404

+1-313-307-4176

Rubber Processing Chemicals Market Analysis | 2024-2032

Rubber Processing Chemicals Market Size, Share, Trends, Dynamics, Forecast, & Growth Analysis: 2024-2032

Rubber Processing Chemicals Market is segmented by Product Type (Anti-degradants, Accelerators, Flame Retardants, Processing Aid/ Promoters, and Others), by Application Type (Tire and Non-Tire), and by Region (North America [The USA, Canada, and Mexico], Europe [Germany, France, The UK, Russia, and Rest of Europe], Asia-Pacific [China, Japan, India, and Rest of Asia-Pacific], and Rest of the World [Brazil, Saudi Arabia, and Others]).

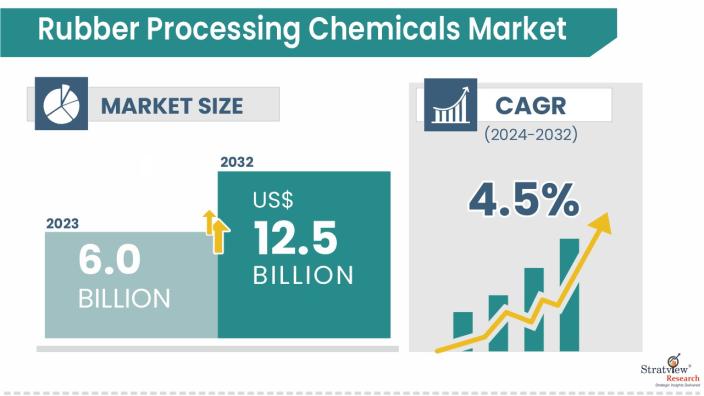

The rubber processing chemicals market size was USD 6.0 billion in 2023 and is likely to grow at a CAGR of 4.5% during 2024-2032 to reach USD 12.5 billion in 2032.

Want to get a free sample? Register Here

The rubber processing chemicals market is witnessing steady growth, driven by rising electric vehicle production, expanding infrastructure development, and increasing industrial manufacturing activities. Growing demand for high-performance tires and industrial rubber products is supporting the consumption of specialty rubber processing chemicals across automotive and industrial applications. A key trend shaping the market is the development of sustainable and bio-based rubber chemicals to meet evolving environmental regulations and circular economy objectives.

Rising EV Production is Expanding Market Share

The rising production of electric vehicles is expanding the market share of the rubber processing chemicals market. Increasing demand for high-performance tires and rubber components is driving the use of rubber processing chemicals that enhance durability, heat resistance, and rolling efficiency.

Expanding Infrastructure Development is Driving Market Growth

Expanding infrastructure development is driving the growth of the rubber processing chemicals market. Increasing investments in transportation, utilities, and industrial facilities are boosting demand for rubber products such as conveyor belts, hoses, seals, and roofing membranes.

Industrial Manufacturing Growth is Driving Market Demand

Industrial manufacturing growth is driving demand in the rubber processing chemicals market. Expanding activity across mining, energy, logistics, and heavy equipment industries is increasing the consumption of industrial rubber products requiring high-performance processing chemicals.

Stringent Chemical Regulations Restrain Market Growth

Stringent chemical regulations are restraining the growth of the rubber processing chemicals market. Increasing environmental and safety requirements are raising compliance costs and requiring manufacturers to reformulate products to meet evolving regulatory standards.

Environmental and Sustainability Pressures Challenge Market Demand

Environmental and sustainability pressures are challenging demand in the rubber processing chemicals market. Stricter requirements for emissions, waste management, and chemical safety are encouraging manufacturers to adopt more sustainable production practices while increasing operational costs.

Feedstock and Energy Cost Volatility Challenges Market Growth

Feedstock and energy cost volatility is challenging the growth of the rubber processing chemicals market. Dependence on petrochemical raw materials exposes manufacturers to fluctuations in energy prices and feedstock availability, affecting production costs and profitability.

Continued EV Market Expansion is Emerging as a Key Market Trend

Continued expansion of the electric vehicle market is emerging as a key trend in the rubber processing chemicals market. Growing production of EVs is creating opportunities for advanced rubber compounds used in tires, battery insulation systems, vibration control components, and sealing applications.

Development of Sustainable and Bio-Based Rubber Chemicals Strengthens Market Forecast

The development of sustainable and bio-based rubber chemicals is strengthening the market forecast for the rubber processing chemicals market. Increasing emphasis on sustainable materials is encouraging innovation in environmentally safer processing chemicals that support regulatory compliance and circular economy initiatives.

Growing Demand for Industrial Rubber Applications is Creating New Market Opportunities

Growing demand for industrial rubber applications is creating new opportunities in the rubber processing chemicals market. Expanding use of industrial rubber products across mining, logistics, renewable energy, and manufacturing is increasing demand for specialty rubber processing chemicals that enhance durability, wear resistance, and processing performance.

|

Segmentations |

List of Sub-Segments |

Segments with High Growth Opportunity |

|

Product-Type Analysis |

Anti-degradants, Accelerators, Flame Retardants, Processing Aids/Promoters, and Others |

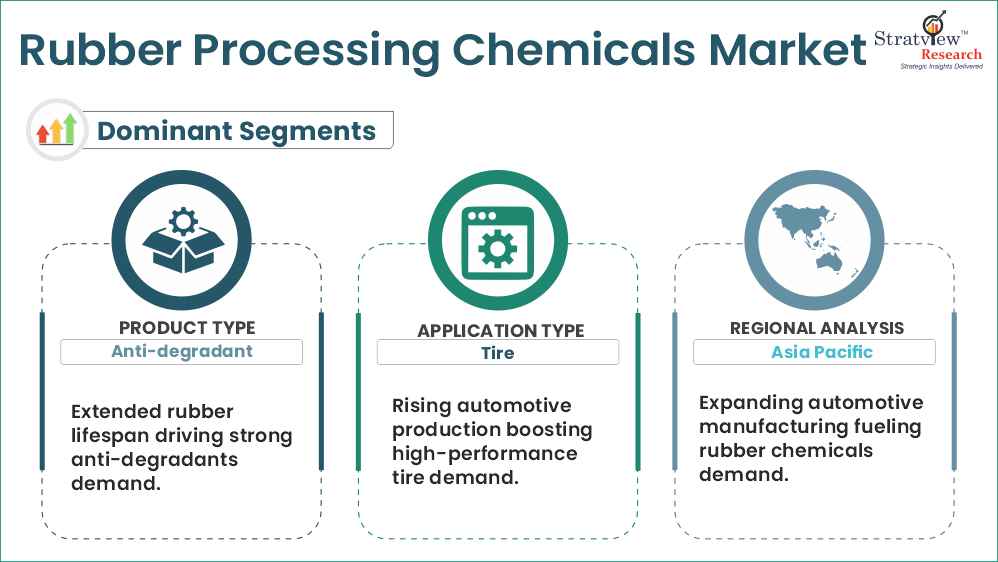

The anti-degradants segment led the market, accounting for 50% of the total share in 2023. Anti-degradants protect rubber from degradation caused by oxygen, ozone, and other environmental factors. This segment is expected to continue growing due to its critical role in enhancing the lifespan of rubber products. |

|

Application-Type Analysis |

Tire and Non-Tire |

The tire application represents the largest share of the market, with the tire manufacturing industry being the biggest consumer of rubber processing chemicals. Growing automotive production, combined with an increasing emphasis on fuel-efficient and durable tires, is boosting the demand for specialized chemicals. |

|

Region Analysis |

North America, Europe, Asia-Pacific, and The Rest of the World |

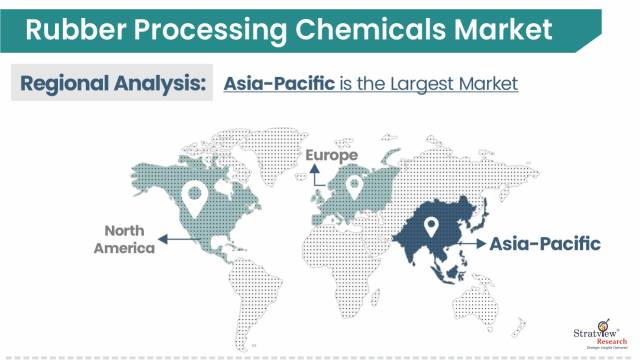

Asia-Pacific leads the global market, driven by high automotive production and industrial growth in countries like China, India, and Japan. The presence of large tire manufacturers and increasing demand for industrial rubber products are further boosting the market. |

“The anti-degradants segment dominates the rubber processing chemical market, with a share of over 50% in 2023. These chemicals protect rubber from oxidative degradation, ozone exposure, and other environmental stressors, which extends the lifespan of rubber products.”

“The tire application dominates the rubber processing chemical market, driven by the automotive industry, which is the largest consumer of rubber processing chemicals.”

Want to get more details about the segmentations? Register Here

“Asia-Pacific is the largest and fastest-growing market for rubber processing chemicals, driven by strong demand from the automotive and industrial industries.”

Also, North America is a well-established market with a high demand for sustainable and high-performance rubber processing chemicals. The region's automotive and industrial industries are key drivers of this demand, particularly for durable and environmentally friendly rubber products.

Know the high-growth countries in this report. Register Here

The market is highly fragmented with the presence of over 500 players across the region. Most of the major players compete in some of the governing factors, including price, service offerings, regional presence, etc. The following are the key players in the rubber processing chemicals market. Some of the major players are providing a complete range of rubber processing chemicals.

Here is the list of the Top Players (Based on Dominance)

Note: The above list does not necessarily include all the top players of the market.

Are you the leading player in this market? We would love to include your name. Write to us at [email protected]

A decent number of strategic alliances including M&As, JVs, etc. have been performed over the past few years:

This report provides market intelligence most comprehensively. The report structure has been kept such that it offers maximum business value. It provides critical insights into market dynamics and will enable strategic decision-making for existing market players as well as those willing to enter the market. The following are the key features of the report:

This report studies the market, covering a period of 12 years of trends and forecasts. The report provides detailed insights into the market dynamics to enable informed business decision-making and growth strategy formulation based on the opportunities present in the market.

The rubber processing chemical market is segmented into the following categories.

By Product Type

By Application Type

By Region

With this detailed report, Stratview Research offers one of the following free customization options to our respectable clients:

Company Profiling

Competitive Benchmarking

Custom Research: Stratview Research offers custom research services across sectors. In case of any custom research requirement related to market assessment, competitive benchmarking, sourcing and procurement, target screening, and others, please send your inquiry to [email protected]

The report is delivered digitally through our online portal. Buyers receive login credentials from our team to access the report and may update their credentials at any time after the initial login.

Delivery timelines depend on the status of the report:

For the most accurate delivery timeline, please contact us to confirm the current status of the report.

Yes. You may request a complimentary preview of the report through a video conference with our team.

Yes. The scope of the report can be fully customized to align with your specific research objectives and information requirements.

Please contact us at [email protected], and our team will be happy to discuss your requirements and propose a tailored solution.

Yes. Selected sections of the report can be purchased separately based on your requirements. Please contact us at [email protected] to discuss your needs.

Yes, AI can help gather publicly available information, but its outputs are only as reliable as the data it accesses. Stratview Research reports are built using validated data, extensive primary interviews with industry stakeholders, and the expertise of our experienced research team.

Additionally, many critical insights, including market dynamics, competitive intelligence, and industry-specific trends, are not publicly available and therefore cannot be captured through AI alone.

Rubber processing chemicals are key components in the manufacturing and optimization of rubber products. These chemicals are crucial in enhancing the physical, chemical, and mechanical characteristics of rubber, increasing its durability, flexibility, and resistance to environmental factors like heat, UV rays, ozone, and chemical exposure. By using these chemicals, manufacturers ensure that rubber products meet the necessary performance standards across various sectors, including automotive, industrial, and consumer goods.

The rubber processing chemicals market is projected to grow significantly, with forecasts suggesting it could reach approximately USD 12.5 billion by 2032. This growth is driven by increasing demand from the automotive sector, especially in tire manufacturing, rising industrial applications, and developing eco-friendly rubber chemicals.

The rubber processing chemicals market is anticipated to experience a CAGR of 4.5% over the coming years. This growth rate reflects the increasing demand from key sectors such as automotive, industrial applications, and consumer goods.

The key drivers of the market include the growing demand from the automotive industry, particularly for durable and high-performance tires, rapid industrialization and infrastructure development requiring advanced rubber products, and increasing consumer demand for durable goods.

Asia-Pacific holds the largest market share for rubber processing chemicals. This dominance is driven by the region's extensive automotive manufacturing base, particularly in economies such as China, India, and Japan, as well as rapid industrialization and urbanization.

The Asia-Pacific region also demonstrates the most significant market growth for rubber processing chemicals, driven by swift industrialization, a surge in automotive production, and a growing need for rubber products.

Lanxess, Solvay, Akzo Nobel N.V., BASF SE, Arkema, Eastman Chemical Company, R.T. Vanderbilt Holding Company, Inc., Behn Meyer, KUMHO PETROCHEMICAL, Paul & Company are the leading players in the market.

China holds the largest market share for rubber processing chemicals. Its prominent role as a global center for automotive manufacturing and industrial production results in high demand for rubber products, especially tires and industrial components, cementing its leading position in the market.

WE ACCEPT