Market Analysis | 2026-2032")

404

+1-313-307-4176

Counter Unmanned Aircraft System (UAS) Market Analysis | 2026-2032

Market Analysis | 2026-2032")

Counter Unmanned Aircraft System (UAS) Market Size, Share, Trend, Forecast, Competitive Landscape & Growth Opportunities: 2026-2032

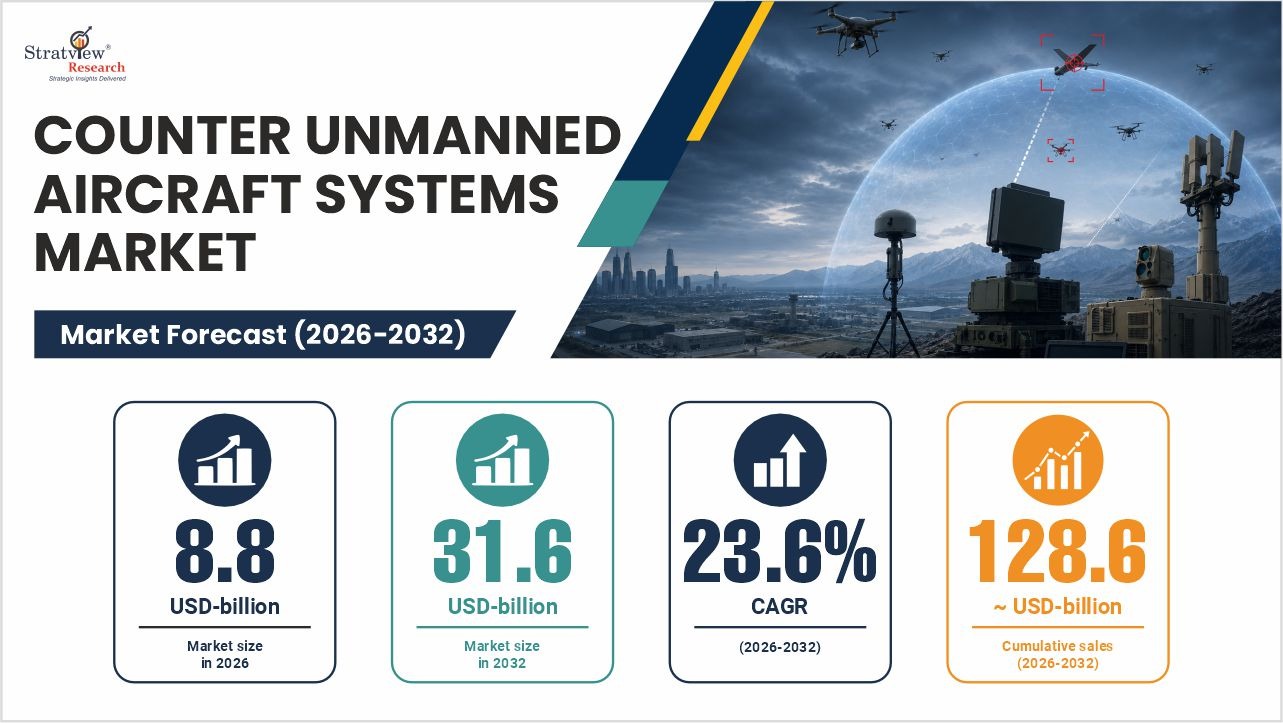

“The Counter Unmanned Aircraft System market is entering a phase of rapid operational integration, with the market valued at USD 7.1 billion in 2025 and projected to reach USD 8.8 billion in 2026, reflecting a strong 24.6% year-on-year growth, and further expanding to USD 31.6 billion by 2032 at a CAGR of 23.6%. This acceleration underscores the rising urgency to counter increasingly sophisticated and networked drone threats across defense and critical infrastructure environments.”

“A defining shift in the market is the transition from standalone counter-drone solutions to fully integrated, network-centric air defense ecosystems. This is evident in systems such as Raytheon’s Coyote counter-UAS platform, which combines KuRFS radar providing 360-degree surveillance with the FAAD command-and-control system to enable a coordinated detect–decide–engage workflow against multiple simultaneous aerial threats. Similarly, India’s indigenous D4 counter-drone system integrated with the Akashteer C2 architecture, offering a 5–8 km detection range, highlights the accelerating global move toward interoperable, layered air defense networks.”

“These developments illustrate how counter-UAS capability is no longer limited to point-defense interception but is increasingly embedded within broader command-and-control ecosystems. As a result, demand is shifting toward systems that can seamlessly integrate radar, RF sensing, electro-optical tracking, and neutralization technologies into unified operational frameworks capable of real-time decision-making across multi-domain environments.”

“The next wave of market expansion is being driven by large-scale deployment of such integrated architectures, alongside growing adoption of non-kinetic mitigation technologies including RF jamming, GNSS disruption, interceptor drones, and directed-energy systems. With ground-based and extended-range systems continuing to dominate deployments, North America remains the leading and fastest-growing region, supported by high defense spending, modernization programs, and accelerated procurement of advanced counter-drone solutions.”

The annual demand for the counter unmanned aircraft system was USD 7.1 billion in 2025 and is expected to reach USD 8.8 billion in 2026, up 24.6% than the value in 2025.

During the forecast period (2026-2032), the counter unmanned aircraft system market size is expected to grow at a CAGR of 23.6%. The annual demand will reach USD 31.6 billion in 2032, which is almost 3.6 times the demand in 2026.

As per the market analysis, during 2026-2032, the counter unmanned aircraft system industry is expected to generate a cumulative sales opportunity of USD 128.6 billion.

Sharpen Your Strategies by Knowing the Opportunity Pockets. Get Free Sample “Here”.

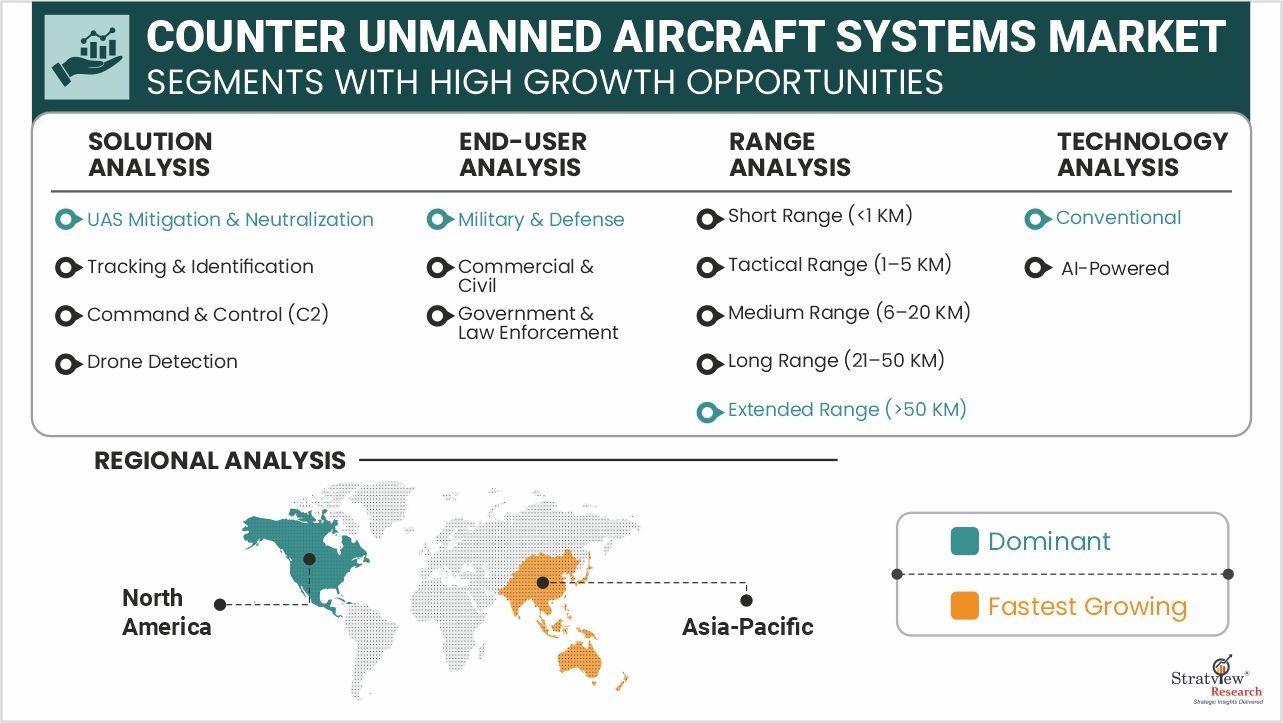

A comprehensive Counter Unmanned Aircraft System (C-UAS) market analysis indicates that segment-level performance varies significantly across key categories.

By region, North America is expected to remain the dominant and fastest-growing region during the forecast period.

By solution, UAS mitigation & neutralization segment is expected to be the dominant segment during the forecast period.

By end-use, military & defense segment is expected to be the dominant segment during the forecast period.

By deployment, ground-based segment is expected to be the dominant segment during the forecast period.

By range, extended-range (>50 km) segment is expected to be the dominant segment during the forecast period.

By technology, conventional segment is expected to be the dominant segment during the forecast period.

Have a look at the sales opportunities presented by the counter unmanned aircraft system market in terms of growth and market forecast.

Counter Unmanned Aircraft System (UAS) Market Data & Statistics

|

Market Statistics |

Value (in USD Billion) |

Market Growth (%) |

|

Annual Market Size in 2025 |

USD 7.1 billion |

- |

|

Annual Market Size in 2026 |

USD 8.8 billion |

YoY Growth in 2026: 24.6% |

|

Annual Market Size in 2032 |

USD 31.6 billion |

CAGR 2026-2032: 23.6% |

|

Cumulative Sales Opportunity during 2026-2032 |

USD 128.6 billion |

- |

|

Top 10 Countries’ Market Share in 2025 |

USD 5.7 billion + |

> 80% |

|

Top 10 Company’s Market Share in 2025 |

USD 3.6 billion to USD 5.0 billion |

50% - 70% |

Want to Explore the Market Opportunities? Get Free Sample “Here”.

A Counter-Unmanned Aircraft System (Counter-UAS) is a technology or system designed to detect, track, identify, and neutralize unauthorized or hostile drones. It helps protect military installations, critical infrastructure, airports, government facilities, and public venues from potential drone-related threats.

Counter-UAS solutions use sensors such as radar, radiofrequency (RF) detectors, and cameras to monitor airspace and identify drone activity. Once a threat is detected, the system can disrupt or disable the drone through methods such as RF jamming, GPS interference, interceptor drones, or other defensive measures, helping ensure airspace security and operational safety.

Align with the Mega Trends Shaping the Industry. Get Free Sample “Here”

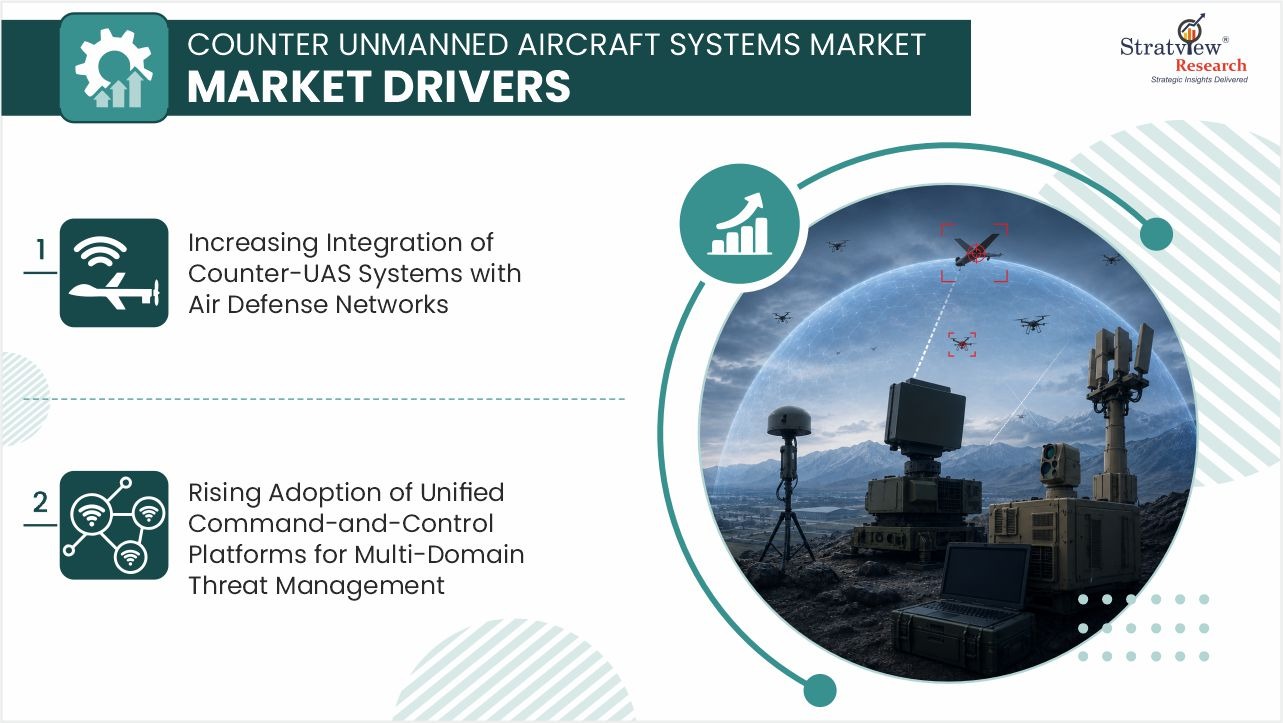

The counter unmanned aircraft system market is witnessing increased demand as military organizations integrate counter-drone capabilities into broader air and missile defense architectures to address evolving aerial threats

The U.S. Department of Defense’s Replicator initiative highlights the growing integration of counter-UAS capabilities within broader defense networks. The program includes counter-uncrewed aerial systems such as Fortem Technologies' DroneHunter F700 alongside autonomous aerial, surface, and undersea platforms, supporting demand for interoperable and networked defense architectures.

India's indigenous D4 counter-drone system has been integrated with the Akashteer command-and-control architecture and offers a drone detection range of 5–8 km, demonstrating the growing adoption of networked counter-UAS capabilities within integrated air defense systems.

Additionally, The Indian Army is expanding deployment of the indigenous SAKSHAM AI-powered Counter-UAS Grid System, which provides integrated detection and neutralization capabilities across tactical battlefield airspace extending up to 3,000 meters above ground level, strengthening layered airspace protection against emerging drone threats.

These developments highlight the growing emphasis on network-centric and layered air defense strategies, accelerating counter-UAS market demand for interoperable detection, tracking, and neutralization systems capable of operating within broader defense networks.

Rising Adoption of Unified Command-and-Control Platforms for Multi-Domain Threat Management

The counter unmanned aircraft system market is witnessing growing demand as defense organizations increasingly adopt unified command-and-control (C2) platforms to enhance situational awareness, coordinate responses across multiple domains, and manage evolving drone threats more effectively.

For example, Raytheon's Coyote counter-UAS system combines the KuRFS radar, which provides 360-degree surveillance, with the FAAD C2 command-and-control platform that manages the detect-decide-engage cycle and supports the simultaneous handling of multiple aerial threats.

Northrop Grumman introduced its AiON Counter-UAS platform, enabling a single operator to manage multiple sites through a unified command-and-control interface. The platform integrates with more than 45 sensors and systems, supporting coordinated threat detection, tracking, and response across distributed operational environments.

The growing deployment of unified command-and-control platforms is accelerating counter-UAS market growth by enabling faster decision-making, improved situational awareness, and seamless coordination of multi-domain air defense operations.

Supply Chain Constraints Affecting Critical Electro-Optical, Infrared, and Directed-Energy Components

The counter unmanned aircraft system market faces challenges due to supply chain constraints affecting critical electro-optical (EO), infrared (IR), and directed-energy components that are essential for drone detection, tracking, identification, and neutralization.

Operational Validation and Safety Certification Challenges for Advanced Drone Defeat Technologies

The counter unmanned aircraft system market faces challenges related to operational validation and safety certification of emerging drone defeat technologies, including kinetic interceptors, electronic warfare systems, and directed-energy solutions.

Advanced counter-drone technologies must undergo extensive real-world testing to validate performance against diverse threat profiles, including swarming drones, low-RCS targets, and high-speed unmanned aerial systems operating in complex environments. This increases deployment timelines and slows large-scale adoption.

Stringent certification and compliance requirements, including MIL-STD-461/464 electromagnetic compatibility standards, NATO STANAG operational protocols, and civil aviation regulatory approvals such as FAA airspace safety frameworks, increase validation complexity for electronic warfare and directed-energy based counter-UAS systems, often extending deployment timelines.

Scalable Deployment of Non-Kinetic Counter-UAS Solutions Across Civil and Defense Applications

The counter unmanned aircraft system market is creating significant opportunities driven by the increasing demand for scalable, non-kinetic drone mitigation technologies that can be deployed across both defense and civilian environments.

Growing restrictions on kinetic interception in urban and civilian airspace are accelerating the adoption of non-kinetic solutions such as RF jamming, GNSS spoofing, and high-power microwave systems, enabling flexible deployment across airports, critical infrastructure, and public venues.

Advancements in modular and software-defined counter-UAS platforms are enabling rapid scalability, allowing a single system architecture to be deployed across fixed-site, mobile, and handheld configurations while supporting integration with existing surveillance and command-and-control networks.

The increasing adoption of integrated defense platforms is shaping the counter unmanned aircraft system market trend globally.

Increasing Adoption of Interoperable Counter-UAS Architectures Across Defense Ecosystems

The counter unmanned aircraft system market is generating strong opportunities due to the growing need for interoperable and open-architecture solutions that can integrate seamlessly with existing air defense, surveillance, and command-and-control infrastructures.

The U.S. Army’s Forward Area Air Defense (FAAD) ecosystem modernization efforts are increasingly focused on enabling plug-and-play integration of radars, electro-optical sensors, and interceptor systems, supporting flexible deployment configurations across allied and expeditionary defense operations.

NATO’s ongoing digital modernization efforts under its Federated Mission Networking (FMN) framework are promoting standardized data-sharing and interoperability across member nations, enabling different command-and-control systems to exchange real-time situational awareness data for coordinated responses against aerial threats, including unmanned aircraft systems.

These advancements are contributing to the expansion of the counter unmanned aircraft system market size over the forecast period.

|

Segmentations |

List of Sub-Segments |

Segments with High-Growth Opportunity |

||

|

Solution Analysis |

Drone Detection, Tracking & Identification; Command & Control (C2); UAS Mitigation & Neutralization; Services |

UAS Mitigation & Neutralization segment is projected to be the dominant segment during the forecast period. |

||

|

End-User Analysis |

Commercial & Civil, Military & Defense, Government & Law Enforcement |

Military & Defense segment is expected to hold the largest market share during the forecast period. |

||

|

Deployment Analysis |

Ground-Based, Handheld |

Ground-Based segment is anticipated to dominate the market during the forecast period. |

||

|

Range Analysis |

|

Extended Range (>50 KM) segment is expected to have the largest market share during the forecast period. |

||

|

Technology Analysis |

Conventional, AI-Powered |

Conventional segment is projected to lead the market, while AI-powered systems are expected to witness the fastest growth over the forecast period. |

||

|

Regional Analysis |

North America, Europe, Asia-Pacific, and The Rest of the World |

North America is expected to be the dominant and fastest-growing region over the forecast period |

Get Insights on High-Growth Segments. Get Free Sample “Here”.

“UAS Mitigation & Neutralization segment is projected to be the dominant segment during the forecast period.”

The counter unmanned aircraft system market is segmented by solution into drone detection & tracking, command & control (C2), UAS mitigation & neutralization, and support services.

UAS Mitigation & Neutralization segment is projected to be the dominant segment during the forecast period due to the increasing need to actively counter unauthorized and hostile drones across military bases, airports, critical infrastructure, government facilities, and public venues.

The dominance of this segment is driven by growing investments in electronic warfare systems, RF jammers, GPS spoofing technologies, interceptor drones, and directed-energy weapons. As drone threats continue to evolve in complexity and frequency, end users are increasingly prioritizing neutralization capabilities to ensure effective protection against aerial intrusions and security risks..

“Military & Defense segment is projected to be the dominant segment during the forecast period.”

The counter unmanned aircraft system market is segmented by end user into military & defense, government & law enforcement, and commercial & civil.

Military & Defense segment is projected to be the dominant segment during the forecast period owing to the growing deployment of counter-drone technologies to protect military personnel, installations, critical assets, and operational airspace from emerging unmanned threats.

The segment's dominance is supported by rising defense expenditures, increasing procurement of advanced counter-UAS systems, and growing concerns regarding the use of drones for intelligence gathering, surveillance, and attack missions. Military organizations worldwide are integrating multi-layered counter-drone solutions into their air defense architectures to enhance force protection and operational readiness.

“Ground-Based segment is projected to be the dominant segment during the forecast period.”

The counter unmanned aircraft system market is segmented by deployment into ground-based and handheld systems.

Ground-Based segment is projected to be the dominant segment during the forecast period due to its widespread deployment across military facilities, airports, border security installations, critical infrastructure sites, and public event venues.

The dominance of this segment is driven by its ability to integrate multiple detection and mitigation technologies, including radar systems, RF sensors, electro-optical cameras, and electronic countermeasures. Ground-based platforms provide broad-area surveillance, continuous monitoring capabilities, and scalable protection, making them the preferred choice for fixed-site security applications.

“Extended Range (>50 km) segment is projected to be the dominant segment during the forecast period.”

The counter unmanned aircraft system market is segmented by range into short range (<1 km), tactical range (1–5 km), medium range (6–20 km), long range (21–50 km), and extended range (>50 km).

Extended Range (>50 km) segment is projected to be the dominant segment during the forecast period owing to the growing need for early threat detection and interception of drones operating at greater distances from protected assets.

The increasing use of long-endurance unmanned aerial systems and the rising emphasis on layered airspace security are driving demand for extended-range counter-UAS capabilities. Governments and defense organizations are investing in advanced radar systems, integrated surveillance networks, and long-range detection technologies to enhance situational awareness and response effectiveness.

“Conventional segment is projected to be the dominant segment during the forecast period.”

The counter unmanned aircraft system market is segmented by technology into conventional and AI-powered systems.

Conventional segment is projected to be the dominant segment during the forecast period due to its established deployment across defense, homeland security, and critical infrastructure applications. These systems utilize proven detection, tracking, and mitigation technologies that have demonstrated operational effectiveness in real-world environments.

The segment continues to benefit from widespread adoption of radar-based surveillance, RF detection systems, electronic jamming solutions, and integrated command-and-control platforms. The maturity, reliability, and regulatory acceptance of conventional technologies are expected to support their continued market leadership throughout the forecast period.

“North America is expected to be the dominant and fastest-growing region over the forecast period.”

Based on region, the counter unmanned aircraft system market has been segmented into North America, Europe, Asia-Pacific, Middle East, and Rest of the World.

North America is expected to be the dominant and fastest-growing region over the forecast period due to substantial defense spending, increasing investments in counter-drone technologies, and the growing need to protect military installations, critical infrastructure, airports, and public events from unauthorized drone activity.

The presence of leading defense contractors, strong government support for counter-UAS modernization programs, and rapid adoption of advanced detection and mitigation technologies further strengthen regional leadership. Additionally, increasing concerns regarding drone-based security threats and evolving airspace protection requirements are accelerating market growth across the region.

Align with the Mega Trends Shaping the Industry. Get Free Sample “Here”

The market is fragmented with the presence of less than 100 global and regional players. Some of the major players also manufacture counter unmanned aircraft system (UAS) parts. Leading players hold excellent market positions with a vast product portfolio, a wide distribution network, and years of track record.

The following are the key players in the counter unmanned aircraft system (UAS) market

Raytheon Technologies Corporation (RTX)

Lockheed Martin Corporation

Leonardo S.p.A

Saab AB

Israel Aerospace Industries (IAI)

Recent mergers & acquisitions and other developments in the counter unmanned aircraft systems market reflect evolving market trends, and impact the market. Below given are a few recent developments in the market –

In March 2026, AeroVironment acquired Empirical Systems Aerospace (ESAero) for approximately $200 million, strengthening its portfolio in unmanned aircraft systems and expanding its capabilities in advanced aerospace engineering and defense drone technologies.

In March 2026, Zen Technologies acquired a 55% stake in TISA Aerospace, an emerging Indian defense technology company focused on UAVs and loitering munitions, enhancing its indigenous counter-UAS and autonomous systems capabilities.

In 2025, AeroVironment completed the acquisition of BlueHalo for approximately $4.1 billion, significantly expanding its presence in space, electronic warfare, and counter-UAS technologies, particularly in advanced sensing and autonomous defense systems.

This report provides market intelligence most comprehensively. The report structure has been kept so that it offers maximum business value. It provides critical insights into market dynamics and will enable strategic decision-making for existing market players as well as those willing to enter the market.

The following are the key features of the report:

Market structure: Overview, industry life cycle analysis, supply chain analysis.

Market environment analysis: Growth drivers and constraints, Porter’s five forces analysis, SWOT analysis.

Market trend and forecast analysis.

Market segment trend and forecast.

Competitive landscape and dynamics: Market share, Service portfolio, New Product Launches, etc.

COVID-19 impact and its recovery curve.

Attractive market segments and associated growth opportunities.

Emerging trends.

Strategic growth opportunities for the existing and new players.

Key success factors.

|

Market Study Period |

2019-2032 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2032 |

|

Trend Period |

2019-2024 |

|

Number of Tables & Figures |

>100 |

|

Number of Segments Analysed |

6 (Component Type, End-User Type, Deployement Type, Range Type, Technology and Region) |

|

Number of Regions Analysed |

4 (North America, Europe, Asia-Pacific, Rest of the World) |

|

Countries Analysed |

15 (The USA, Canada, Mexico, Germany, France, Italy, The UK, China, Japan, India, Brazil, Saudi Arabia, Rest of Europe, Rest of APAC, and Rest of the World) |

|

Free Customization Offered |

10% |

|

After Sales Support |

Unlimited |

|

Report Presentation |

Complimentary |

|

Market Dataset |

Complimentary |

|

Further Deep Dive & Consulting Services |

10% Discount |

Counter-UAS Market, By Solution Type

Drone Detection, Tracking & Identification Systems

Command & Control (C2) Systems

UAS Mitigation & Neutralization Systems

Services

Counter-UAS Market, By End-User Type

Commercial & Civil

Military & Defense

Government & Law Enforcement

Counter-UAS Market, By Deployment Type

Ground-Based Systems

Handheld Systems

Counter-UAS Market, By Range Type

Short Range (<1 KM)

Tactical Range (1–5 KM)

Medium Range (6–20 KM)

Long Range (21–50 KM)

Extended Range (>50 KM)

Counter-UAS Market, By Technology Type

Conventional Systems

AI-Powered Systems

Counter-UAS Market, By Region Type

North America (Country Analysis: The USA, Canada, and Mexico)

Europe (Country Analysis: Germany, France, The UK, Russia, and the Rest of Europe)

Asia-Pacific (Country Analysis: Japan, China, India, and Rest of Asia-Pacific)

Rest of the World (Country Analysis: Brazil and Others)

This strategic assessment report from Stratview Research provides a comprehensive analysis that reflects today’s counter uas market realities and future market possibilities for the forecast period.

The report segments and analyzes the market in the most detailed manner to provide a panoramic view of the market.

The vital data/information provided in the report can play a crucial role for market participants and investors in identifying the low-hanging fruits available in the market and formulating growth strategies to expedite their growth process.

This report offers high-quality insights and is the outcome of a detailed research methodology comprising extensive secondary research, rigorous primary interviews with industry stakeholders, and validation and triangulation with Stratview Research’s internal database and statistical tools.

More than 1,000 authenticated secondary sources, such as company annual reports, fact books, press releases, journals, investor presentations, white papers, patents, and articles, have been leveraged to gather the data.

We conducted more than 15 detailed primary interviews with market players across the value chain in all four regions and industry experts to obtain both qualitative and quantitative insights.

With this detailed report, Stratview Research offers one of the following free customization options to our respected clients:

Company Profiling

Detailed profiling of additional market players (up to three players)

SWOT analysis of key players (up to three players)

Competitive Benchmarking

Benchmarking of key players on the following parameters: Service portfolio, geographical reach, regional presence, and strategic alliances

Custom Research: Stratview Research offers custom research services across industries. In case of any custom research requirement related to market assessment, competitive benchmarking, sourcing and procurement, target screening, and others, please send your inquiry to [email protected]

The report is delivered digitally through our online portal. Buyers receive login credentials from our team to access the report and may update their credentials at any time after the initial login.

Delivery timelines depend on the status of the report:

For the most accurate delivery timeline, please contact us to confirm the current status of the report.

Yes. You may request a complimentary preview of the report through a video conference with our team.

Yes. The scope of the report can be fully customized to align with your specific research objectives and information requirements.

Please contact us at [email protected], and our team will be happy to discuss your requirements and propose a tailored solution.

Yes. Selected sections of the report can be purchased separately based on your requirements. Please contact us at [email protected] to discuss your needs.

Yes, AI can help gather publicly available information, but its outputs are only as reliable as the data it accesses. Stratview Research reports are built using validated data, extensive primary interviews with industry stakeholders, and the expertise of our experienced research team.

Additionally, many critical insights, including market dynamics, competitive intelligence, and industry-specific trends, are not publicly available and therefore cannot be captured through AI alone.

The Counter Unmanned Aircraft System (C-UAS) market refers to technologies and solutions designed to detect, track, identify, and neutralize unauthorized or hostile drones. These systems are widely used to protect military bases, airports, critical infrastructure, government facilities, and public spaces from drone-enabled threats.

The Counter UAS market size was valued at approximately USD 7.1 billion in 2025.

The market is expected to reach USD 31.6 billion by 2032, growing significantly from USD 8.8 billion in 2026.

The Counter UAS market is projected to grow at a CAGR of 23.6% during 2026–2032.

The key drivers of the Counter UAS market include increasing drone-based security threats, modernization of integrated air defense systems, rising defense expenditures, and growing adoption of networked command-and-control platforms.

Key applications driving the market include military base protection, airport security, border surveillance, protection of critical infrastructure, and securing public venues and government facilities from unauthorized drone activity.

The major end-use industries include military & defense, government & law enforcement, and commercial & civil sectors, with military & defense accounting for the largest share due to rising adoption of advanced counter-drone systems.

The top players in the Counter UAS market include Northrop Grumman Corporation, Raytheon Technologies Corporation (RTX), Lockheed Martin Corporation, Thales Group, Leonardo S.p.A, Saab AB, Elbit Systems Ltd., and Israel Aerospace Industries (IAI).

WE ACCEPT