flat fabrics.

“C/SUV is likely to remain the leading vehicle of the automotive airbag fabric market by 2031.”

Based on the vehicle type, the automotive airbag fabric market is segmented into Cars, C/SUVs, Pickups, Vans, MPVs, and Sports cars. C/SUV is expected to remain the market's largest and fastest-growing vehicle type in the market owing to increasing demand for SUVs in major Asian countries, such as China and India, and highly congested cities of the developed economies. Rising customer preference for SUVs for their several attractive features, such as spacious interiors, higher ground clearance, and a smooth & comfortable driving experience, is triggering the demand for SUVs and so on airbag fabrics. Also, the fitment rates of airbag fabrics are higher in SUVs compared to standard cars.

“Coated fabric is expected to be the dominant coating type of the market during the forecast period.”

In terms of coating type, the market is segmented into coated fabric and uncoated fabric. Coated fabric offers superior properties over uncoated fabric. Silicone elastomer is mainly used as the coating material, as opposed to neoprene, which was previously used for the same purpose. There has been an increasing usage of lightweight coating material to develop lightweight airbags and save space. Liquid silicone rubber (LSR)-coated fabrics have thermal resistance, flame resistance, high tear strength, and good adhesive properties as compared to uncoated fabric. Almost all the major automakers rely on silicone elastomer for their airbag coating applications.

Uncoated fabrics are expected to register higher growth in the coming years owing to their good tensile strength, high modulus, low shrinkage, excellent creep resistance, dimensional stability, increased flexibility, and low cost.

“Polyamide fabric is anticipated to grab a higher share in the market by 2031, whereas polyester fabric is estimated to grow at a higher pace during 2025-2031.”

In terms of yarn type, the market is segmented into polyamide fabric and polyester fabric. Polyamide 6.6 yarn is the most preferred yarn type in the market owing to its properties, such as elasticity, fatigue resistance, energy absorption, high-tensile strength and wear resistance, high tenacity, small-friction coefficient, and relative density as compared to polyester. Polyester yarn is anticipated to have a higher growth rate in the market owing to an increase in the penetration of side and curtain airbags in vehicles. Another advantage that polyester yarns bring to the table is that they have a significantly lower price than polyamide yarns.

“Asia-Pacific is expected to remain the largest market for automotive airbag fabric during the forecast period.”

In terms of region, the market is segmented into North America, Europe, Asia-Pacific, and the Rest of the World. Asia-Pacific will continue to be the largest and most influential regional market for automotive airbag fabric. The rapid expansion of light vehicle production in China and India, the growing awareness of passenger safety, and the introduction of safety standards by the respective governments are the major factors driving the growth of the region. However, the Rest of the World is expected to grow at the fastest rate, owing to upcoming assembly plants and the increasing penetration of airbags per car.

North America and Europe are also likely to create sizeable opportunities in the coming six years, driven by vehicle production growth coupled with the fitment rates of side, curtain, and knee airbags. The expected rebound in automobile production is likely to create demand for airbags along with their fabrics in the coming years.

Know the high-growth countries in this report. Register Here

The market is moderately concentrated, with the presence of some regional and global players. Most of the players are either forward-integrated or backward-integrated. Some airbag system manufacturers have a subsidiary company that manufactures their airbag cushions. Asahi Kasei Airbag Fabric Vietnam, Co., Ltd., a joint venture between Asahi Kasei Corp and Teijin Frontier to open an airbag fabric manufacturing facility with an expected capacity of 20 million square meters of fabric per year in 2024.

The following are the key players in the automotive airbag fabric market.

Here is the list of the Top Players (Based on Dominance)

Note: The above list does not necessarily include all the top players in the market.

Are you the leading player in this market? We would love to include your name. Please write to us at [email protected]

This report provides market intelligence most comprehensively. The report structure has been kept so that it offers maximum business value. It provides critical insights into market dynamics and will enable strategic decision-making for existing market players as well as those willing to enter the market. The following are the key features of the report:

This report studies the market, covering a period of 12 years of trends and forecasts. The report provides detailed insights into the market dynamics to enable informed business decision-making and growth strategy formulation based on the opportunities present in the market.

The automotive airbag fabric market is segmented into the following categories:

By Airbag Type

By Fabric Type

By Vehicle Type

By Coating Type

By Yarn Type

By Region

With this detailed report, Stratview Research offers one of the following free customization options to our respected clients:

Company Profiling

Competitive Benchmarking

Custom Research: Stratview Research offers custom research services across sectors. In case of any custom research requirement related to market assessment, competitive benchmarking, sourcing and procurement, target screening, and others, please send your inquiry to [email protected]

The report is delivered digitally through our online portal. Buyers receive login credentials from our team to access the report and may update their credentials at any time after the initial login.

Delivery timelines depend on the status of the report:

For the most accurate delivery timeline, please contact us to confirm the current status of the report.

Yes. You may request a complimentary preview of the report through a video conference with our team.

Yes. The scope of the report can be fully customized to align with your specific research objectives and information requirements.

Please contact us at [email protected], and our team will be happy to discuss your requirements and propose a tailored solution.

Yes. Selected sections of the report can be purchased separately based on your requirements. Please contact us at [email protected] to discuss your needs.

Yes, AI can help gather publicly available information, but its outputs are only as reliable as the data it accesses. Stratview Research reports are built using validated data, extensive primary interviews with industry stakeholders, and the expertise of our experienced research team.

Additionally, many critical insights, including market dynamics, competitive intelligence, and industry-specific trends, are not publicly available and therefore cannot be captured through AI alone.

Automotive airbag fabric is mainly a tough material that is durable enough and has the capability to retain its quality even after rapid inflation and impacts. Normally, nylon is the most commonly used material for an automotive airbag, but now new options are coming up to offer even better results. Automotive Airbag Fabric is chosen depending on the type of airbag and the position of the airbags in the vehicle. The demand for automotive options, especially SUVs with durable and reliable automotive airbag fabric, is continuously increasing due to the increasing number of accidents taking place on the road.

The automotive airbag fabric market is projected to reach approximately US$ 3.5 billion by 2031, driven by rising vehicle safety mandates and increasing demand for advanced restraint systems in passenger vehicles.

The automotive airbag fabric market is estimated to grow at a CAGR of 4.4% by 2031.

Asia-Pacific holds the largest share of the automotive airbag fabric market and is anticipated to continue its dominance throughout the forecast period, owing to high vehicle production, rapid urbanization, and government mandates on passenger safety in countries like China, Japan, and India.

Toray Industries, Inc., Hyosung Corporation, Kolon Industries, Inc., HMT (Xiamen) New Technical Materials Co., Ltd., and Indorama Ventures are the leading players in the market.

WE ACCEPT