404

+1-313-307-4176

Green Hydrogen Market Analysis | 2025-2032

Green Hydrogen Market Size, Share, Trends, Dynamics, Forecast, & Growth Analysis: 2025-2032

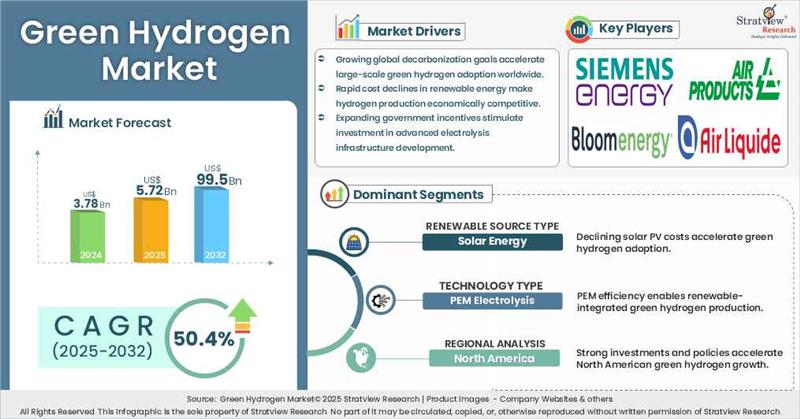

"Green hydrogen market size was USD 3.78 billion in 2024."

Want to get a free sample? Register Here

High-Growth Market Segments:

Have a look at the sales opportunities presented by the green hydrogen market in terms of growth and market forecast.

|

Green Hydrogen Market Data & Statistics |

||

|

Market Statistics |

Value (in USD Billion) |

Market Growth (%) |

|

Annual Market Size in 2023 |

USD 2.53 billion |

- |

|

Annual Market Size in 2024 |

USD 3.78 billion |

YoY Growth in 2024: 49.5% |

|

Annual Market Size in 2025 |

USD 5.72 billion |

YoY Growth in 2025: 51.2% |

|

Annual Market Size in 2032 |

USD 99.50 billion |

CAGR 2025-2032: 50.4% |

|

Cumulative Sales Opportunity during 2025-2032 |

USD 286.60 billion |

|

|

Top 10 Countries’ Market Share in 2024 |

USD 3.02 billion + |

> 80% |

|

Top 10 Company’s Market Share in 2024 |

USD 1.89 billion to USD 2.64 billion |

50% - 70% |

Government Decarbonization Policies and Net-Zero Targets

Governments are directly driving green hydrogen demand by creating regulatory mandates, subsidies, and national targets that convert long-term net-zero commitments into funded projects and procurement pipelines. This policy push is accelerating project announcements, electrolyzer deployment, and early-stage offtake agreements across industrial sectors.

For instance, according to the International Energy Agency (IEA), more than 60 governments have adopted hydrogen strategies, many of which include production targets, financial incentives, and sector-specific mandates that are expected to unlock large-scale investment in low-emission hydrogen infrastructure.

Rapid Growth in Renewable Energy Capacity Reducing Production Costs

The expansion of low-cost solar and wind power is directly improving the cost competitiveness of green hydrogen by lowering the most critical input cost in electrolysis, electricity. As renewable tariffs decline and capacity factors improve in high-resource regions, more projects are becoming economically viable and moving closer to investment decisions.

The International Energy Agency (IEA) estimates that hydrogen produced from renewable electricity could see production cost reductions of around 30% by 2030, driven by cheaper renewable generation and scaling electrolyzer deployment, which together enhance project feasibility and support wider commercialization.

Rising Industrial Demand for Clean Fuels and Energy Security

Industrial sectors are increasingly adopting green hydrogen market demand is strengthening as industries shift away from fossil-based fuels to reduce emissions and enhance long-term energy security across global supply chains, particularly in energy-intensive sectors such as refining, ammonia, steel, and chemicals.

According to the International Energy Agency (IEA), global hydrogen demand reached nearly 100 million tonnes in 2024, growing at around 2% year-over-year, with consumption primarily driven by refining, ammonia production, and steel manufacturing applications.

High Production Costs Compared to Fossil-Based Hydrogen

High production costs continue to limit the commercial competitiveness of green hydrogen, particularly in industrial sectors where conventional hydrogen remains significantly cheaper and more widely available. The market is highly sensitive to renewable power pricing, as electricity remains the single largest cost component in hydrogen production through electrolysis.

The International Energy Agency reports that unsubsidized green hydrogen production costs typically range between USD 2.50 and USD 5.00 per kg, with renewable electricity prices accounting for nearly 60% to 70% of the final production cost. Although alkaline electrolyzer systems generally range between USD 500 and USD 800/kW, Chinese-manufactured systems have reduced costs further to nearly USD 300–400/kW in some cases, helping improve project economics in large-scale deployments.

Proton Exchange Membrane (PEM) electrolyzers remain comparatively expensive at around USD 800–1,100/kW due to the use of precious metal catalysts and more complex operating systems, which continues to increase overall capital expenditure for advanced green hydrogen projects.

Infrastructure and Storage Limitations

Limited hydrogen transport, storage, and distribution infrastructure continues to remain a major barrier to large-scale green hydrogen commercialization, particularly for long-distance trade and industrial deployment. The lack of dedicated hydrogen pipelines, storage facilities, and refueling networks is slowing project scalability across multiple regions.

Hydrogen transportation, liquefaction, and conversion into carriers such as ammonia remain highly energy-intensive and expensive, increasing overall supply chain costs and limiting cross-border trade competitiveness.

Project Delays and Uncertain Demand Economics

Despite strong project announcements globally, a significant share of green hydrogen capacity remains in the early planning stage due to financing challenges and weak long-term demand visibility. Uncertainty surrounding offtake agreements and future hydrogen pricing continues to delay investment decisions across large-scale projects.

The International Energy Agency (IEA) estimates that only around 20 GW of global electrolyzer project capacity has reached final investment decision (FID) despite a substantially larger announced pipeline, reflecting persistent bankability and commercial viability concerns.

Strong Government Incentives and Hydrogen Strategies

Government-backed incentives, tax credits, and national hydrogen missions are accelerating investments across the green hydrogen value chain by improving project economics and supporting large-scale commercialization efforts. The current green hydrogen market trend is increasingly shaped by policy-led funding mechanisms aimed at scaling domestic production capacity and reducing dependence on fossil fuel-based hydrogen.

The U.S. Department of Energy’s Hydrogen Shot initiative aims to reduce clean hydrogen production costs to USD 1/kg within a decade, supporting long-term market expansion and encouraging private-sector investment in hydrogen production and infrastructure development.

Growing Decarbonization Demand from Heavy Industries and Transport

Rising pressure to reduce industrial emissions and transition toward cleaner fuels is increasing green hydrogen adoption across hard-to-abate sectors such as steel, refining, fertilizers, shipping, aviation, and heavy-duty transportation. The green hydrogen market forecast remains strongly linked to the pace of industrial decarbonization, as heavy industries continue evaluating low-emission hydrogen as a long-term alternative to fossil-based feedstocks and fuels.

According to the International Energy Agency (IEA), global hydrogen demand reached nearly 100 million tonnes in 2024. However, low-emission hydrogen production remains extremely limited at around 1 million tonnes, indicating that more than 99% of global hydrogen supply is still produced from unabated fossil fuels.

Based on projects that have already reached Final Investment Decision (FID) or are operational, low-emission hydrogen demand is projected to reach approximately 4.2 million tonnes by 2030, representing a fivefold increase from current levels, although it would still account for only around 4% of the global hydrogen market.

|

Segmentations |

List of Sub-Segments |

Segments with High-Growth Opportunity |

|

Renewable Source Analysis |

Wind Energy, Solar Energy, and Other Renewable Sources |

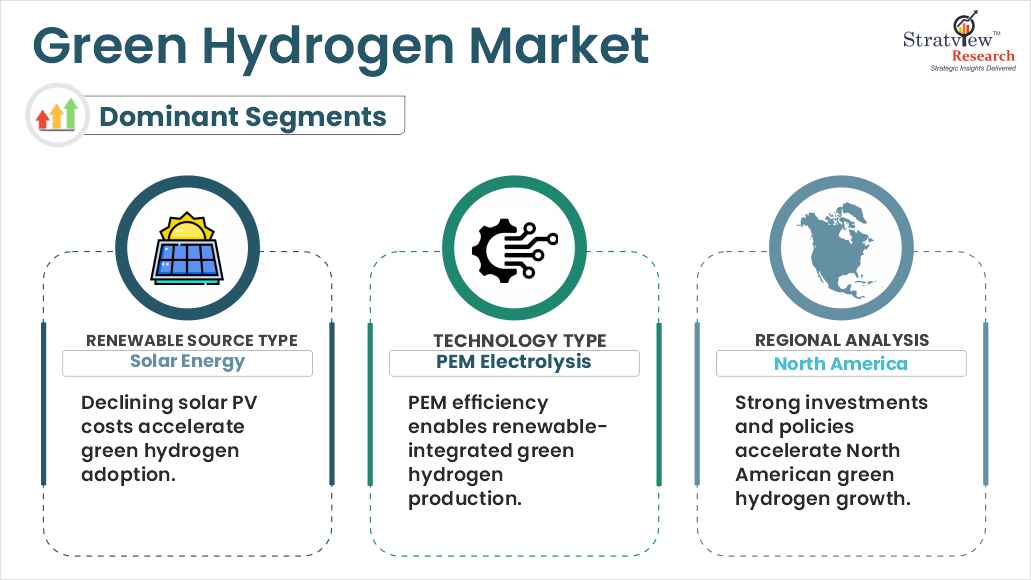

Solar Energy segment is projected to be the fastest-growing segment of this market during the forecast period. |

|

Technology Analysis |

Alkaline Electrolysis and PEM Electrolysis |

PEM Electrolysis segment is projected to be the fastest-growing segment of this market during the forecast period. |

|

End-Use Analysis |

Mobility, Chemical, Power, Grid Junction, and Industrial |

Mobility segment accounted for the largest share of green hydrogen market. |

|

Regional Analysis |

North America, Europe, Asia-Pacific, and The Rest of the World |

North America is expected to be the dominant and fastest-growing region over the forecasted period. |

“Solar Energy segment is projected to be the fastest-growing segment of this market during the forecast period.”

The green hydrogen market is segmented into wind energy, solar energy, and other renewable sources.

Solar Energy segment is projected to be the fastest-growing segment of this market during the forecast period. The rapid decline in solar photovoltaic (PV) costs has made solar-powered electrolysis increasingly cost-effective for hydrogen production.

Moreover, governments and private players are increasingly investing in solar-hydrogen initiatives, supported by favorable policies, tax incentives, and infrastructure development plans aimed at achieving net-zero emissions.

“PEM Electrolysis segment is projected to be the fastest-growing segment of this market during the forecast period.”

The green hydrogen market is segmented into alkaline electrolysis and PEM electrolysis.

PEM Electrolysis segment is projected to be the fastest-growing segment of this market during the forecast period, due to its high efficiency, rapid response times, and compatibility with renewable energy sources. PEM electrolyzers can function optimally under varying loads and are thus well-suited for integration with intermittent renewables such as solar and wind power.

Additionally, advancements in PEM technology have led to cost reductions and improved durability, further driving their adoption across various industries seeking sustainable hydrogen solutions.

Want to get more details about the segmentations? Register Here

“North America is expected to be the dominant and fastest-growing region over the forecasted period.”

In terms of region, the green hydrogen market is segmented into the North American region, the European region, the Asia-Pacific region, and the rest of the world.

North America is expected to be the dominant and fastest-growing region over the forecasted period, driven by substantial public and private investments, supportive policies, and a strong focus on decarbonization.

Moreover, the growing green hydrogen manufacturing facilities in North America, coupled with major green hydrogen key players, provide a high potential for market growth in the coming years.

Most of the major players compete in some of the factors, including price, service offerings, regional presence, etc. The following are the key players in the green hydrogen market:

Air Products Inc.

Bloom Energy

Engie

Linde plc.

Nel ASA

Toshiba Energy Systems & Solutions Corporation

Uniper SE

Note: The above list does not necessarily include all the top players in the market.

Are you a leading player in this market? We would love to include your name. Please write to us at [email protected]

In September 2024, Thermax collaborated with Ceres Power to produce large-scale Solid Oxide Electrolysis Cells (SOEC) for producing green hydrogen on an industrial scale by making use of industrial waste heat. This partnership is intended to develop efficient systems that will be optimized for industries like steel and refineries.

In April 2024, Oman's Hydrom entered into an agreement worth USD 11 billion with Electricité de France (EDF Group) to develop two green hydrogen projects. This project aims to produce approximately 178,000 tonnes per year (tpa) of green hydrogen by 2030, using approximately 4.5 gigawatts (GW) of wind and solar energy coupled with battery storage and an estimated 2.5 GW electrolyzer.

This report provides market intelligence most comprehensively. The report structure has been kept so that it offers maximum business value. It provides critical insights into market dynamics and will enable strategic decision-making for existing market players as well as those willing to enter the market.

The following are the key features of the report:

Market structure: Overview, industry life cycle analysis, supply chain analysis.

Market environment analysis: Growth drivers and constraints, Porter’s five forces analysis, SWOT analysis.

Market trend and forecast analysis.

Market segment trend and forecast.

Competitive landscape and dynamics: Market share, Service portfolio, New Product Launches, etc.

COVID-19 impact and its recovery curve.

Attractive market segments and associated growth opportunities.

Emerging trends.

Strategic growth opportunities for the existing and new players.

Key success factors.

|

Market Study Period |

2019-2032 |

|

Base Year |

2024 |

|

Forecast Period |

2025-2032 |

|

Trend Period |

2019-2023 |

|

Number of Tables & Figures |

>100 |

|

Number of Segments Analysed |

4 (Renewable Source Type, Technology Type, End-Use Type, and Region) |

|

Number of Regions Analysed |

4 (North America, Europe, Asia-Pacific, Rest of the World) |

|

Countries Analysed |

15 (The USA, Canada, Mexico, Germany, France, Italy, The UK, China, Japan, India, Brazil, Saudi Arabia, Rest of Europe, Rest of APAC, and Rest of the World) |

|

Free Customization Offered |

10% |

|

After Sales Support |

Unlimited |

|

Report Presentation |

Complimentary |

|

Market Dataset |

Complimentary |

|

Further Deep Dive & Consulting Services |

10% Discount |

This report studies the market, covering a period of 15 years of trend and forecast. The report provides detailed insights into the market dynamics to enable informed business decision-making and growth strategy formulation based on the opportunities present in the market.

The green hydrogen market is segmented into the following categories.

By Renewable Source Type

Wind Energy

Solar Energy

Other Renewable Sources

By Technology Type

Alkaline Electrolysis

PEM Electrolysis

By End-Use Type

Mobility

Chemical

Power

Grid Junction

Industrial

By Region

North America (Country Analysis: The USA, Canada, and Mexico)

Europe (Country Analysis: Germany, France, Italy, The UK, and Rest of Europe)

Asia-Pacific (Country Analysis: Japan, China, India, and Rest of Asia-Pacific)

Rest of the World (Country Analysis: Brazil, Saudi Arabia, and Others)

This strategic assessment report from Stratview Research provides a comprehensive analysis that reflects today’s green hydrogen market realities and future market possibilities for the forecast period.

The report segments and analyzes the market in the most detailed manner to provide a panoramic view of the market.

The vital data/information provided in the report can play a crucial role for market participants and investors in identifying the low-hanging fruits available in the market and formulating growth strategies to expedite their growth process.

This report offers high-quality insights and is the outcome of a detailed research methodology comprising extensive secondary research, rigorous primary interviews with industry stakeholders, and validation and triangulation with Stratview Research’s internal database and statistical tools.

More than 1,000 authenticated secondary sources, such as company annual reports, fact books, press releases, journals, investor presentations, white papers, patents, and articles, have been leveraged to gather the data.

We conducted more than 15 detailed primary interviews with market players across the value chain in all four regions and industry experts to obtain both qualitative and quantitative insights.

With this detailed report, Stratview Research offers one of the following free customization options to our respected clients:

Company Profiling

Competitive Benchmarking

Custom Research: Stratview Research offers custom research services across industries. In case of any custom research requirement related to market assessment, competitive benchmarking, sourcing and procurement, target screening, and others, please send your inquiry to [email protected].

The green hydrogen market refers to the global industry focused on the production, distribution, and utilization of hydrogen generated through renewable energy sources, primarily via electrolysis powered by solar, wind, or hydropower.

The forecasted value for the market is US$ 99.50 billion in 2032.

Green Hydrogen market size was USD 3.78 billion in 2024 and is expected to grow from USD 5.72 billion in 2025 to USD 99.5 billion in 2032, witnessing an impressive market growth (CAGR) of 50.4% during the forecast period (2025-2032).

The key drivers of the green hydrogen market include global plans for net-zero emissions by 2050 and high demand from FCEVs and power industry.

The top players in the green hydrogen market include • Air Liquide • Air Products Inc. • Bloom Energy • Cummins Inc. • Engie

North America is expected to be the dominant and fastest-growing region over the forecasted period, driven by substantial public and private investments, supportive policies, and a strong focus on decarbonization.

WE ACCEPT