404

+1-313-307-4176

Biocomponent Fiber Market Report

Biocomponent Fiber Market Size, Share, Trend, Forecast, Competitive Analysis, and Growth Opportunity: 2026-2032

Biocomponent Fiber Market is segmented by Material Type (PE/PP, PE/PET, Co-PET/PET, and Others), by Structure Type (Sheath/Core, Side-by-Side, Islands-in-the-Sea, and Others), by End-Use Industry Type (Hygiene, Textiles, Automotive, Home Furnish, and Others), by Web Formation Technology Type (Drylaid, Spunlaid, Airlaid, and Wetlaid), by Consolidation Process Type (Spunlaid, Needlepunched, and Thermal Bonded), by Fiber Length Type (Short-Cut Fibers and Staple Fibers) and by Region (North America [The USA, Canada, and Mexico], Europe [Germany, France, The UK, Russia, and Rest of Europe], Asia-Pacific [China, Japan, India, and Rest of Asia-Pacific], and Rest of the World [Brazil, Saudi Arabia, and Others]).

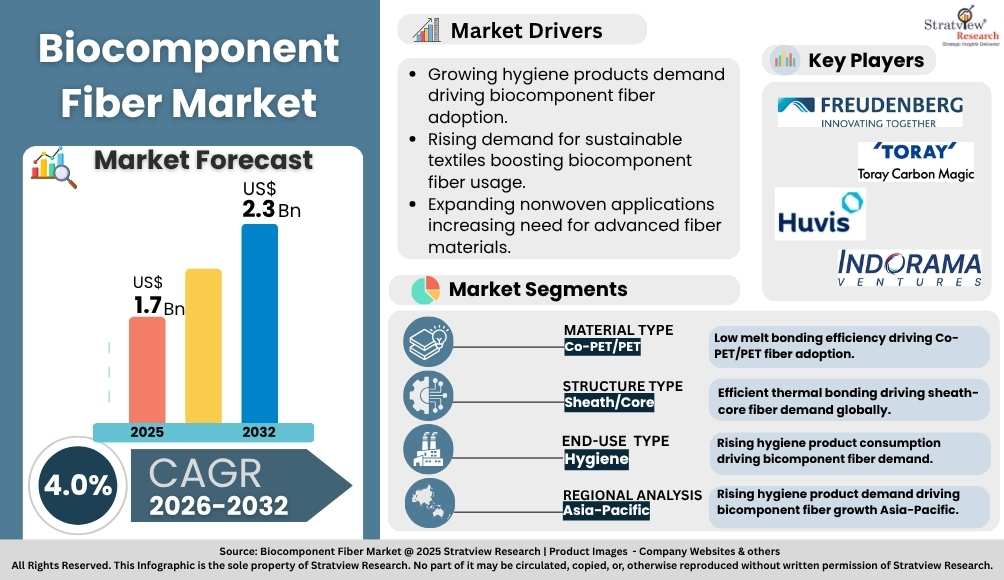

“The biocomponent fiber market size was US$ 1.7 billion in 2025 and is likely to grow at an impressive CAGR of 4.0% in the long run to reach US$ 2.3 billion in 2032.”

Want to get a free sample? Register Here

Bicomponent fibers represent a new generation of high-performance materials engineered by combining two distinct polymers within a single filament, typically arranged in sheath–core or side-by-side structures. This advanced construction enables properties that conventional single-polymer fibers cannot achieve, including superior bonding behavior, enhanced thermal response, optimized strength-to-weight ratios, and improved softness. Widely used polymer combinations such as polyester–polyethylene, polyester–polyester, polypropylene, and emerging bio-based systems allow manufacturers to tailor fibers for specific processing requirements and end-use applications. As industries increasingly seek multifunctional and lightweight materials, bicomponent fibers are gaining global traction across technical and nonwoven textile markets.

One of the primary drivers of the bicomponent fiber market is strong demand from hygiene and medical applications, where performance consistency and reliability are critical. Products such as diapers, sanitary napkins, wipes, and medical disposables rely heavily on the excellent thermal bonding efficiency and structural integrity offered by bicomponent fibers. Their ability to create strong, uniform nonwoven fabrics without chemical binders improves product safety and comfort while enhancing production efficiency. Rising healthcare expenditure, growing awareness of hygiene standards, and expanding populations, especially in emerging economies, continue to accelerate consumption in these high-volume, recurring-use segments.

Beyond hygiene, market growth is further supported by expanding applications in automotive interiors, filtration, home textiles, and industrial nonwovens. In automotive uses, bicomponent fibers enable lightweight structures, effective sound absorption, and improved thermal management, supporting vehicle efficiency targets. At the same time, stricter sustainability regulations and environmental concerns are encouraging the adoption of recyclable and bio-based fiber systems. Continuous advancements in fiber spinning technologies, material science, and product design are unlocking new functionalities, broadening application scope, and positioning bicomponent fibers as a key enabler of next-generation textile and nonwoven solutions.

A considerable number of strategic alliances, including M&As, JVs, etc., have been performed over the past few years:

|

Segmentations |

List of Sub-Segments |

Segments with High-Growth Opportunity |

|

Material-Type Analysis |

PE/PP, PE/PET, Co-PET/PET, and Others |

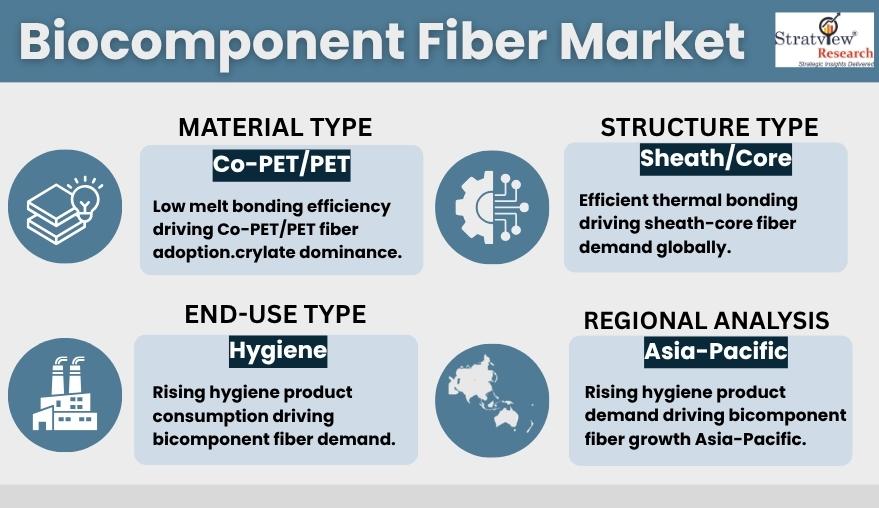

Co-PET/PET is expected to remain the dominant segment as well as the fastest-growing material type during the forecast period. |

|

Structure-Type Analysis |

Sheath/Core, Side-by-Side, Islands-in-the-Sea, and Others |

Sheath/Core structure type holds the major share in the bicomponent fiber market. |

|

End-Use-Industry-Type Analysis |

Hygiene, Textiles, Automotive, Home Furnish, and Others |

The hygiene end-use industry is expected to be the largest demand generator for bicomponent fiber. |

|

Web-Formation-Technology-Type Analysis |

Drylaid, Spunlaid, Airlaid, and Wetlaid |

Drylaid web formation type holds the major share in the bicomponent fiber market. |

|

Consolidation-Process-Type Analysis |

Spunlaid, Needlepunched, and Thermal Bonded |

The thermal bonded consolidation process type will be the dominant as well as the fastest growing segment in the bicomponent fiber market. |

|

Fiber Length-Type Analysis |

Short-Cut Fibers and Staple Fibers |

Short-cut fibers hold the major share in the bicomponent fiber market. |

|

Region Analysis |

North America, Europe, Asia-Pacific, and The Rest of the World |

Asia-Pacific is expected to remain the largest as well as the fastest-growing market over the next five years. |

“Co-PET/PET is expected to remain the dominant segment as well as the fastest-growing material type during the forecast period.”

The biocomponent fiber market is segmented by material type into PE/PP, PE/PET, Co-PET/PET, and others. Strongly led by Co-PET/PET in both value and volume shipments. Its dominance stems from widespread adoption across nonwoven applications, supported by a low melt temperature below 110°C that enables efficient thermal bonding. Additionally, Co-PET/PET offers an attractive balance of strength, lightweight performance, superior dyeability, wrinkle resistance, and cost efficiency, making it a preferred choice for hygiene, medical, and industrial nonwoven manufacturers globally.

Meanwhile, PE/PP bicomponent fibers are gaining notable traction due to their enhanced softness, bulkiness, and excellent liquid absorption characteristics. These properties make them especially suitable for hygiene and personal care products, where comfort and fluid management are critical. Strong demand from the United States and Western European markets further supports growth, driven by high hygiene standards, consumer preference for premium nonwoven products, and continuous innovation in disposable and absorbent material applications.

“Sheath/Core structure type holds the major share in the bicomponent fiber market.”

The biocomponent fiber market is segmented by structure type into sheath-core, side-by-side, islands-in-the-sea, and others. Led by sheath-core structures due to their extensive use as bonding fibers in nonwoven applications. These fibers are commonly produced in concentric designs to enhance strength or eccentric designs to improve bulkiness, allowing manufacturers to tailor performance to specific end uses. Their efficient thermal bonding and processing versatility drive widespread adoption. Meanwhile, side-by-side fibers present a strong growth opportunity, particularly as self-crimping fibers that enhance elasticity, softness, and dimensional stability across diverse nonwoven and textile applications.

“The hygiene end-use industry is expected to be the largest demand generator for bicomponent fiber.”

The biocomponent fiber market is segmented by end-use industry type into hygiene, textiles, automotive, home furnishing, and others. The hygiene segment governs the bicomponent fiber market and is expected to remain avant-garde in the foreseeable future as well. Improving the living standard of people, raising awareness towards good health, and inclination towards the use of hygiene products, such as baby diapers, wipes, and feminine hygiene products, are driving the demand for bicomponent fibers in the segment. Key requirements for hygiene products, such as softness, better fluid absorption, low irritation to the skin, high strength, and high bulkiness, are efficiently fulfilled by bicomponent fiber.

“Drylaid web formation type holds the major share in the bicomponent fiber market.”

The biocomponent fiber market is segmented by web formation technology type into drylaid, spunlaid, airlaid, and wetlaid. with drylaid technology emerging as the most dominant segment during the forecast period. Its leadership is driven by the high degree of design freedom it offers when processing bicomponent fibers. Manufacturers can fine-tune fabric properties by modifying polymer combinations and ratios, enabling precise control over melting points, bonding efficiency, and thermal behavior. As a result, drylaid webs can deliver tailored strength, stiffness, and heat resistance, making them well-suited for performance-driven applications across hygiene, technical textiles, filtration, and industrial nonwovens.

“Thermal bonded consolidation process type will be the dominant as well as the fastest growing segment in the bicomponent fiber market.”

The biocomponent fiber market is segmented by consolidation process type into spunlaid, needlepunched, and thermal bonded. The thermal bonded consolidation process segment is expected to be the dominant as well as the fastest growing consolidation process during the forecast period. This process creates a non-woven fabric with unique properties such as enhanced strength, durability, and elasticity. The choice of bicomponent fibers and the specific thermal bonding process used can be tailored to create fabrics with a wide range of properties for different applications, such as in the manufacturing of medical textiles, protective clothing, and industrial fabrics.

“Short-cut fibers hold the major share in the bicomponent fiber market.”

The biocomponent fiber market is segmented by fiber length type into short-cut fibers and staple fibers. The short-cut fibers are expected to maintain their lead in terms of value and volume both during the forecast period. They are used in a wide range of applications, such as in the production of nonwoven fabrics, insulation materials, and filtration media. Short-cut fibers are often used as reinforcements in composite materials, such as plastics, to improve their mechanical properties.

Want to get more details about the segmentations? Register Here

“Asia-Pacific is expected to remain the largest as well as the fastest-growing market over the next five years.”

Asia-Pacific dominates the global bicomponent fiber market and is expected to sustain its leadership while also registering the fastest growth over the long term. This strong position is supported by a large and growing population, rising disposable incomes, and increasing awareness of personal hygiene and healthcare products such as baby diapers, wipes, and feminine hygiene products. Rapid urbanization, changing lifestyles, and expanding middle-class populations are accelerating consumption. Additionally, the presence of large-scale nonwoven manufacturing hubs and cost-competitive production further strengthens Asia-Pacific’s dominance in both volume and value terms.

Emerging economies such as China and India are witnessing a sharp rise in bicomponent fiber usage, driven by expanding hygiene, medical, and textile industries alongside supportive government initiatives and foreign investments. In contrast, North America and Europe represent mature yet lucrative markets with high penetration of bicomponent fibers across hygiene, automotive, and technical textile applications. These regions continue to offer sizeable opportunities, supported by innovation, sustainability-focused product development, and steady demand for high-performance and eco-friendly fiber solutions.

The market is highly consolidated. Most of the major players compete in some of the governing factors, including price, product offerings, and regional presence, etc. The following are the key players in the biocomponent fiber market. Some of the major players provide a complete range of products.

Here is the list of the Top Players (Based on Dominance)

Note: The above list does not necessarily include all the top players in the market.

Are you the leading player in this market? We would love to include your name. Please write to us at [email protected]

This report provides market intelligence most comprehensively. The report structure has been kept so that it offers maximum business value. It provides critical insights into market dynamics and will enable strategic decision-making for existing market players as well as those willing to enter the market. The following are the key features of the report:

The global biocomponent fiber market is segmented into the following categories.

Biocomponent Fiber Market by Material Type

Biocomponent Fiber Market by Structure Type

Biocomponent Fiber Market by End-Use Industry Type

Biocomponent Fiber Market by Web Formation Technology Type

Biocomponent Fiber Market by Consolidated Process Type

Biocomponent Fiber Market by Fiber Length Type

Biocomponent Market by Region Type

With this detailed report, Stratview Research offers one of the following free customization options to our respectable clients:

Company Profiling

Competitive Benchmarking

Custom Research: Stratview Research offers custom research services across industries. In case of any custom research requirement related to market assessment, competitive benchmarking, sourcing and procurement, target screening, and others, please send your inquiry to [email protected]

The bicomponent fiber market is estimated to grow at a CAGR of 4.0% by 2032, driven by increasing penetration of nonwoven fabrics, growing per capita income, growing disposable income, increasing awareness about health and hygiene, and the benefits of using bicomponent fiber as compared to traditional materials.

Far Eastern New Century Corporation, Indorama Ventures, Freudenberg Group, Huvis Corporation, Toray Industries, Inc, Jiangsu Jiangnan High Polymer Fiber Co., Ltd., and Cha Technologies Group are the leading players in the bicomponent fiber market.

Asia Pacific is estimated to remain dominant in the bicomponent fiber market in the foreseeable future, owing to a host of factors such as a large population base, increasing disposable income of consumers, and increasing awareness of hygiene products such as diapers and feminine hygiene products. Emerging nations, such as China and India, are experiencing a rapid increase in the usage of bicomponent fiber.

The hygiene segment governs the bicomponent fiber market and is expected to remain avant-garde in the foreseeable future as well. Improving the living standard of people, raising awareness towards good health, and inclination towards the use of hygiene products, such as baby diapers, wipes, and feminine hygiene products, are driving the demand for bicomponent fibers in the segment.

Sheath-core structure leads the bicomponent fiber market. This structure type fiber is generally processed as a bonding fiber for non-wovens. Typically, these are used in two forms, concentric and eccentric types, based on the emphasis on product strength and bulkiness, respectively.

The drylaid web formation technology is expected to be the dominant segment during the forecast period, because this formation technology is used to create fabrics with different levels of strength, stiffness, and heat resistance, as well as other properties that are useful in a variety of applications.

The thermal-bonded consolidation process is expected to be the dominant consolidation process in the market in the coming years. This process creates a non-woven fabric with unique properties such as enhanced strength, durability, and elasticity.

The short-cut fibers are expected to maintain their lead in the bicomponent fiber market during the forecast period. They are used in a wide range of applications, such as in the production of nonwoven fabrics, insulation materials, and filtration media. Short-cut fibers are often used as reinforcements in composite materials, such as plastics, to improve their mechanical properties.

WE ACCEPT