404

+1-313-307-4176

Data Center RFID Market Analysis | 2024-2032

Data Center RFID Market Size, Share, Trend, Forecast, Competitive Analysis, and Growth Opportunity: 2024-2032

Data Center RFID Market is segmented by Application Type (IT Asset & Infrastructure Tracking, Security Access & Compliance Management, and Environmental & Operational Monitoring), by Tag Type (Passive, Semi-Passive, and Active), by Reader Type (Fixed Reader and Handheld Reader), by Frequency Type (Low Frequency, High Frequency, and Ultra High Frequency), by Data Center Type (Hyperscale, Colocation, Enterprise, and Edge) and by Region (North America [The USA, Canada, and Mexico], Europe [The UK, Germany, France, and Rest of Europe], Asia-Pacific [China, Australia, Japan, India, and Rest of Asia-Pacific], and Rest of the World [Brazil, Africa, and Others]).

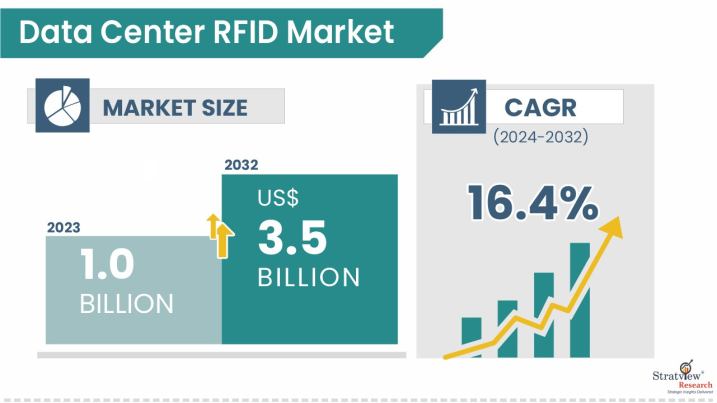

The data center RFID market size was USD 1.0 billion in 2023 and is likely to grow at a CAGR of 16.4% during 2024-2032 to reach USD 3.5 billion in 2032.

Want to know more about the market scope? Register Here

Data Center Radio Frequency Identification Technology (RFID) is becoming an essential tool for infrastructure management, enabling real-time visibility and automated tracking of critical assets. RFID systems use electromagnetic fields to identify tags attached to servers, racks, cables, and networking equipment without requiring line-of-sight scanning. This capability enhances operational efficiency in complex data center environments where manual tracking is time-consuming and prone to errors. RFID solutions include passive, semi-passive, and active tags operating across multiple frequency bands, allowing operators to select configurations based on range, accuracy, and performance requirements.

One of the key drivers of the data center RFID market is the rapid expansion of hyperscale and colocation facilities, which increases the complexity of asset management. As data centers scale, tracking thousands of components becomes challenging, creating demand for automated inventory and lifecycle management solutions. RFID enables quick identification, reduces human errors, and improves audit readiness. Additionally, strict compliance requirements and security standards encourage adoption of RFID-based monitoring to ensure proper asset control, prevent unauthorized movement, and maintain accurate documentation across large, distributed infrastructure environments.

Another major factor driving market growth is the integration of RFID with advanced data center management and security systems. Modern RFID deployments support environmental monitoring, predictive maintenance, and access control capabilities, improving reliability and operational resilience. Organizations are leveraging RFID to track equipment health, monitor temperature-sensitive assets, and enhance cybersecurity through controlled access. Furthermore, the shift toward automation, digital infrastructure management, and real-time analytics is accelerating RFID adoption. These capabilities help reduce downtime, optimize resource utilization, and support efficient data center operations in increasingly dynamic and high-density computing environments.

A considerable number of strategic alliances, including M&As, JVs, etc., have been performed over the past few years:

|

Segmentations |

List of Sub-Segments |

Segments with High-Growth Opportunity |

|

Application-Type Analysis |

IT Asset & Infrastructure Tracking, Security Access & Compliance Management, and Environmental & Operational Monitoring |

IT Asset & Infrastructure Tracking systems lead the market, and Environmental & Operational Monitoring is the fastest-growing segment. |

|

Tag-Type Analysis |

Passive Tag, Semi-Passive Tag, and Active Tag |

Passive Tag systems dominate current deployments, while Active Tags exhibit the fastest growth. |

|

Reader-Type Analysis |

Fixed Reader and Handheld Reader |

Fixed Reader installations account for the largest market share, while Handheld Readers show the fastest growth. |

|

Frequency-Type Analysis |

Low Frequency, High Frequency, and Ultra High Frequency |

Ultra-High Frequency systems lead both current installations and growth rates. |

|

Data-Center-Type Analysis |

Hyperscale, Colocation, Enterprise, and Edge |

Colocation facilities drive substantial RFID adoption, while Hyperscale data centers demonstrate the fastest growth. |

|

Region Analysis |

North America, Europe, Asia-Pacific, and The Rest of the World |

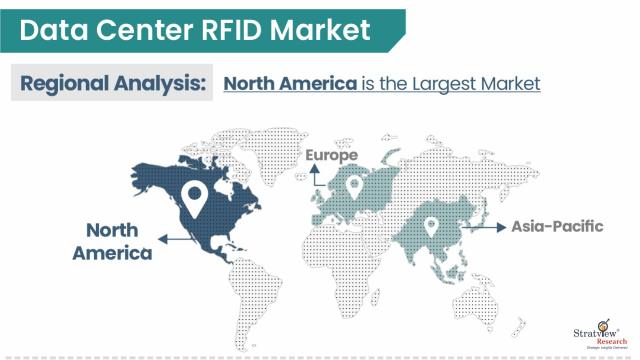

North America leads the market through concentrated hyperscale facilities, while Asia-Pacific grows fastest. |

“IT asset & infrastructure tracking dominates current RFID deployments through fundamental inventory management and audit requirements, while Environmental & Operational Monitoring emerges as the fastest-growing application driven by predictive maintenance imperatives and real-time condition awareness.”

The data center RFID market is segmented by application type into IT Asset & Infrastructure Tracking, Security Access & Compliance Management, and Environmental & Operational Monitoring. The reason behind the dominance of IT Asset and Infrastructure Tracking is the need to provide automated inventory controls, lifecycle tools, and audit records in both hyperscale and colocation facilities. The most rapidly expanding segment is the Environmental & Operational Monitoring, which is fueled by sensor-based RFID tags that are used to monitor the conditions of the environment in real time and predictive maintenance in high-density settings. Smaller in share, Security Access & Compliance Management continues to grow steadily because of RFID-based access control integration, regulatory compliance needs like SOC 2 and ISO 27001.

“Passive tags hold the largest market share through cost efficiency and maintenance simplicity, while active tags demonstrate the fastest growth, enabling advanced real-time location and sensor-enabled monitoring.”

The data center RFID market is segmented by tag type into Passive Tag, Semi-Passive Tag, and Active Tag. The prevalence of passive tags is low cost, battery-free, long life, and applicable in large-scale tracking of the assets across servers and racks. They can have sufficient reading ranges and standardized protocols and hence are suitable for bulk deployments. Among the fastest-growing segments are active tags based on the need to access location tracking in real-time and sensor-enabled environmental monitoring, which provides longer reading ranges and is programmable. Semi-passive tags are niche and offer sensory capabilities with reduced power consumption; that is, they use batteries to sense and readers to communicate.

“Fixed readers constitute the dominant deployment architecture through automated zone monitoring and access control integration capabilities, while handheld readers exhibit the fastest growth supporting field audits, exception investigation, and distributed facility management requirements.”

The data center RFID market is segmented by reader type into Fixed Reader and Handheld. Fixed readers have the greatest proportion and are installed at the entrance, cages, aisles, and storage areas to allow continuous automated asset tracking, movement tracking, and connection with access control and audit systems. The most popular category is the fastest-expanding segment of the handheld readers, and it is inspired by the need to perform periodic audits, process exceptions, manage remote sites, and work in the field. These mobile devices enable speedy bulk scanning and identification of discrepancies and special searches of assets without infrastructural considerations. Growth is high in enterprise, colocation, and edge environments where flexibility and cost-effective inventory checking and real-time database synchronization are necessary.

“Ultra-High Frequency (UHF) systems dominate both current installations and growth trajectories through superior read range, simultaneous multi-tag reading capability, and global standardization enabling cost-effective tag manufacturing and deployment.”

The data center RFID market is segmented by frequency type into Low Frequency, High Frequency, and Ultra-High Frequency. The highest and fastest-growing share is UHF, as it has the longest read range, scanning speed is fast, and it can be used to monitor the inventory bulk and zone level in the large data halls. Its low-cost passive tags and international EPC Gen2 standardization enable large-scale deployments to be cost-effective. HF is used in niche applications, where there is a need to integrate short-range reading or access control, whereas LF is the smallest segment, which is restricted to special or legacy applications that have very short read ranges.

“Colocation facilities drive substantial RFID adoption through multi-tenant asset segregation imperatives and customer service level agreement requirements, while hyperscale data centers demonstrate the fastest growth propelled by massive infrastructure scale and automation-driven operational models.”

The data center RFID market is segmented by data center type into Hyperscale, Colocation, Enterprise, and Edge. Colocation centers are another large segment because of multi-tenant asset segregation, SLA compliance, and automated inventory tracking needs. Facilities that are hyperscale exhibit the most rapid growth, due to their huge scale of infrastructure needing full automation, high-speed bulk scanning, real-time location visibility, and incorporation with advanced deployment systems. Enterprise data centers are gradually implementing RFID as a means of meeting audit requirements, lifecycle management, and efficiency. The new high-growth segment is the edge facilities, which utilize RFID to view the assets remotely and manage distributed sites in which on-site monitoring and manual controls are constrained.

“North America leads the data center RFID market, driven by hyperscale infrastructure concentration and technology sector maturity, while Asia-Pacific demonstrates the fastest regional growth, fueled by aggressive digital transformation and data center construction programs.”

The data center RFID market is segmented by region into North America, Europe, Asia Pacific, and the Rest of the World. North America is the largest market with regard to data center RFID, with high hyperscale implementations, stringent compliance systems, and developed DCIM integration, where the U.S. leads in adoption. Europe is next with GDPR stimulated localization, energy efficiency requirements, and powerful asset governance in Germany, the UK, and France. Asia Pacific is the quickest expanding region, with data localization policies of China at the forefront, the operational rigour of Japan, and the growing capacity of India for hyperscale. The Rest of the World, Latin America, and the Middle East experience the emergence of adoption due to the growth of colocation and digital transformation programs and regulatory modernization, and Africa is nascent but growing slowly with rising regional investments in data centers.

Know the high-growth countries in this report. Register Here

Most of the major players compete in some of the governing factors, including price, product offerings, and regional presence, etc. The following are the key players in the data center RFID market. Some of the major players provide a complete range of products.

Here is the list of the Top Players (Based on Dominance)

Note: The above list does not necessarily include all the top players in the market.

Are you the leading player in this market? We would love to include your name. Please write to us at [email protected]

This report provides market intelligence most comprehensively. The report structure has been kept so that it offers maximum business value. It provides critical insights into market dynamics and will enable strategic decision-making for existing market players as well as those willing to enter the market. The following are the key features of the report:

The global data center RFID market is segmented into the following categories.

Data Center RFID Market by Application Type

Data Center RFID Market by Tag Type

Data Center RFID Market by Reader Type

Data Center RFID Market by Frequency Type

Data Center RFID Market by Data Center Type

Data Center RFID Market by Region Type

With this detailed report, Stratview Research offers one of the following free customization options to our respectable clients:

Company Profiling

Competitive Benchmarking

Custom Research: Stratview Research offers custom research services across industries. In case of any custom research requirement related to market assessment, competitive benchmarking, sourcing and procurement, target screening, and others, please send your inquiry to [email protected]

By 2032, the global data center RFID market is expected to increase at a compound annual growth rate (CAGR) of 16.4%.

The global data center RFID market is projected to reach US$ 3.5 billion by 2032, growing from US$ 1.0 billion in 2023.

Data center RFID (Radio Frequency Identification) refers to the deployment of RFID tags, readers, antennas, and software platforms to enable automated identification, tracking, and management of IT assets, racks, cables, and infrastructure components within data center environments. It enhances asset visibility, lifecycle management, audit compliance, and operational efficiency through real-time or near-real-time data capture.

Key drivers include hyperscale and colocation expansion, rising AI-driven infrastructure complexity, demand for real-time asset visibility, regulatory compliance requirements, reduction of manual tracking errors, RFID integration with DCIM and BMS platforms, and expanding edge data center deployments requiring remote monitoring.

High-growth segments include Environmental & Operational Monitoring, Active Tags, Handheld Readers, Ultra-High Frequency Systems, and Colocation Data Centers.

North America holds the largest market share, driven by hyperscale concentration, mature colocation infrastructure, efficiency regulations, technology leadership, and ongoing data center modernization and replacement cycles.

Leading players in the global data center RFID market include Avery Dennison Corporation, Impinj Inc., Zebra Technologies Corporation, Honeywell International Inc., HID Global Corporation, Eaton Corporation plc, Fujitsu Limited, Invengo Information Technology Co., Ltd., RF Code, Inc., and NXP Semiconductors N.V..

Emerging trends include AI-enabled asset analytics, integration with DCIM and BMS platforms, IoT-connected smart readers, passive UHF adoption for rack-level automation, real-time location visibility, predictive maintenance insights, and edge-ready RFID deployments supporting distributed data center infrastructure.

WE ACCEPT