404

+1-313-307-4176

Aerospace Carbon Seals Market Analysis | 2026-2034

Aerospace Carbon Seals Market Size, Share, Trends, Dynamics, Forecast, & Growth Analysis: 2026-2034

Aerospace Carbon Seals Market is segmented by Platform Type (Commercial Aircraft, Regional Aircraft, Helicopter, Military Aircraft, General Aviation, and Space), by Application Type (Turbine Engine, Auxiliary Power Unit, Gearbox, Hydraulics & Actuation, and Other Applications), by Product Type (Face seals, Circumferential seals, and Other Seals), by End-User Type (OE, and Aftermarket), and by Region (North America [The USA, Canada, and Mexico], Europe [Germany, France, The UK, Russia, and Rest of Europe], Asia-Pacific [China, Japan, India, and Rest of Asia-Pacific], and Rest of the World [Brazil, Saudi Arabia, and Others]).

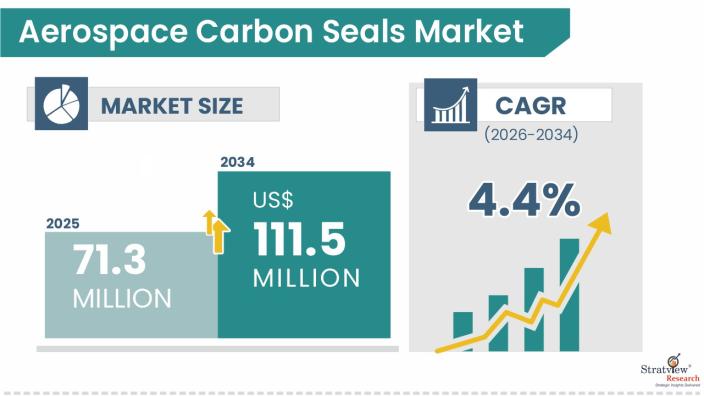

The aerospace carbon seals market size was USD 71.3 million in 2025 and is likely to grow at a CAGR of 4.4% during 2026-2034 to reach USD 111.5 million in 2034.

Want to know more about the market scope? Register Here

Aerospace carbon seals represent a specialized segment within aerospace seals, designed for high-temperature and high-speed rotating applications in critical aircraft systems. Typically manufactured from carbon-graphite materials, these seals are widely used in aircraft engines, auxiliary power units (APUs), and gearboxes to prevent leakage of lubricants and gases across rotating shafts and bearing compartments. Their self-lubricating properties, thermal stability, and wear resistance enable reliable performance under extreme operating conditions such as high pressure, temperature variations, and rotational speeds. The growing demand for efficient, durable, and high-performance sealing solutions across commercial, military, and space applications, supported by rising aircraft production, expanding fleets, and increasing MRO activities, is driving the adoption of aerospace carbon seals.

A considerable number of strategic alliances, including M&As, JVs, etc., have been performed over the past few years:

The aerospace carbon seals industry players are concentrating on improving the leakage properties, increasing the life of the seals, and providing improved thermal properties along with wear resistance. Some of the significant developments are related to the improvement of the properties of the carbon material by optimizing the porosity levels and the impregnation systems. Additionally, the segmented ring face seals are being improved, along with the development of the seals for specific applications such as turbine engines, gearboxes, auxiliary power units, fuel systems, and oil management systems.

|

Segmentations |

List of Sub-Segments |

Segments with High-Growth Opportunity |

|

Platform Type Analysis |

Commercial Aircraft, Regional Aircraft, Helicopter, Military Aircraft, General Aviation, and Space |

Commercial aircraft account for the largest share of the market and is also projected to witness the fastest growth in the market over the next seven years. |

|

Application Analysis |

Turbine Engine, Auxiliary Power Unit, Gearbox, Hydraulics & Actuation, and Other Applications |

Turbine Engine holds the dominant share in the aerospace carbon seals market, whereas the Auxiliary Power Unit is likely to be the fastest-growing segment during the period. |

|

Product Type Analysis |

Face Seals, Circumferential Seals, and Others |

Carbon Face Seals dominate the market, and it is also projected to register the fastest growth rate during the forecast period. |

|

End-User Analysis |

OE, and Aftermarket |

OE accounts for the largest share of the market, whereas the aftermarket segment is likely to grow steadily, driven by increasing maintenance and overhaul activities. |

|

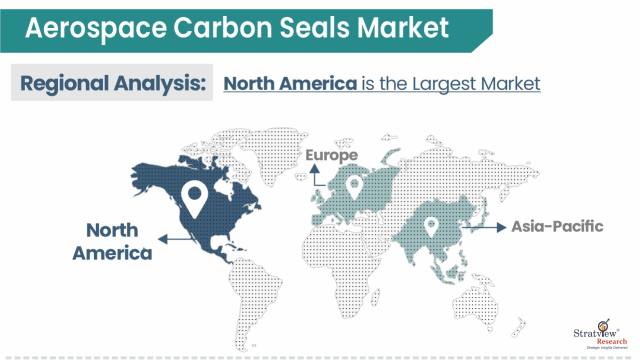

Regional Analysis |

North America, Europe, Asia-Pacific, and the Rest of the World |

North America dominates the aerospace carbon seals market, driven by the strong presence of aircraft OEMs, engine OEMs, and extensive MRO infrastructure, whereas Asia-Pacific is emerging as the fastest-growing region during the forecast period. |

“Commercial aircraft account for the largest share of the market and is also projected to grow as the fastest-growing rate in the aerospace carbon seals market during the forecast period.”

The aerospace carbon seals market is segmented by platform type into commercial aircraft, regional aircraft, military aircraft, helicopters, general aviation, and space. Commercial aircraft are projected to remain the leading demand generator for the carbon seals, owing to their large global fleet size and high utilization rates, and frequent maintenance, repair, and overhaul (MRO) requirements. The continuous expansion of air passenger traffic, coupled with rising aircraft production and ongoing fleet modernization programs, is further driving the demand for efficient and reliable sealing solutions, particularly in engines and auxiliary systems where carbon seals play a critical role in maintaining performance, efficiency, and safety.

Military aircraft are anticipated to experience the second-fastest growth in the market over the next seven years, driven by an increase in defense modernization programs and the procurement of next-generation fighter and transport aircraft in various economies. Expanding defense budgets and the procurement of next-generation aircraft are anticipated to drive the demand for aerospace carbon seals in military aircraft systems.

“Turbine engine holds the dominant share in the aerospace carbon seals market, whereas Auxiliary Power Units are expected to be the fastest-growing segment during the forecast period.”

By application, the aerospace carbon seals market is segmented into turbine engines, auxiliary power units, gearboxes, hydraulics & actuation, and others. Aerospace carbon seals are a specialized type of mechanical seals used in turbine engines, auxiliary power units, and gearboxes where leakage control is required under high-temperature and high-speed rotating conditions. Among applications, turbine engines are expected to continue their dominance owing to extensive use of carbon seals in rotating interfaces and hot sections within aircraft systems. These seals are critical for pressure and leakage control under high-temperature and high-speed operating conditions.

The auxiliary power units are expected to witness the fastest growth, driven by rising aircraft deliveries, increasing onboard power demand, and growing focus on fuel-efficient aircraft systems, along with expanding MRO activities.

“Carbon face seals dominate the product type segment in the market and are also projected to register the fastest growth rate among all seal categories during the forecast period.”

By product type, the aerospace carbon seals market is categorized into face seals, circumferential seals, and other seals. Face seals hold the largest share of the market due to their superior sealing efficiency, ability to operate under high-pressure and high-temperature conditions, and widespread application in critical engine sections such as bearing compartments and oil systems, and in gearbox compartments. Their robust design, reliability, and ability to minimize leakage in high-speed rotating environments make them the preferred choice across both commercial and military aircraft engines.

Circumferential seals account for a notable share of the market due to their ability to accommodate shaft misalignment and thermal expansion while maintaining effective sealing performance in dynamic operating conditions. Their segmented design allows for flexibility and durability, making them well-suited for use in bearing compartments and other engine sections where reliable sealing and long service life are essential. These seals are commonly utilized in systems operating under varying thermal and operational conditions. Their consistent sealing performance supports stable demand across multiple aerospace applications.

“OE accounts for the largest share of demand, whereas the Aftermarket segment is expected to grow steadily, driven by increasing maintenance and overhaul activities.”

The aerospace carbon seals market, by end-user, has been classified into OE and aftermarket. The OE segment is expected to dominate the market share, as carbon seals are critical components integrated during the initial assembly of aircraft engines, APUs, and gearboxes, and are closely aligned with aircraft production rates. Increasing deliveries of new commercial and military aircraft, along with the introduction of next-generation engines, are driving strong demand from OEMs, thereby supporting the dominance of the OE segment in the market.

The aftermarket segment is also expected to grow steadily as carbon seals are subject to wear and periodic replacement due to continuous exposure to elevated temperatures, pressure differentials, and rotational stress. Increasing aircraft utilization rates, aging fleets, and rising aircraft MRO activities are driving consistent demand for replacement seals, thereby supporting sustained growth in the aftermarket segment.

“North America dominates the aerospace carbon seals market, driven by the strong presence of aircraft OEMs, engine OEMs, tier players, and extensive MRO infrastructure, whereas Asia-Pacific is emerging as the fastest-growing region in the market during the forecast period.”

The Asia-Pacific region is observed to be the fastest-growing segment in the aerospace carbon seals market, driven by rapid growth in air passenger traffic, increasing aircraft fleet size, and significant aircraft procurement across emerging economies such as China, India, and Southeast Asia. Expanding low-cost carrier networks, rising defense spending, and the development of indigenous aircraft programs are further contributing to market growth, along with the gradual expansion of regional MRO capabilities supporting higher demand for replacement components, including carbon seals.

North America retains its position of leadership in the market for aerospace carbon seals, owing to the strong presence of major aircraft and engine OEMs, a well-established aerospace supply chain, and a large installed fleet of commercial and military aircraft. High aircraft production rates, advanced technological capabilities, and significant MRO activity in the region further contribute to sustained demand for carbon seals across both OEM and aftermarket segments.

Know the high-growth countries in this report. Register Here

The market is moderately consolidated, with over 30 players. Most of the major players compete in key governing factors, including technology innovation, product portfolio, regional presence, and strategic partnerships. The following are the key players in the market.

Here is the list of the Top Players (Based on Dominance)

Note: The above list does not necessarily include all the top players in the market.

Are you the leading player in this market? We would love to include your name. Please write to us at [email protected]

This report provides market intelligence most comprehensively. The report structure has been kept so that it offers maximum business value. It provides critical insights into market dynamics and will enable strategic decision-making for existing market players as well as those willing to enter the market. The following are the key features of the report:

This report studies the market, covering a period of 12 years of trends and forecasts. The report provides detailed insights into the market dynamics to enable informed business decision-making and growth strategy formulation based on the opportunities present in the market.

The aerospace carbon seals market is segmented into the following categories.

By Platform Type

By Application Type

By Product Type

By End-User Type

By Region

With this detailed report, Stratview Research offers one of the following free customization options to our respected clients:

Company Profiling

Competitive Benchmarking

Custom Research: Stratview Research offers custom research services across industries. In case of any custom research requirement related to market assessment, competitive benchmarking, sourcing and procurement, target screening, and others, please send your inquiry to [email protected].

The report is delivered digitally through our online portal. Buyers receive login credentials from our team to access the report and may update their credentials at any time after the initial login.

Delivery timelines depend on the status of the report:

For the most accurate delivery timeline, please contact us to confirm the current status of the report.

Yes. You may request a complimentary preview of the report through a video conference with our team.

Yes. The scope of the report can be fully customized to align with your specific research objectives and information requirements.

Please contact us at [email protected], and our team will be happy to discuss your requirements and propose a tailored solution.

Yes. Selected sections of the report can be purchased separately based on your requirements. Please contact us at [email protected] to discuss your needs.

Yes, AI can help gather publicly available information, but its outputs are only as reliable as the data it accesses. Stratview Research reports are built using validated data, extensive primary interviews with industry stakeholders, and the expertise of our experienced research team.

Additionally, many critical insights, including market dynamics, competitive intelligence, and industry-specific trends, are not publicly available and therefore cannot be captured through AI alone.

The aerospace carbon seals market is expected to grow at a CAGR of 4.4% during 2034. The growth is driven by the increase in aircraft production, fleet expansion, and increasing defense aircraft procurement activities, along with advancements in aeroengine technologies.

The aerospace carbon seals market size was USD 71.3 million in 2025.

The forecasted value of the aerospace carbon seals market is expected to be USD 111.5 million in 2034.

Eaton Corporation plc, AB SKF, Enpro Inc., Stein Seal Company, Eagle Industry Co., Ltd., Ergoseal, Inc., Magnetic Seal Corporation, St. Marys Carbon Company Inc., Morgan Advanced Materials plc, and Ningbo Tiangong Fluid Technology Co., Ltd. are the leading players in the market.

Face seals comprise the largest segment in the market, driven by their superior sealing properties in high-speed rotation environments and their widespread use in aerospace applications.

The auxiliary power units (APUs) segment is expected to be the fastest-growing application in the market. This growth is driven by increasing aircraft deliveries, higher reliance on APUs for onboard power and ground operations, and the shift toward more electric aircraft architectures. Additionally, rising aircraft utilization and expanding MRO activities are further accelerating demand for carbon seals in APU systems.

North America is the largest regional market for aerospace carbon seals, driven by a strong footprint of major aircraft and engine OEMs, a large installed aircraft fleet, and a strong aftermarket demand.

WE ACCEPT