404

+1-313-307-4176

Thermal Interface Materials Market Analysis | 2026-2032

Thermal Interface Materials Market Size, Share, Trends, Dynamics, Forecast, & Growth Analysis: 2026-2032

Thermal Interface Materials Market is segmented by Type (Greases & Adhesives, Tapes & Films, Gap Fillers, Metal-Based Thermal Interface Materials, Phase Change Materials, and Others), by Application Type (Computers, Telecom, Medical Devices, Industrial Machinery, Consumer Durables, Automotive Electronics, and Others), and by Region (North America, Europe, Asia-Pacific, and Rest of the World).

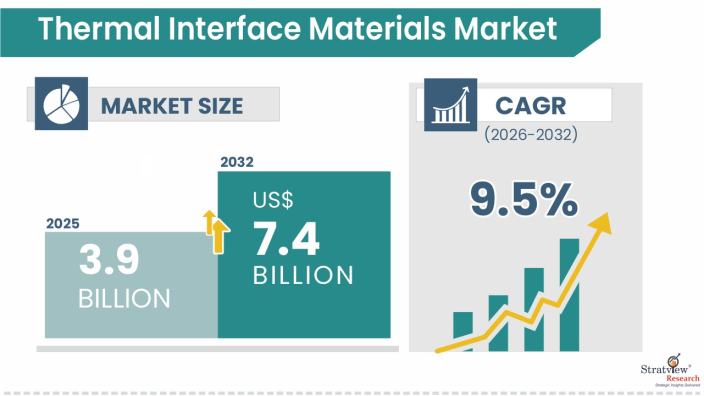

The thermal interface materials market was estimated at USD 3.9 billion in 2025 and is likely to grow at a CAGR of 9.5% during 2026-2032 to reach USD 7.4 billion in 2032.

Wish to get a free sample? Register Here

A thermal interface refers to the material or layer used to enhance the transfer of heat between two surfaces in contact, such as a computer processor and a heat sink. It serves as a bridge between the two surfaces, filling any gaps and irregularities, and improving the thermal conductivity to facilitate efficient heat dissipation.

The primary purpose of a thermal interface is to minimize the thermal resistance at the interface, ensuring optimal heat transfer and preventing overheating. Common types of thermal interfaces include thermal pastes, pads, and phase-change materials, each with specific properties suited for different applications.

Rising Electric Vehicle (EV) Adoption is Expanding Market Share

The rising adoption of electric vehicles (EVs) is expanding the market share of the thermal interface materials market. Growing demand for efficient thermal management in EV battery packs, power electronics, and charging systems is increasing the adoption of advanced thermal interface materials.

According to the International Energy Agency (IEA), global EV sales surpassed 17 million units in 2024, up more than 25% from 2023. The rapid growth in EV adoption is increasing demand for thermal interface materials that enhance battery safety, performance, and lifespan.

According to the International Energy Agency (IEA), electric vehicle fleets consumed around 180 TWh of electricity in 2024, nearly 60% higher than the previous year. The rising electricity consumption reflects the rapid expansion of EV fleets and battery systems, further increasing demand for high-performance thermal interface materials for efficient battery thermal management.

Expansion of Data Centers and AI Computing Infrastructure

The expansion of data centers and AI computing infrastructure is driving the growth of the thermal interface materials market. Rising deployment of AI servers, high-performance processors, and advanced cooling systems is increasing demand for thermal interface materials to ensure efficient heat dissipation and reliable system performance.

According to the International Energy Agency (IEA), global electricity demand grew 4.3% in 2024, with new data centers and AI infrastructure among the major contributors to increased power consumption. The rapid expansion of AI-driven computing infrastructure is driving demand for thermal interface materials used in processors, GPUs, and cooling systems.

Growing Demand for Consumer Electronics and Miniaturized

The growing demand for consumer electronics and miniaturized devices is accelerating demand in the thermal interface materials market. Increasing adoption of compact, high-performance electronic devices is driving the need for advanced thermal interface materials to improve heat dissipation, device reliability, and operational efficiency.

According to the International Energy Agency (IEA), global electricity consumption in buildings increased by more than 600 TWh (5%) in 2024, partly due to the increasing use of connected electronic devices and digital infrastructure. The growing deployment of electronic devices is driving demand for thermal interface materials to support effective thermal management in compact designs.

Market Challenge

High Cost of Advanced Thermal Interface Materials Restrains Market Growth

The high cost of advanced thermal interface materials is restraining the growth of the thermal interface materials market. The use of premium raw materials and complex manufacturing processes increases product costs, limiting adoption across cost-sensitive consumer and industrial applications.

Physical Performance Limitations and Thermal Resistance Issues

Physical performance limitations and thermal resistance issues are challenging demand in the thermal interface materials market. Increasing power densities in semiconductors and electronic devices require highly efficient thermal management, while improper material selection or application can reduce heat transfer performance.

According to the Electric Power Research Institute (EPRI), U.S. data centers could consume up to 9% of the nation's electricity demand by 2030. The rising thermal loads in high-performance computing environments are increasing the need for advanced thermal interface materials, while highlighting the performance challenges associated with achieving optimal thermal conductivity.

Precision Application and Manufacturing Complexity

Precision application and manufacturing complexity are restraining the growth of the thermal interface materials market. Maintaining the optimal thickness and application of thermal interface materials is critical for ensuring efficient heat transfer and device reliability, particularly in EV batteries and semiconductor packaging.

According to the International Energy Agency (IEA), electric vehicle fleets consumed around 180 TWh of electricity in 2024, nearly 60% higher than the previous year. The growing deployment of EV battery systems is increasing demand for precisely applied thermal interface materials, while highlighting manufacturing and quality control challenges.

Market Opportunity

Deployment of 5G Infrastructure and Advanced Telecom Equipment is Emerging as a Key Market Trend

The deployment of 5G infrastructure and advanced telecom equipment is emerging as a key trend in the thermal interface materials market. The expansion of high-performance networking equipment and telecom infrastructure is creating opportunities for thermal interface materials to improve heat dissipation, system reliability, and operational efficiency.

According to the International Energy Agency (IEA), global electricity demand increased by 1,080 TWh in 2024, nearly double the average annual increase of the previous decade, partly supported by the expansion of digital infrastructure. The rapid deployment of 5G networks is increasing demand for thermal interface materials in base stations, antennas, and networking equipment.

Adoption of Nanomaterial-Based TIMs Strengthens Market Forecast

The adoption of nanomaterial-based thermal interface materials is strengthening the market forecast for the thermal interface materials market. The commercialization of graphene-, nanodiamond-, and other carbon-based TIMs is creating opportunities for advanced thermal management across semiconductors, EVs, aerospace, and high-performance computing applications.

According to the U.S. Energy Information Administration (EIA), U.S. electricity demand is projected to reach 4,193 billion kWh in 2025, driven largely by the rapid expansion of AI and data centers. The growing deployment of AI computing infrastructure is increasing demand for high-performance thermal interface materials to enhance heat dissipation and ensure reliable operation of processors, GPUs, and advanced cooling systems.

Growth of Renewable Energy and Energy Storage Systems is Creating New Market Opportunities

The growth of renewable energy and energy storage systems is creating new opportunities in the thermal interface materials market. Expanding deployment of battery energy storage systems (BESS), solar inverters, and power electronics is increasing demand for thermal interface materials to improve system efficiency, safety, and reliability.

According to the International Energy Agency (IEA), global electricity demand increased by 4.3% in 2024, driven by the rapid adoption of electrification and clean energy technologies, while renewable electricity generation continues to expand worldwide. The growing deployment of renewable energy infrastructure is driving demand for thermal interface materials used in energy storage and power electronic systems.

|

Segmentations |

List of Sub-Segments |

Segments with High Growth Opportunity |

|

Type Analysis |

Greases & Adhesives, Tapes & Films, Gap Fillers, Metal-Based Thermal Interface Materials, Phase Change Materials, and Others |

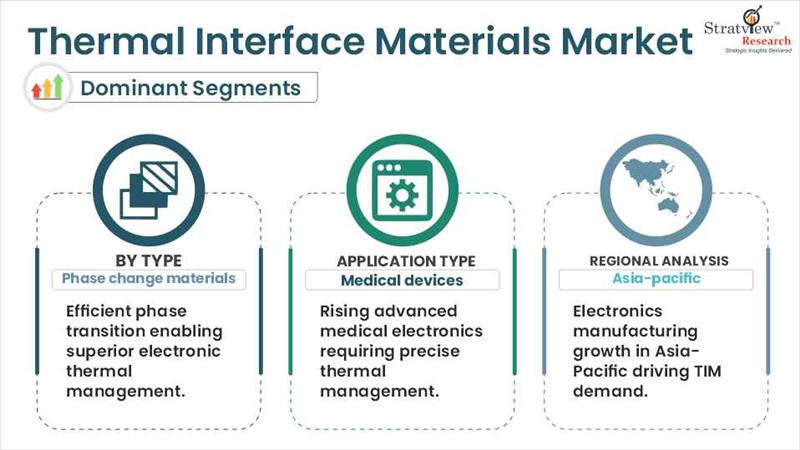

The phase change materials dominate the market during the forecast period. The growth is attributed to their specific properties, such as being a good conductor of electricity and the capability to remain solid at room temperature and melt as the temperature increases. |

|

Application Type Analysis |

Computers, Telecom, Medical Devices, Industrial Machinery, Consumer Durables, Automotive Electronics, and Others |

The medical devices segment is estimated to be the fastest-growing segment during the forecast period. The electronic devices used in the medical industry need proper thermal management. The electronics employed in this industry are required to remain cool sufficiently to path uninterruptedly and appropriately within their functioning temperature arrays. |

|

Regional Analysis |

North America, Europe, Asia-Pacific, and Rest of the World |

Asia-Pacific is expected to remain the largest market for thermal interface materials in the coming five years. |

“The phase change materials dominate the market during the forecast period.”

The market is segmented as greases & adhesives, tapes & films, gap fillers, metal-based thermal interface materials, phase change materials, and others. The phase change materials segment is estimated to be the fastest-growing segment in the coming five years.

The growth is attributed to their specific properties, such as being a good conductor of electricity and the capability to remain solid at room temperature and melt as the temperature increases.

“The medical devices segment dominates the market during the forecast period.”

The market is segmented as computers, telecom, medical devices, industrial machinery, consumer durables, automotive electronics, and others. The medical devices segment is estimated to be the fastest-growing segment during the forecast period. The electronic devices used in the medical industry need proper thermal management. The electronics employed in this industry are required to remain cool sufficiently to path uninterruptedly and appropriately within their functioning temperature ranges.

Want to get more details about the segmentations? Register Here

The operative thermal management allows surplus heat to be resourcefully moved, uniformly spread, and adequately dissipated. This progresses system dependability and service lifespan of electronic contrivances in the medical sector. Several medical apparatuses influence the computing power of progressive microprocessors. These comprise ultrasound equipment, lasers, X-ray machines, and digital imaging. These devices require proper thermal administration as the surplus heat can be upshot in imprecisions or breakdowns.

“Asia-Pacific is expected to remain the largest market for thermal interface materials in the coming five years.”

China and India are the growth engines of the region. The market is driven by the growing demand from various end-use industries, such as telecom and consumer electronics in the region. Further, the demand for better consumer electronics and telecom devices is fuelling the growth of the market.

North America and Europe are also expected to offer considerable growth opportunities during the forecast period.

Know the high-growth countries in this report. Register Here

The market is highly populated with the presence of several local, regional, and global players. Most of the major players compete in some of the governing factors including price, product offerings, regional presence, etc.

The following are the key players in the thermal interface materials market (arranged alphabetically).

Note: The above list does not necessarily include all the top players in the market.

Are you the leading player in this market? We would love to include your name. Write to us at [email protected]

This strategic assessment report, from Stratview Research, provides a comprehensive analysis that reflects today’s thermal interface materials market realities and future market possibilities for the forecast period of 2026 to 2032. After a continuous interest in our thermal interface materials market report from the industry stakeholders, we have tried to further accentuate our research scope to the thermal interface materials market to provide the most crystal-clear picture of the market. The report segments and analyses the market in the most detailed manner to provide a panoramic view of the market. The vital data/information provided in the report can play a crucial role for the market participants as well as investors in the identification of the low-hanging fruits available in the market as well as to formulate the growth strategies to expedite their growth process.

This report offers high-quality insights and is the outcome of a detailed research methodology comprising extensive secondary research, rigorous primary interviews with industry stakeholders, and validation and triangulation with Stratview Research’s internal database and statistical tools. More than 1000 authenticated secondary sources, such as company annual reports, fact books, press releases, journals, investor presentations, white papers, patents, and articles, have been leveraged to gather the data. We conducted more than 15 detailed primary interviews with the market players across the value chain in all four regions and industry experts to obtain both qualitative and quantitative insights.

This report provides market intelligence in the most comprehensive way. The report structure has been kept such that it offers maximum business value. It provides critical insights into market dynamics and will enable strategic decision-making for existing market players as well as those willing to enter the market. The following are the key features of the report:

This report studies the market, covering a period of 12 years of trend and forecast. The report provides detailed insights into the market dynamics to enable informed business decision-making and growth strategy formulation based on the opportunities present in the market.

The thermal interface materials market is segmented into the following categories:

By Type

By Application Type

By Region

With this detailed report, Stratview Research offers one of the following free customization options to our respectable clients:

Company Profiling

Competitive Benchmarking

Custom Research: Stratview Research offers custom research services across sectors. In case of any custom research requirement related to market assessment, competitive benchmarking, sourcing and procurement, target screening, and others, please send your inquiry to [email protected].

The report is delivered digitally through our online portal. Buyers receive login credentials from our team to access the report and may update their credentials at any time after the initial login.

Delivery timelines depend on the status of the report:

For the most accurate delivery timeline, please contact us to confirm the current status of the report.

Yes. You may request a complimentary preview of the report through a video conference with our team.

Yes. The scope of the report can be fully customized to align with your specific research objectives and information requirements.

Please contact us at [email protected], and our team will be happy to discuss your requirements and propose a tailored solution.

Yes. Selected sections of the report can be purchased separately based on your requirements. Please contact us at [email protected] to discuss your needs.

Yes, AI can help gather publicly available information, but its outputs are only as reliable as the data it accesses. Stratview Research reports are built using validated data, extensive primary interviews with industry stakeholders, and the expertise of our experienced research team.

Additionally, many critical insights, including market dynamics, competitive intelligence, and industry-specific trends, are not publicly available and therefore cannot be captured through AI alone.

A thermal interface refers to the material or layer used to enhance the transfer of heat between two surfaces in contact, such as a computer processor and a heat sink. It serves as a bridge between the two surfaces, filling any gaps and irregularities, and improving the thermal conductivity to facilitate efficient heat dissipation. The primary purpose of a thermal interface is to minimize the thermal resistance at the interface, ensuring optimal heat transfer and preventing overheating. Common types of thermal interfaces include thermal pastes, pads, and phase-change materials, each with specific properties suited for different applications.

The thermal interface materials market was estimated at USD 3.9 billion in 2025.

The thermal interface materials market is likely to reach USD 7.4 billion in 2032.

The thermal interface materials market is likely to grow at a CAGR of 9.5% during 2026-2032.

The 3M Company, Henkel AG & Co. KGAA, Parker Hannifin Corporation, DOW Corning Corporation, Laird Technologies, Inc., Momentive Performance Materials Inc., The Bergquist Company, Inc., Indium Corporation, Wakefield-Vette, Inc., Zalman Tech Co., Ltd are among the key players in the market.

Asia-Pacific is expected to be the largest market for thermal interface materials during the next five years.

The medical device segment is expected to be the fastest-growing segment in the market in the coming years.

WE ACCEPT