404

+1-313-307-4176

Data Center Rack Market Report

Data Center Racks Market Size, Share, Trend, Forecast, Competitive Analysis, and Growth Opportunity: 2025-2032

Data Center Racks Market is segmented by Application Type (Server Rack, Network Rack, and Storage Rack), by Rack Type (Open Frame and Enclosure), by Rack Size Type (<=42U and >42U), by Rack Density Type (<10 kW, 10-20 kW, and >20 kW), by Data Center Type (Hyperscale, Colocation, Enterprise, and Edge) and by Region (North America [The USA, Canada, and Mexico], Europe [The UK, Germany, France, and Rest of Europe], Asia-Pacific [China, Australia, Japan, India, and Rest of Asia-Pacific], and Rest of the World [Brazil, Africa, and Others]).

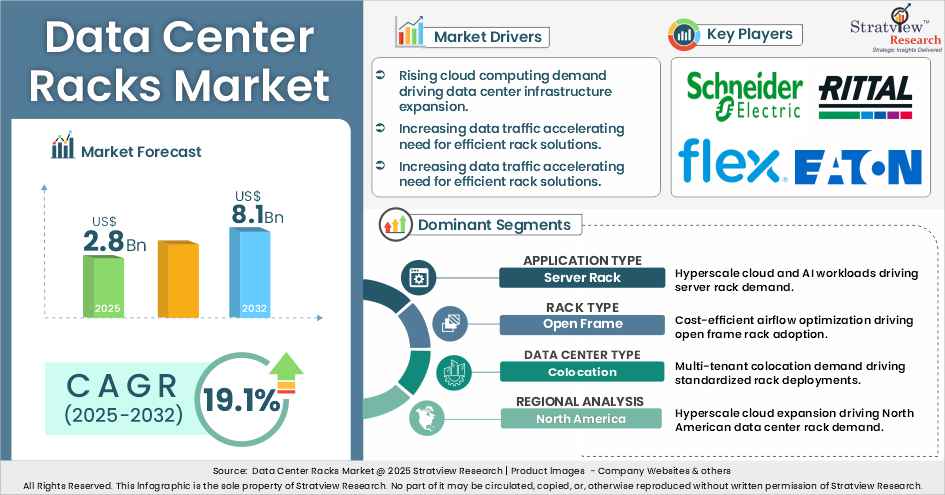

“The Data Center Racks Market size was US$ 2.8 billion in 2025 and is likely to grow at an impressive CAGR of 19.1% in the long run to reach US$ 8.1 billion in 2032.”

Want to get a free sample? Register Here

Introduction

Data center racks are at the heart of modern IT infrastructure, providing structured enclosures for servers, storage, and networking equipment while ensuring efficient use of space, power, and cooling. Racks come in several types, including enclosed cabinets for security and airflow management, open-frame racks for easy access, wall-mounted racks for space-constrained environments, high-density racks for GPU-heavy or high-performance computing, and advanced liquid-cooled racks for AI and high-density workloads. Standard 19-inch racks with modular designs support scalable power distribution, structured cabling, and optimized airflow, enabling efficient operation in cloud, hyperscale, and edge data centers. Leading manufacturers such as Schneider Electric, Vertiv, Rittal, Eaton, and Legrand are driving innovation, delivering reliable solutions to meet the demands of next-generation workloads.

Hyperscale and Cloud Expansion

Edge Computing Infrastructure

High Initial Investment

High-Density Power and Cooling Challenges

Advancements in Thermal Management Technology

Smart Rack Technology

|

Segmentations |

List of Sub-Segments |

Segments with High-Growth Opportunity |

|

Application-Type Analysis |

Server Rack, Network Rack, and Storage Rack. |

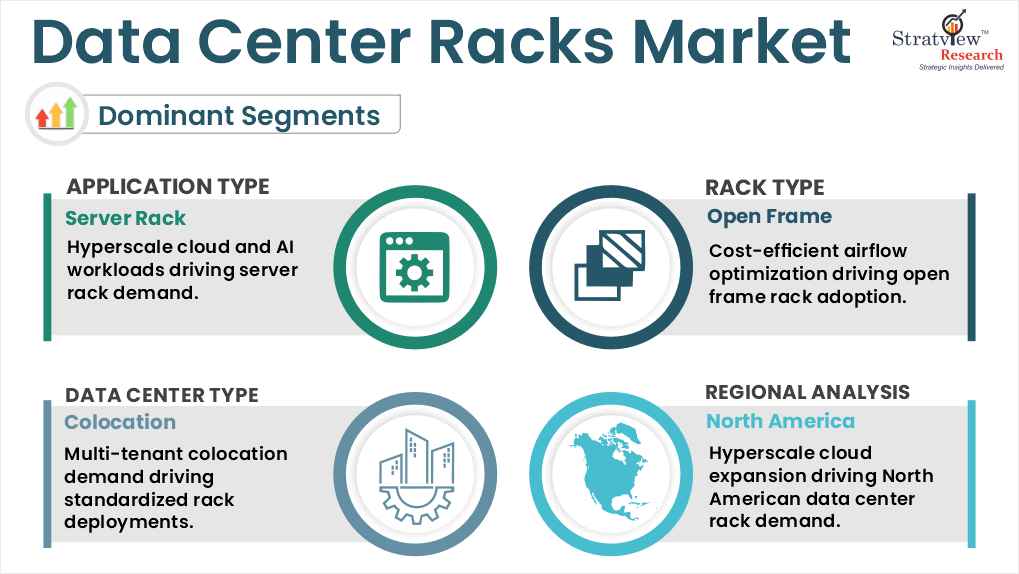

Server Rack is both the largest and the fastest-growing application segment. |

|

Rack-Type Analysis |

Open Frame and Enclosure. |

Open Frame accounts for the largest share; Enclosure is the fastest-growing segment. |

|

Rack-Size-Type Analysis |

≤42U and >42U. |

≤42U racks dominate current installations; >42U racks are the slightly faster-growing segment. |

|

Rack-Density-Type Analysis |

<10 kW, 10–20 kW, and >20 kW. |

10–20kW represents the largest density tier; >20kW is the fastest-growing, driven by AI workloads. |

|

Data-Center-Type Analysis |

Hyperscale, Colocation, Enterprise, and Edge. |

Colocation facilities drive substantial rack adoption, while Hyperscale data centers demonstrate the fastest growth. |

|

Region Analysis |

North America, Europe, Asia-Pacific, and The Rest of the World. |

North America leads the market through concentrated hyperscale facilities, while Asia-Pacific grows fastest. |

By Application Type

“Server racks dominate both market share and growth trajectory, underpinned by hyperscale cloud expansion and AI/GPU cluster buildouts, while network and storage rack segments maintain steady demand driven by bandwidth upgrades and exploding data volume growth, respectively.”

The Data Center Racks Market is segmented by application into Server Rack, Network Rack, and Storage Rack. Server racks dominate the data center racks market in both share and growth, driven by hyperscale cloud expansion, enterprise IT modernization, and large-scale AI deployments. Increasing adoption of GPU-intensive workloads requires high-density enclosures capable of supporting heavy equipment and advanced cooling systems. Modern AI servers often demand reinforced rack structures, enhanced airflow, and high-capacity power distribution units. These evolving performance requirements, combined with continuous investments in cloud infrastructure, are accelerating the deployment of server racks and strengthening their leadership position across hyperscale and enterprise data centers.

Network and storage racks continue to experience steady demand as bandwidth requirements and data volumes expand rapidly. Growing adoption of high-speed connectivity standards, including 100GbE, 400GbE, and emerging 800GbE technologies, is driving the need for scalable and organized network rack solutions. Meanwhile, the surge in unstructured data from AI, video streaming, and enterprise applications is increasing demand for storage racks designed to handle heavy loads and high-capacity configurations. These trends ensure consistent growth for both segments, complementing the strong momentum observed in server rack deployments.

By Rack Type

“Open frame racks dominate the market through cost efficiency and superior airflow characteristics, while enclosure racks are the fastest-growing type, driven by high-density AI deployments, colocation security requirements, and the adoption of hot/cold aisle containment architectures.”

The Data Center Racks Market is segmented by rack type into Open Frame and Enclosure. Open frame racks hold the largest share in the data center racks market due to their cost efficiency, excellent airflow characteristics, and ease of maintenance. These racks provide unobstructed cooling paths, making them highly compatible with precision air-based cooling systems used in hyperscale and telecom environments. Their simple design allows quick equipment installation, flexible cable management, and convenient access for upgrades or servicing. Additionally, adoption of standardized two- and four-post architectures supported by open infrastructure initiatives further strengthens demand, particularly in large-scale deployments where operational simplicity and efficient thermal performance are critical.

Enclosure racks, however, are witnessing the fastest growth as data centers transition toward high-density computing and enhanced security requirements. Increasing rack power densities exceeding traditional thresholds are driving the adoption of enclosed designs that support advanced cooling methods such as rear-door heat exchangers. Colocation facilities also favor enclosure racks to ensure equipment protection and controlled access for multiple tenants. Furthermore, the growing implementation of hot- and cold-aisle containment strategies to improve energy efficiency is accelerating deployment. These factors collectively position enclosure racks as a key growth segment in modern data center infrastructure.

By Rack Size Type

“The ≤42U rack remains the dominant size category as the global industry standard, while the >42U format is the slightly faster-growing tier as operators seek to maximize rack-unit yield per floor tile footprint in high-cost metropolitan data center markets.”

The Data Center Racks Market is segmented by rack size into ≤42U and >42U configurations. Since 42U has long been the industry norm, widely used in government, business, and colocation facilities, and compatible with the majority of server form factors, the ≤42U category has the biggest share. The demand for replacements is still driven by its sizable installed base. As operators add additional equipment, PDUs, and cabling to maximize capacity within the same footprint, the >42U segment (45U–48U) is expanding more quickly. The 48U configuration is becoming more popular, especially in European colocation markets where the cost of floor space is high.

By Rack Density Type

“The 10–20kW density tier commands the largest market share across the global installed base, while the >20kW segment is the fastest-growing, fundamentally redefining data center power and thermal architecture as AI workloads concentrate compute at unprecedented density levels.”

The Data Center Racks Market is segmented by rack density into <10kW, 10–20kW, and >20kW tiers. With typical x86 servers and air-cooling systems, the 10–20kW category accounts for the majority of enterprise, colocation, and cloud deployments. For edge deployments with lower density requirements, telecom rooms, and legacy configurations, the <10kW sector is still relevant. Driven by AI infrastructure like GPU and accelerator-based systems, the >20kW segment is expanding at the quickest rate, frequently surpassing 40kW per rack. These deployments, which are anticipated to rise significantly in the upcoming years, call for sophisticated cooling technologies, including liquid cooling and rear-door heat exchangers.

By Data Center Type

“Colocation facilities represent the largest data center type segment, driven by multi-tenant infrastructure demands and SLA compliance requirements, while Hyperscale data centers are the fastest-growing, fueled by relentless AI-driven cloud expansion and ultra-high-density rack procurement programs.”

The Data Center Racks Market is segmented by data center type into Hyperscale, Colocation, Enterprise, and Edge. Due to the company's migration to third-party facilities that offer standardized racks and scalable deployments, colocation data centers have the highest share. In order to offer a variety of configurations and maintain demand across rack types, operators purchase racks in bulk. With increasing rack density fueled by AI and GPU clusters, hyperscale facilities are the sector with the greatest rate of growth. While edge facilities, an emerging market, deploy small, durable racks for latency-sensitive applications like 5G, autonomous systems, and smart manufacturing, enterprise data centers demonstrate consistent demand through continuous upgrades.

Want to get more details about the segmentations? Register Here

By Region Type

“North America leads the global Data Center Racks Market through its unmatched concentration of hyperscale cloud campuses and AI infrastructure investment, while Asia-Pacific is the fastest-growing region driven by unprecedented data center construction activity across China, India, and Southeast Asia.”

North America leads the global data center racks market, supported by a dense concentration of hyperscale cloud campuses and large-scale AI infrastructure investments. Major cloud providers such as Amazon Web Services, Microsoft Azure, Google Cloud, and Meta continue expanding across key U.S. regions, driving demand for high-density rack deployments. These facilities require advanced rack solutions capable of supporting GPU clusters, optimized airflow, and high-capacity power distribution. Additionally, strong colocation activity, enterprise cloud migration, and early adoption of modular data center architectures further reinforce North America’s dominant position in the global market.

Asia-Pacific is the fastest-growing region, fueled by rapid data center construction across China, India, and Southeast Asia. Increasing internet penetration, digital transformation initiatives, and rising cloud adoption are encouraging large-scale infrastructure investments. Governments are also supporting data localization policies, further accelerating regional deployments. Europe remains a mature yet steadily growing market, driven by sustainability-focused upgrades and regulatory compliance requirements. Meanwhile, emerging regions, including Brazil, the Middle East, and Africa, are witnessing gradual growth as enterprises and colocation providers expand digital infrastructure, creating additional opportunities for rack manufacturers worldwide.

Most of the major players compete in some of the factors, including price, service offerings, regional presence, etc. The following are the key players in the data center rack market -

Note: The above list does not necessarily include all the top players in the market.

Are you a leading player in this market? We would love to include your name. Please write to us at [email protected]

This report provides market intelligence most comprehensively. The report structure has been kept so that it offers maximum business value. It provides critical insights into market dynamics and will enable strategic decision-making for existing market players as well as those willing to enter the market.

The following are the key features of the report:

|

Market Study Period |

2019-2032 |

|

Base Year |

2024 |

|

Forecast Period |

2025-2032 |

|

Trend Period |

2019-2023 |

|

Number of Tables & Figures |

>100 |

|

Number of Segments Analysed |

5 (Application Type, Rack Type, Rack-Size Type, Rack-Density Type, Data-Center-Type and Region) |

|

Number of Regions Analysed |

4 (North America, Europe, Asia-Pacific, Rest of the World) |

|

Countries Analysed |

15 (The USA, Canada, Mexico, Germany, France, Italy, The UK, China, Japan, India, Brazil, Saudi Arabia, Rest of Europe, Rest of APAC, and Rest of the World) |

|

Free Customization Offered |

10% |

|

After Sales Support |

Unlimited |

|

Report Presentation |

Complimentary |

|

Market Dataset |

Complimentary |

|

Further Deep Dive & Consulting Services |

10% Discount |

This report provides market intelligence most comprehensively. The report structure has been kept so that it offers maximum business value. It provides critical insights into market dynamics and will enable strategic decision-making for existing market players as well as those willing to enter the market. The following are the key features of the report:

The global Data Center Racks Market is segmented into the following categories.

Data Center Racks Market by Application Type

Data Center Racks Market by Rack Type

Data Center Racks Market by Rack Size Type

Data Center Racks Market by Rack Density Type

Data Center Racks Market by Data Center Type

Data Center Racks Market by Region Type

With this detailed report, Stratview Research offers one of the following free customization options to our respected clients:

Company Profiling

Competitive Benchmarking

Custom Research: Stratview Research offers custom research services across industries. In case of any custom research requirement related to market assessment, competitive benchmarking, sourcing and procurement, target screening, and others, please send your inquiry to [email protected]

In data center settings, a data center rack is a standardized metal frame or enclosed cabinet used to install, arrange, and store IT equipment, such as servers, networking devices, storage arrays, and power distribution units. Racks are measured in rack units (U), where 1U is equivalent to 1.75 inches of vertical mounting space. Racks offer structural support, cable management, airflow management, and physical security for IT assets.

The global Data Center Racks Market is projected to reach US$ 8.1 billion by 2032, growing from US$ 2.8 billion in 2025.

By 2032, the global Data Center Racks Market is expected to increase at a compound annual growth rate (CAGR) of 19.1%.

Key drivers include rapid expansion of hyperscale cloud infrastructure, AI/ML workload-driven demand for high-density rack enclosures, edge computing deployments, enterprise data center modernization cycles, 5G network infrastructure buildouts, growing colocation adoption, and the shift to liquid-cooling-integrated rack designs to support elevated rack power densities exceeding 20kW per cabinet..

High-growth segments include Server Rack, Enclosure, >42U, >20 kW, Colocation Data Centers, and Asia-Pacific.

North America holds the largest market share, driven by hyperscale concentration, mature colocation infrastructure, efficiency regulations, technology leadership, and ongoing data center modernization and replacement cycles.

Asia-Pacific demonstrates the highest regional growth rate, fueled by aggressive digital transformation initiatives, massive data center construction programs across China and India, government infrastructure development policies, expanding cloud adoption, rising internet penetration, and e-commerce platform growth.

Open frame racks dominate the market by volume because of their cost-effectiveness, unrestricted airflow features, compatibility with precision air cooling systems, and widespread use in hyperscale and telecommunications applications. This segment's leadership position has been strengthened by the Open Compute Project (OCP), which has further standardized open-frame designs for large-scale cloud deployments.

WE ACCEPT