404

+1-313-307-4176

Zero Liquid Discharge Systems Market Analysis | 2025-2032

Zero Liquid Discharge Systems Market Size, Share, Trends, Dynamics, Forecast, & Growth Analysis: 2025-2032

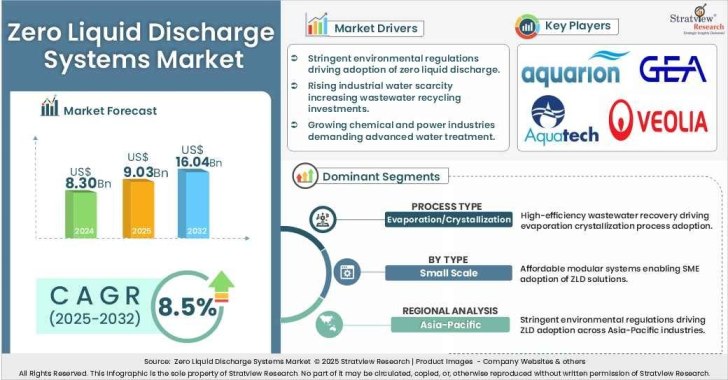

"Zero liquid discharge systems market size was USD 8.30 billion in 2024.”

Wish to get a free sample report? Click Here

Have a look at the sales opportunities presented by the zero liquid discharge systems market in terms of growth and market forecast.

|

Zero Liquid Discharge Systems Market Data & Statistics |

||

|

Market Statistics |

Value (in USD Billion) |

Market Growth (%) |

|

Annual Market Size in 2023 |

USD 7.68 billion |

- |

|

Annual Market Size in 2024 |

USD 8.30 billion |

YoY Growth in 2024: 8.1% |

|

Annual Market Size in 2025 |

USD 9.03 billion |

YoY Growth in 2025: 8.8% |

|

Annual Market Size in 2032 |

USD 16.04 billion |

CAGR 2025-2032: 8.5% |

|

Cumulative Sales Opportunity during 2025-2032 |

USD 98.26 billion |

- |

|

Top 10 Countries’ Market Share in 2024 |

USD 6.6 + |

> 80% |

|

Top 10 Company’s Market Share in 2024 |

USD 4.1 billion to USD 5.8 billion |

50% - 70% |

Zero Liquid Discharge (ZLD) systems are advanced wastewater treatment solutions designed to eliminate all liquid waste from industrial processes. They recover and recycle water while converting contaminants into solid waste. This helps industries meet strict environmental regulations, reduce water consumption, and promote sustainable operations, especially in water-scarce regions.

Zero liquid discharge systems are witnessing increasing adoption across water-intensive industries due to their ability to achieve near-complete wastewater recovery and eliminate liquid effluents. Industries such as power generation, chemicals, textiles, and pharmaceuticals are increasingly deploying ZLD solutions for wastewater treatment, reuse, and regulatory compliance, driven by strong market demand for efficient water management and discharge minimization. A key market trend shaping the industry is the shift toward circular water management and sustainability-focused operations, which is accelerating the deployment of zero liquid discharge systems globally

Stringent Environmental Regulations and Discharge Norms

Stringent wastewater discharge regulations are increasing the adoption of zero liquid discharge (ZLD) systems across industries such as power generation, chemicals, textiles, and pharmaceuticals. As governments strengthen environmental compliance requirements and freshwater protection measures, demand for ZLD systems is supporting zero liquid discharge systems market growth.

Rising Water Scarcity and Industrial Water Reuse Requirements

Increasing freshwater stress is driving industries toward wastewater recovery and reuse to reduce dependence on limited water resources. Zero liquid discharge systems are being adopted to maximize water recovery and treat wastewater as a reusable input, supporting zero liquid discharge systems market demand amid rising water scarcity and climate variability.

High Energy Consumption and Carbon Footprint

Zero liquid discharge systems rely heavily on energy-intensive processes such as thermal evaporation and crystallization, which significantly increase operating costs and carbon emissions. This makes adoption challenging, particularly for small and medium-sized industries with limited sustainability budgets, thereby restraining wider zero liquid discharge systems market growth.

Limited Technical Expertise and Skilled Workforce

The implementation and operation of zero liquid discharge systems require advanced technical expertise in membrane filtration, thermal processing, and chemical treatment technologies. A shortage of skilled professionals can delay project deployment, increase maintenance challenges, and reduce overall system efficiency.

Technological Advancements in Energy-Efficient and Modular ZLD Solutions

Advancements in membrane technologies, hybrid treatment systems, heat recovery, and modular plant designs are improving the efficiency and cost-effectiveness of zero liquid discharge systems. These innovations are reducing energy consumption and lifecycle costs while expanding the applicability of ZLD solutions across diverse industrial sectors, thereby shaping a key zero liquid discharge systems market trend.

Growing Industrial Expansion in Emerging Economies

Rapid industrialization across emerging economies is generating large volumes of industrial wastewater, increasing the need for advanced treatment and reuse solutions. Water-stressed countries are increasingly prioritizing circular water management strategies, creating strong demand for zero liquid discharge systems and contributing to the expansion of the ZLD market size.

|

Segmentations |

List of Sub-Segments |

Segments with High-Growth Opportunity |

|

Process Analysis |

Pretreatment, Filtration, and Evaporation/Crystallization |

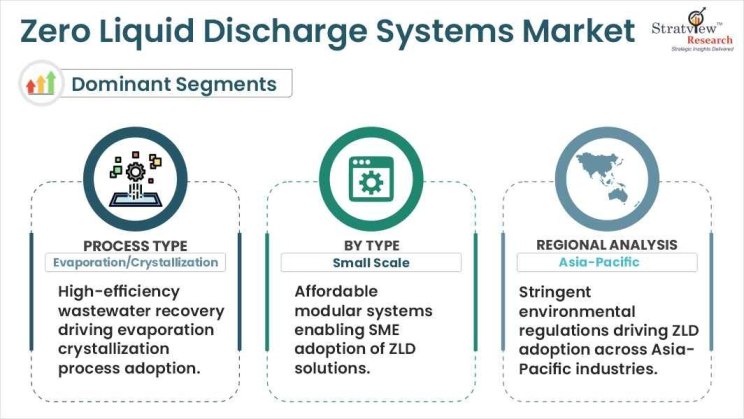

Evaporation/Crystallization segment is anticipated to have the largest share of this market in the coming years. |

|

Capacity Analysis |

Small Scale, Medium Scale, and Large Scale |

Small Scale segment is expected to be the fastest-growing segment during the forecast period. |

|

System Analysis |

Conventional and Hybrid |

Hybrid segment is projected to be the fastest-growing segment during the forecast period. |

|

End-Use Industry |

Energy & Power, Chemicals & Petrochemicals, Food & Beverages, Textiles, Pharmaceuticals, Semiconductors & Electronics, and Others |

Energy & Power segment is projected to be the fastest-growing segment during the forecast period. |

|

Regional Analysis |

North America, Europe, Asia-Pacific, and The Rest of the World |

Asia-Pacific is expected to be the dominant and fastest-growing region over the forecasted period. |

“Evaporation/Crystallization segment is anticipated to have the largest share of this market in the coming years.”

“Small Scale segment is expected to be the fastest-growing segment during the forecast period.”

Want to get more details about the segmentations? Register Here

“Asia-Pacific is expected to be the dominant and the fastest-growing region over the forecasted period.”

Most of the major players compete in some of the factors, including price, service offerings, regional presence, etc. The following are the key players in the zero liquid discharge systems market:

Note: The above list does not necessarily include all the top players in the market.

Are you a leading player in this market? We would love to include your name. Please write to us at [email protected]

This report provides market intelligence most comprehensively. The report structure has been kept so that it offers maximum business value. It provides critical insights into market dynamics and will enable strategic decision-making for existing market players as well as those willing to enter the market.

The following are the key features of the report:

|

Market Study Period |

2019-2032 |

|

Base Year |

2024 |

|

Forecast Period |

2025-2032 |

|

Trend Period |

2019-2023 |

|

Number of Tables & Figures |

>100 |

|

Number of Segments Analysed |

5 (Process Type, System Type, Capacity Type, End-Use Type, and Region) |

|

Number of Regions Analysed |

4 (North America, Europe, Asia-Pacific, Rest of the World) |

|

Countries Analysed |

15 (The USA, Canada, Mexico, Germany, France, Italy, The UK, China, Japan, India, Brazil, Saudi Arabia, Rest of Europe, Rest of APAC, and Rest of the World) |

|

Free Customization Offered |

10% |

|

After Sales Support |

Unlimited |

|

Report Presentation |

Complimentary |

|

Market Dataset |

Complimentary |

|

Further Deep Dive & Consulting Services |

10% Discount |

This report studies the market, covering a period of 15 years of trend and forecast. The report provides detailed insights into the market dynamics to enable informed business decision-making and growth strategy formulation based on the opportunities present in the market.

The zero liquid discharge systems market is segmented into the following categories.

By Process Type

By Capacity Type

By System Type

By Application Type

By End-Use Industry Type

By Region

With this detailed report, Stratview Research offers one of the following free customization options to our respectable clients:

Company Profiling

Competitive Benchmarking

Custom Research: Stratview Research offers custom research services across sectors. In case of any custom research requirement related to market assessment, competitive benchmarking, sourcing and procurement, target screening, and others, please send your inquiry to [email protected].

The report is delivered digitally through our online portal. Buyers receive login credentials from our team to access the report and may update their credentials at any time after the initial login.

Delivery timelines depend on the status of the report:

For the most accurate delivery timeline, please contact us to confirm the current status of the report.

Yes. You may request a complimentary preview of the report through a video conference with our team.

Yes. The scope of the report can be fully customized to align with your specific research objectives and information requirements.

Please contact us at [email protected], and our team will be happy to discuss your requirements and propose a tailored solution.

Yes. Selected sections of the report can be purchased separately based on your requirements. Please contact us at [email protected] to discuss your needs.

Yes, AI can help gather publicly available information, but its outputs are only as reliable as the data it accesses. Stratview Research reports are built using validated data, extensive primary interviews with industry stakeholders, and the expertise of our experienced research team.

Additionally, many critical insights, including market dynamics, competitive intelligence, and industry-specific trends, are not publicly available and therefore cannot be captured through AI alone.

The forecasted value for the market is US$16.04 billion in 2032.

Aquatech International, Veolia, GEA Group AG, Alfa Laval AB, Praj Industries are the leading players in the market.

Asia-Pacific is estimated to remain dominant in the market in the foreseeable future due to rapid industrialization, escalating water scarcity concerns, and stringent environmental regulations fostering the adoption of sustainable water management solutions.

The energy & power sector's vast scale and resource-intensive nature make ZLD systems particularly relevant, as they allow for the sustainable management of water resources, reduce the environmental impact of power generation, and align with the global shift towards more responsible industrial practices. As a result, the dominance of ZLD systems in the energy & power sector reflects a proactive commitment to both regulatory compliance and sustainable resource management.

WE ACCEPT