404

+1-313-307-4176

Aerospace and Defense Braking Control System Market Analysis | 2025-2034

Aerospace and Defense Braking Control System Market Size, Share, Trends, Dynamics, Forecast, & Growth Analysis: 2025-2034

Aerospace and Defense Braking Control System Market is segmented by Application Type (Commercial Aircraft, Regional Aircraft, General Aviation, and Military Aircraft), by End-Use Type (OEM and Aftermarket), and by Region (North America [The USA, Canada, and Mexico]; Europe [Germany, France, The UK, Russia, and the Rest of Europe]; Asia-Pacific [China, Japan, India, and the Rest of Asia-Pacific]; and the Rest of the World [Brazil, Argentina, and Others]).

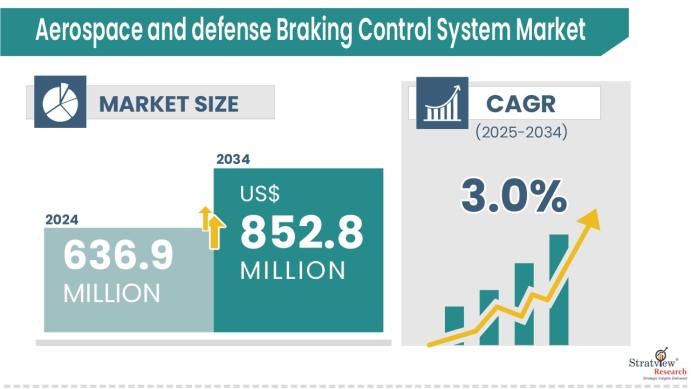

The aerospace and defense braking control system market was valued at USD 636.9 million in 2024 and is likely to grow at a CAGR of 3.0% during 2025-2034 to reach USD 852.8 million in 2034.

Want to know more about the market scope? Register Here

The aerospace and defense braking control system market plays a critical role in ensuring the safe, stable, and efficient ground operation of aircraft across commercial, military, regional, and general aviation categories. Braking control systems are responsible for regulating and optimizing braking performance during landing, taxiing, and emergency stopping conditions, helping maintain directional stability and preventing wheel skidding under varying runway and environmental conditions. With advancements in aircraft design and the growing emphasis on safety, performance, reliability, and weight reduction, braking control systems have evolved from traditional hydraulic systems to more sophisticated digital and electronically actuated solutions, including Brake-by-Wire and anti-skid braking technologies.

In addition, rising aircraft production rates, increasing global air travel, and ongoing modernization programs in defense fleets are driving the demand for advanced braking control solutions. The need for efficient braking performance under high landing loads and diverse climate conditions further reinforces the importance of braking control systems as a key component of aviation safety and operational efficiency. As a result, the aerospace and defense braking control system market continues to expand, shaped by technological innovation and the growing focus on enhanced aircraft safety and control.

|

Segmentations |

List of Sub-Segments |

Segments with High Growth Opportunity |

|

Application-Type Analysis |

Commercial Aircraft, Regional Aircraft, General Aviation, and Military Aircraft |

The commercial aircraft segment currently leads the aerospace and defense braking control system market and is expected to maintain its dominance, experiencing the highest growth during the forecast period. |

|

End-Use-Type Analysis |

OEM and Aftermarket |

While the aftermarket category currently dominates the market, OEM is projected to experience higher growth in the coming period. |

|

Region Analysis |

North America, Europe, Asia-Pacific, and The Rest of the World |

Asia-Pacific is set to witness robust growth in the years ahead, with North America retaining its dominant market share. |

“The commercial aircraft represents the widely used application category of the aerospace and defense braking control system market.”

The market is segmented into commercial aircraft, regional aircraft, general aviation, and military aircraft. The commercial aircraft segment holds the largest share of the aerospace and defense braking control system market primarily due to the large size of the global commercial fleet and the continuous rise in air passenger traffic worldwide. Airlines are actively expanding and modernizing their fleets to enhance fuel efficiency, safety, and operational performance, which drives the adoption of advanced, digitally integrated braking control technologies. Additionally, commercial aircraft experience high numbers of take-off and landing cycles, increasing the demand for reliable braking control systems that ensure precise deceleration, anti-skid performance, and runway stability under varying operating conditions. The frequent maintenance, inspection, and system upgrades required to support such intensive usage further contribute to strong aftermarket demand. As a result, the scale of fleet operations, high utilization rates, and ongoing need for system reliability and servicing collectively reinforce the commercial aircraft segment’s dominant position in the aerospace and defense braking control system market.

“The aftermarket category currently dominates the aerospace and defense braking control system market, primarily due to frequent maintenance & replacement requirements in the legacy aircraft.”

Based on end-use, the market is categorized into OEM and aftermarket. The aftermarket segment currently leads the aerospace and defense braking control system market due to the ongoing need for maintenance, repair, overhaul, and periodic replacement of braking control components in active aircraft fleets. Braking control systems operate under frequent high-stress conditions during landing, taxiing, and runway operations, which can lead to wear in sensors, valves, actuators, and electronic control modules over time. As global air travel continues to recover and fleets remain in service longer, airlines and defense operators must regularly service and upgrade these systems to maintain safety, performance, and regulatory compliance. Meanwhile, although the OEM segment is smaller in comparison, it is expected to grow steadily as aircraft production accelerates, and newer platforms increasingly integrate advanced digital braking control technologies for improved precision, lighter weight, and enhanced energy efficiency. This combination of sustained aftermarket activity and rising OEM demand is shaping the long-term growth trajectory of the braking control system market.

“Asia-Pacific is expected to experience the highest growth in the coming years, driven by increasing air passenger traffic and expanding commercial fleets.”

North America continues to lead the aerospace and defense braking control system market due to the strong concentration of major aircraft manufacturers and established braking system suppliers in the region. The region’s mature aerospace supply chain, high levels of commercial and defense aviation activity, and continuous investments in advanced braking control technologies such as digital brake control units and electronically actuated braking systems further strengthen its dominant position. In contrast, the Asia-Pacific region is projected to witness the fastest growth, supported by expanding aircraft production, rapid growth in airline fleets, and increasing passenger traffic. Therefore, while North America maintains its leadership in technology and market share, Asia-Pacific is expected to record the highest growth during the forecast period.

Know the high-growth countries in this report. Register Here

The market is highly concentrated, with only a few players across the region. Most of the major players compete in some of the governing factors, including price, service offerings, regional presence, etc. The following are the key players in the aerospace and defense braking control system market. Some of the major players provide a complete range of services.

Here is the list of the Top Players (Based on Dominance)

Note: The above list does not necessarily include all the top players in the market.

Are you the leading player in this market? We would love to include your name. Please write to us at [email protected]

This report provides market intelligence most comprehensively. The report structure has been kept so that it offers maximum business value. It provides critical insights into market dynamics and will enable strategic decision-making for existing market players as well as those willing to enter the market. The following are the key features of the report:

This report studies the market, covering a period of 12 years of trends and forecasts. The report provides detailed insights into the market dynamics to enable informed business decision-making and growth strategy formulation based on the opportunities present in the market.

The aerospace and defense braking control system market is segmented into the following categories.

By Application Type

By End-Use Type

By Region

With this detailed report, Stratview Research offers one of the following free customization options to our respected clients:

Company Profiling

Competitive Benchmarking

Custom Research: Stratview Research offers custom research services across industries. In case of any custom research requirement related to market assessment, competitive benchmarking, sourcing and procurement, target screening, and others, please send your inquiry to [email protected].

The report is delivered digitally through our online portal. Buyers receive login credentials from our team to access the report and may update their credentials at any time after the initial login.

Delivery timelines depend on the status of the report:

For the most accurate delivery timeline, please contact us to confirm the current status of the report.

Yes. You may request a complimentary preview of the report through a video conference with our team.

Yes. The scope of the report can be fully customized to align with your specific research objectives and information requirements.

Please contact us at [email protected], and our team will be happy to discuss your requirements and propose a tailored solution.

Yes. Selected sections of the report can be purchased separately based on your requirements. Please contact us at [email protected] to discuss your needs.

Yes, AI can help gather publicly available information, but its outputs are only as reliable as the data it accesses. Stratview Research reports are built using validated data, extensive primary interviews with industry stakeholders, and the expertise of our experienced research team.

Additionally, many critical insights, including market dynamics, competitive intelligence, and industry-specific trends, are not publicly available and therefore cannot be captured through AI alone.

The aerospace and defense braking control system market is estimated to be valued at US$ 852.8 million in 2034.

The aerospace and defense braking control system market is estimated to grow at a CAGR of 3.0% by 2034.

The global demand for braking control systems is driven by the growing aircraft fleet size, increasing flight frequency, and the need for enhanced safety and precise braking performance in both commercial and defense aviation.

North America is the largest market in the braking control system industry and is expected to maintain its share, mainly due to the strong presence of major aircraft manufacturers, established aerospace infrastructure, and ongoing investments in advanced braking and safety technologies.

Collins Aerospace, Honeywell International Inc., Meggitt PLC (part of Parker Hannifin Corp.), and Safran are the leading players in the market.

WE ACCEPT