404

+1-313-307-4176

Drone Warfare Market Analysis | 2025-2032

Drone Warfare Market Size, Share, Trends, Dynamics, Forecast, & Growth Analysis: 2025-2032

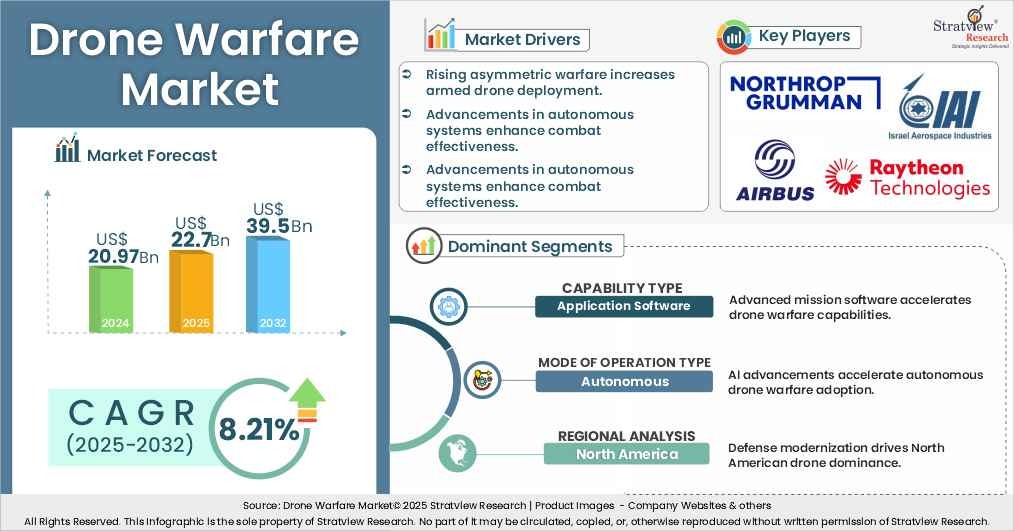

"The drone warfare market size was USD 20.97 billion in 2024.”

Want to get a free sample? Register Here

Have a look at the sales opportunities presented by the drone warfare market in terms of growth and market forecast.

|

Drone Warfare Market Data & Statistics |

||

|

Market Statistics |

Value (in USD Billion) |

Market Growth (%) |

|

Annual Market Size in 2023 |

USD 19.31 billion |

|

|

Annual Market Size in 2024 |

USD 20.97 billion |

YoY Growth in 2024: 8.6% |

|

Annual Market Size in 2025 |

USD 22.7 billion |

YoY Growth in 2025: 8.36% |

|

Annual Market Size in 2032 |

USD 39.5 billion |

CAGR 2025-2032: 8.21% |

|

Cumulative Sales Opportunity during 2025-2032 |

USD 243.8 billion |

|

|

Top 10 Countries’ Market Share in 2024 |

USD 16.78 billion + |

> 80% |

|

Top 10 Company’s Market Share in 2024 |

USD 10.49 billion to USD 14.68 billion |

50% - 70% |

Rising Global Defense Spending and Military Modernization

Global military modernization programs are increasingly prioritizing UAV-based reconnaissance, autonomous surveillance, and unmanned combat systems as part of broader force digitization and operational risk reduction strategies, shaping a drone warfare market trend toward higher adoption of unmanned and autonomous defense platforms.

According to Stockholm International Peace Research, global military expenditure reached approximately USD 2.89 trillion in 2025, marking the 11th consecutive year of growth, reinforcing sustained investment in advanced defense technologies including UAV-based combat and ISR systems.

Military spending reached 2.5% of global GDP in 2025, the highest level since 2009, while the U.S., China, and Russia accounted for ~51% of total global expenditure, driving large-scale procurement of next-generation unmanned and autonomous systems.

This is driving continuous procurement realignment toward UAV-centric defense architecture across modern military programs, strengthening the drone warfare ecosystem.

Modern Conflicts Driving UAV Adoption

The evolving nature of modern warfare has demonstrated the effectiveness of drones in surveillance, targeting, electronic warfare, and precision strike missions. This has accelerated the integration of tactical drones, loitering munitions, and autonomous systems into military operations, driving drone warfare market demand.

Sweden announced investments of approximately USD 437 million in unmanned military drone systems and related capabilities as part of its broader defense modernization efforts. The investment is aimed at strengthening intelligence gathering, battlefield surveillance, and operational readiness through the deployment of advanced unmanned platforms.

India is reportedly preparing drone procurement programs exceeding USD 2 billion, making it one of the country's largest military drone acquisition initiatives to date. The planned procurement is expected to enhance border surveillance, reconnaissance, and combat capabilities while supporting the integration of advanced drone technologies across multiple branches of the armed forces.

Such investments and procurement programs are accelerating the adoption of military drones worldwide, creating sustained demand for drone platforms, payloads, communication systems, and autonomous warfare technologies.

Counter-Drone Technologies and Electronic Warfare ThreatsTop of Form

The rapid advancement of counter-drone technologies, including jamming, GPS spoofing, directed-energy weapons, and anti-drone systems, is creating significant challenges for military drone operations. These technologies can disrupt communications, navigation, and mission effectiveness, reducing drone survivability in contested environments.

As a result, drone manufacturers must continuously upgrade their systems to counter evolving threats, increasing development costs and technological complexity. This ongoing drone-versus-counter-drone race acts as a key challenge for the drone warfare market.

Cybersecurity and Communication Vulnerabilities

Military drones rely heavily on communication links, software, and onboard firmware for navigation, data transmission, and mission execution. However, vulnerabilities such as hacking, signal interception, GPS spoofing, and cyberattacks can compromise operational effectiveness and mission security.

As drones become increasingly connected and autonomous, securing drone networks, communication systems, and critical software infrastructure remains a major challenge for defense agencies, potentially limiting adoption and deployment in sensitive military operations.Bottom of Form

Expansion of Autonomous and Swarm Drone Programs

The growing shift toward autonomous and swarm-enabled warfare is creating strong opportunities in the drone warfare market. Defense agencies are prioritizing AI-enabled multi-UAV systems to enhance mission scalability, resilience, and operational effectiveness in complex environments.

The UK Ministry of Defence allocated over £142 million (~USD 180 million) in 2025–2026 for drone and counter-drone innovation, including autonomous and swarm-enabled capabilities under its defence innovation programme.

The Swedish Government committed more than SEK 5.3 billion (~USD 500+ million) in 2026 for unmanned systems, including reconnaissance drones, loitering munitions, and unmanned electronic warfare capabilities supporting coordinated autonomous operations.

These investments reflect a broader shift toward AI-driven swarm architectures in defence strategies. As adoption expands, demand is expected to rise for swarm coordination software, edge AI systems, secure communications, and mission autonomy technologies.

Growth of Domestic Defense Manufacturing

The increasing focus on self-reliant defense ecosystems is emerging as a key drone warfare market trend, with countries prioritizing indigenous UAV production to reduce dependency on foreign suppliers, strengthen supply chain security, and enhance strategic autonomy.

India’s Ministry of Defence allocated ₹23,855 crore (2025–26) for domestic capital procurement, with strong emphasis on indigenous UAVs, sensors, and subsystems under initiatives like Make in India and Atmanirbhar Bharat.

The U.S. Department of Defense continues expanding its Blue UAS program, approving domestic unmanned systems for military use while restricting non-certified foreign drones, thereby boosting local UAV manufacturing demand.

The European Union’s European Defence Fund (EDF) is increasing 2025–2026 funding to strengthen regional defense industrial capacity, including unmanned systems, avionics, and secure communication technologies.

These initiatives are accelerating localized production ecosystems and reinforcing long-term demand for indigenous platforms, supporting the broader drone warfare market trend toward defense manufacturing self-reliance.

Increasing Demand for ISR and Border Security Operations

Rising security concerns and the need for continuous situational awareness are creating strong opportunities in the drone warfare market. Intelligence, Surveillance, and Reconnaissance (ISR) missions remain a core application of military UAVs, with growing emphasis on long-endurance platforms for persistent monitoring and rapid threat detection.

The U.S. Department of Defense FY2026 budget continues to prioritize ISR modernization, with over USD 60 billion+ allocated to intelligence and surveillance-related programs, including airborne ISR and unmanned systems integration.

The European Defence Agency (EDA) has increased joint funding initiatives in 2025–2026 for maritime surveillance and border security UAV projects, supporting shared ISR infrastructure across member states.

These developments highlight a sustained shift toward persistent, high-endurance surveillance capabilities, reinforcing the growing drone warfare market demand for ISR-focused UAV platforms, sensors, and analytics systems.

|

Segmentations |

List of Sub-Segments |

Segments with High-Growth Opportunity |

|

Capability Type Analysis |

Platform, Application Software, Services, Ground Control Stations, and Drone Launch & Recovery Systems |

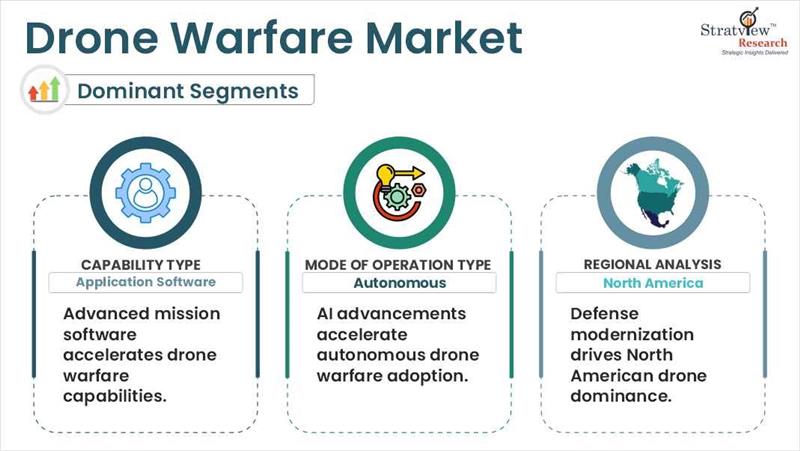

Application Software segment is anticipated to be the fastest-growing segment during the forecast period. |

|

Application Type Analysis |

Unmanned Combat Aerial Vehicles, ISR, and Delivery |

Unmanned Combat Aerial Vehicles (UCAVs) segment is expected to dominate the market with the highest growth rate during the forecast period. |

|

Mode of Operation Type Analysis |

Semi-Autonomous and Autonomous |

Autonomous segment is projected to lead the market with the highest growth rate during the forecast period. |

|

Regional Analysis |

North America, Europe, Asia-Pacific, and The Rest of the World |

North America is expected to be the dominant and fastest-growing region over the forecasted period. |

“Application Software segment is anticipated to be the fastest-growing segment during the forecast period.”

“Autonomous segment is projected to lead the market with the highest growth rate during the forecast period.”

Want to get more details about the segmentations? Register Here

“North America is expected to be the dominant and fastest-growing region over the forecasted period.”

Most of the major players compete in some of the factors, including price, service offerings, regional presence, etc. The following are the key players in the drone warfare market:

Note: The above list does not necessarily include all the top players in the market.

Are you a leading player in this market? We would love to include your name. Please write to us at [email protected]

This report provides market intelligence most comprehensively. The report structure has been kept so that it offers maximum business value. It provides critical insights into market dynamics and will enable strategic decision-making for existing market players as well as those willing to enter the market.

The following are the key features of the report:

|

Market Study Period |

2019-2032 |

|

Base Year |

2024 |

|

Forecast Period |

2025-2032 |

|

Trend Period |

2019-2023 |

|

Number of Tables & Figures |

>100 |

|

Number of Segments Analysed |

4 (Capability Type, Application Type, Mode of Operation Type, and Region) |

|

Number of Regions Analysed |

4 (North America, Europe, Asia-Pacific, Rest of the World) |

|

Countries Analysed |

15 (The USA, Canada, Mexico, Germany, France, Italy, The UK, China, Japan, India, Brazil, Saudi Arabia, Rest of Europe, Rest of APAC, and Rest of the World) |

|

Free Customization Offered |

10% |

|

After Sales Support |

Unlimited |

|

Report Presentation |

Complimentary |

|

Market Dataset |

Complimentary |

|

Further Deep Dive & Consulting Services |

10% Discount |

This report studies the market, covering a period of 15 years of trend and forecast. The report provides detailed insights into the market dynamics to enable informed business decision-making and growth strategy formulation based on the opportunities present in the market.

The drone warfare market is segmented into the following categories:

By Capability Type

By Application Type

By Mode of Operation Type

By Region

With this detailed report, Stratview Research offers one of the following free customization options to our respectable clients:

Company Profiling

Competitive Benchmarking

Custom Research: Stratview Research offers custom research services across industries. In case of any custom research requirement related to market assessment, competitive benchmarking, sourcing and procurement, target screening, and others, please send your inquiry to [email protected].

The report is delivered digitally through our online portal. Buyers receive login credentials from our team to access the report and may update their credentials at any time after the initial login.

Delivery timelines depend on the status of the report:

For the most accurate delivery timeline, please contact us to confirm the current status of the report.

Yes. You may request a complimentary preview of the report through a video conference with our team.

Yes. The scope of the report can be fully customized to align with your specific research objectives and information requirements.

Please contact us at [email protected], and our team will be happy to discuss your requirements and propose a tailored solution.

Yes. Selected sections of the report can be purchased separately based on your requirements. Please contact us at [email protected] to discuss your needs.

Yes, AI can help gather publicly available information, but its outputs are only as reliable as the data it accesses. Stratview Research reports are built using validated data, extensive primary interviews with industry stakeholders, and the expertise of our experienced research team.

Additionally, many critical insights, including market dynamics, competitive intelligence, and industry-specific trends, are not publicly available and therefore cannot be captured through AI alone.

The drone warfare market encompasses the global development, production, and deployment of unmanned aerial vehicles (UAVs) and associated systems for military applications. These drones are utilized for various missions, including intelligence, surveillance, reconnaissance (ISR), electronic warfare, and precision strikes.

The forecasted value for the market is US$ 39.5 billion in 2032.

Drone warfare market size was USD 20.97 billion in 2024 and is expected to grow from USD 22.7 billion in 2025 to USD 39.5 billion in 2032, witnessing an impressive market growth (CAGR) of 8.21% during the forecast period (2025-2032).

The key drivers of the drone warfare market include integration of advanced technologies in drones, growing cost advantages of drones over manned aircraft, increasing incorporation of drones into network-centric warfare, and a surge in global conflicts and terrorist threats.

The top players in the drone warfare market include • Northrop Grumman Corp. • Raytheon Technologies Corporation • Israel Aerospace Industries Ltd. • General Atomics Aeronautical Systems, Inc. • Teledyne FLIR LLC

North American region accounted for the largest share of the drone warfare market, driven by growing defense budgets and a strong focus on military modernization.

WE ACCEPT