Carbon fiber has transformed the bicycle industry: From Greg LeMond’s historic 1986 Tour de France victory on a carbon-fiber bike to today’s $771 million market, the material has become a cornerstone of premium cycling.

At a Glance

- Carbon-fiber frames weigh as little as 700 grams.

- Advanced manufacturing cuts production time.

- E-bikes drive demand for carbon composites.

In the summer of 1986, Greg LeMond arrived at the Tour de France, arguably the most prestigious cycling race in the world, on a bicycle with an unconventional frame material. His victory marked the first time a carbon fiber–integrated bicycle was showcased on such a prominent global stage. Widespread adoption did not come immediately, but Lemond's bike validated carbon fiber’s potential in cycling.

The bicycle industry has seen a long evolutionary journey, from the wooden-frame and iron-wheeled designs of 1817 to a period dominated by steel, and now to carbon-fiber frames weighing as little as 700 grams.

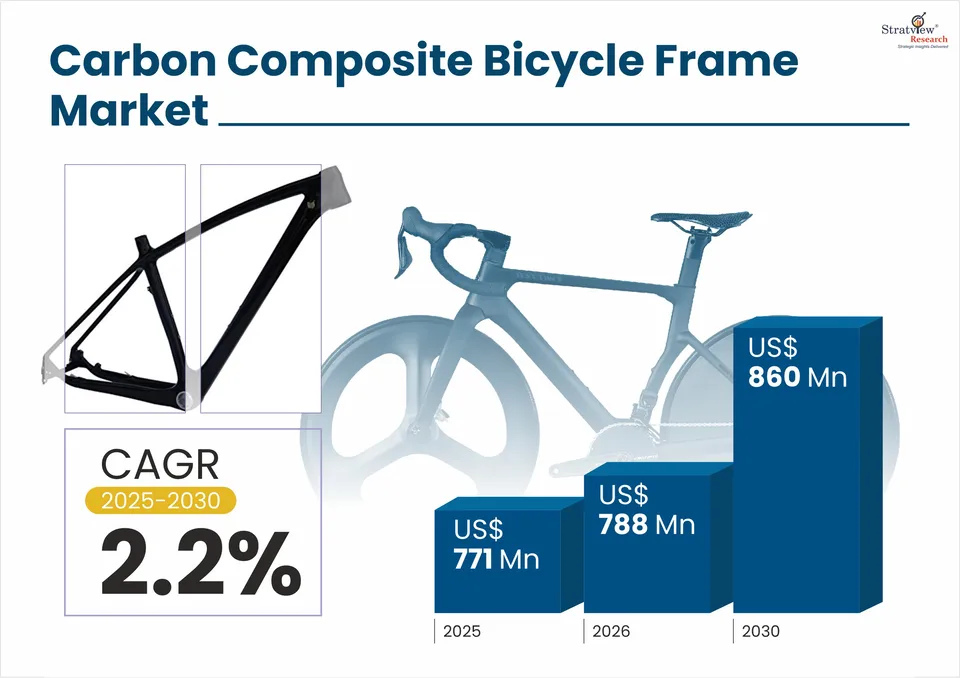

Carbon-fiber bicycle frames now represent a market valued at $771 million in 2025, with approximately three million units sold annually.

Source: Stratview Research

Why carbon composites are the future of cycling

The case for carbon-composite frames rests on properties that are difficult to replicate in other materials at proximate prices and weights.

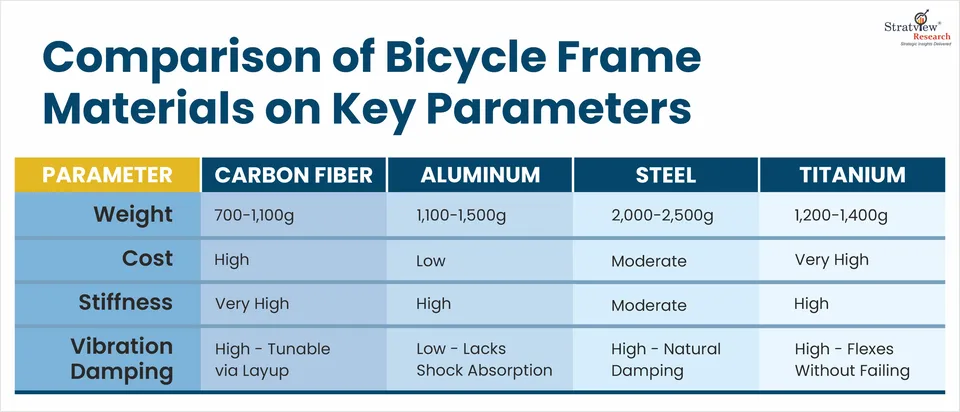

An industrial-grade carbon-fiber road frame weighs somewhere between 700 and 900 grams. By comparison, an aluminum frame weighs between 1,200 and 1,500 grams. Titanium approaches carbon's weight-to-stiffness ratio, but at a cost that puts it beyond most mass-production bicycles.

Another advantage is geometric freedom. Metal frames are built from tubes, which bring design constraints. Carbon-fiber frames can accommodate complex, integrated three-dimensional geometries: Internal cable routing, battery housings, and junction points for electric drivetrains, for example, can be embedded in the structure from the outset rather than added as separate components.

Equally important is vibration behavior: Carbon-composite frames transmit significantly lower levels of high-frequency road vibration to the rider compared to similarly priced material alternatives.

Source: Stratview Research

Market trends: Road bikes, mountain bikes, and electrification

Carbon composites have become more desirable in the performance bikes category for obvious reasons, and their adoption has taken shape across various segments of the market.

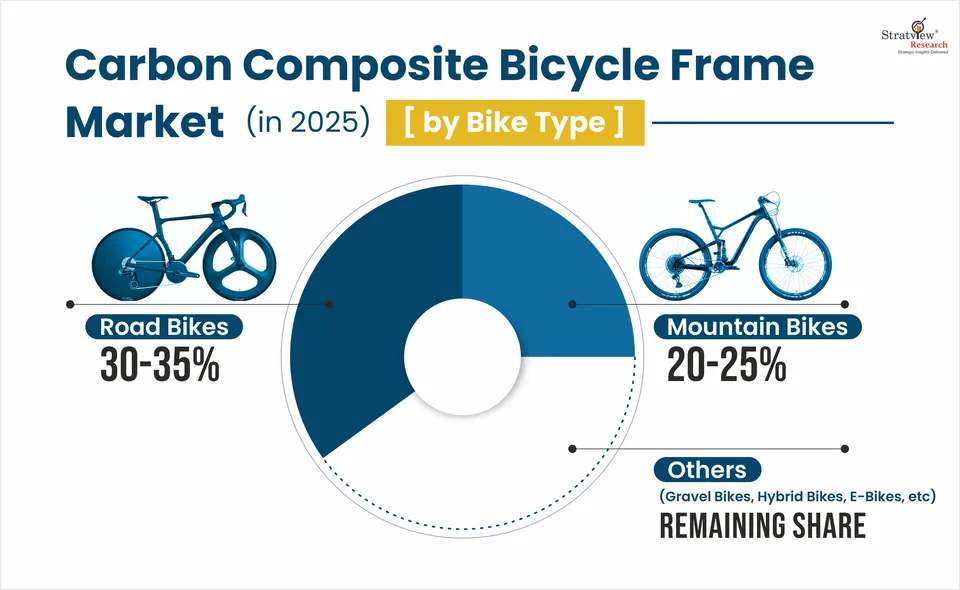

Today, road bicycles remain the largest segment by value, making up 33% to 35% of the carbon-composite frame market. Newer categories are also gaining momentum. For instance, mountain biking is now the fastest-growing segment by volume and already represents 20% to 25% of the market, driven largely by riders who carry performance expectations from road cycling into trail riding.

A similar pattern is visible in gravel bikes, which have rapidly scaled from being nearly non-existent in the mass market before 2018 to becoming one of the fastest-growing segments in premium cycling. Their ability to handle different types of terrain appeals to riders who want the speed and efficiency of road bikes but on rough or mixed surfaces.

E-mountain bikes are also a fast-growing premium category, where the role of carbon composites shifts from pure performance to structural necessity. Electrification adds roughly 3 to 7 kg to the drivetrain, and carbon composites help recover part of that weight due to their high strength-to-weight ratio while providing the architecture needed to integrate battery systems and manage motor loads. This role is extending more broadly as bicycles incorporate more and more electronics.

Source: Stratview Research

Manufacturing innovations: Faster, smarter, better

As carbon composites continue to penetrate across bicycle segments, the manufacturing processes must support them in parallel. However, manufacturing has remained a challenge due to long cycle times and labor-intensive processes. Traditional prepreg layup combined with autoclave curing can take days, often 90 to 100 hours per frame, keeping production slow and concentrated in large facilities. As demand for carbon-fiber bicycles expanded into significant volumes, these manufacturing constraints became increasingly difficult to sustain at scale. The need for faster yet cost-efficient production methods has warranted the exploration of alternative processing technologies.

Resin transfer molding (RTM) is gradually being adopted as an alternative to autoclave curing, using a closed-mold process that can cut cycle times from days to hours. Interestingly, high-pressure RTM (HP-RTM), when combined with techniques like filament winding, can reduce total production time to as low as 140 minutes per frame, making high-volume production far more viable. This is already being applied at scale by companies like Time Bicycles, which is adapting automotive-grade RTM processes at its US manufacturing facilities to improve consistency and durability.

Automated fiber placement (AFP) is another manufacturing technique worth mentioning. By employing robots to place fiber exactly where it is structurally required, AFP not only reduces excess material and improves consistency, but also cuts labor by roughly 80%, while enabling lighter frames, commonly in the 600 to 700 gram range. Companies like Revved Industries are deploying AFP-based production.

Furthermore, new approaches such as continuous-fiber 3D printing and advanced braided-RTM are expanding design possibilities. Beyond geometry, these methods are enabling faster iteration, lower tooling dependence, and opening the door for smaller manufacturers to compete. Brands like Revel Bikes, Arevo Bikes, and Santa Cruz Bicycles are experimenting with 3D-printed carbon-composite bicycles.

Supply chain challenges and reshoring efforts

The current status of carbon bicycle frame production is straightforward: The majority of frames sold under American and European brand names are manufactured in Asia. The top three Taiwanese frame manufacturers — Topkey, Carbotec, and AIM — collectively supply more than 40% of the entire global market. China's manufacturing clusters in Xiamen, Shenzhen, and Dongguan house plants capable of producing 500,000 frames per year, a scale no Western operation can match in the foreseeable future. On the whole, industry estimates suggest that leading premium brands in North America and Europe source between 95% and 99% of their carbon frames from Asian manufacturers.

Although Vietnam is emerging as an alternative due to lower labor costs and more favorable US tariff treatment, its carbon-frame manufacturing base is early-stage relative to the mature Taiwanese and Chinese supply chains. The expertise and ecosystems that make Taiwan and China efficient took decades to build. Furthermore, the raw material supply chain reinforces this concentration, as the major carbon-fiber producers — Toray, Teijin, and Hexcel — hold long-term contracts calibrated to large Asian frame manufacturers.

Sustainability and the road ahead

Going forward, the growth of carbon-composite bicycles will depend as much on strategic choices as on material performance. Manufacturers should focus on incremental improvements in their operations, like tapping into newer manufacturing techniques such as RTM, AFP, and related automation approaches, to enhance production efficiency, consistency, and overall product quality. Also, a key priority should be building a strong portfolio around electric bicycles, particularly e-mountain bikes, where electrification warrants lightweight, high-strength, and integration-friendly materials like carbon fiber.

At the same time, sustainability is emerging as an increasingly important consideration. Eco-conscious buyers, especially in Europe, are increasingly aware of the energy-intensive nature and limited recyclability of traditional carbon frames, and this is beginning to influence purchasing decisions. As a result, stakeholders should actively invest in solutions such as thermoplastic composites and recycled carbon fiber.

It is important to note that these opportunities will continue to play out within a fundamentally premium and niche market. Carbon-fiber bicycles remain anchored to a relatively narrow customer base of competitive cyclists and performance-driven enthusiasts, where the willingness to pay for the material's benefits justifies the 80% to 100% price premium over traditional materials, while remaining significantly cost-effective compared to ultra-expensive materials such as titanium. As a result, the market is expected to grow steadily but modestly, reaching around $788 million in 2026 and approximately $860 million by 2030.

Editor's note: Vyapak Tiwari contributed to this article. A business analyst with Stratview Research, he has experience in the mobility and composites domains. He has contributed to numerous articles, market briefings, and thought leadership reports.

Authored by Stratview Research. Also published on – plasticstoday.com