Market Analysis | 2024-2032")

404

+1-313-307-4176

Data Center Computer Room Air Handler (CRAH) Market Analysis | 2024-2032

Market Analysis | 2024-2032")

Data Center Computer Room Air Handler (CRAH) Market Size, Share, Trend, Forecast, Competitive Analysis, and Growth Opportunity: 2024-2032

Data Center Computer Room Air Handler (CRAH) Market is segmented by Product Type (Perimeter, In-row, and Overhead), by Cooling Capacity Type (<100 kW, 100-300 kW, >300 kW), by Data Center Type (Hyperscale, Colocation, Enterprise, and Edge), and by Region (North America [The USA, Canada, and Mexico], Europe [Germany, France, The UK, Russia, and Rest of Europe], Asia-Pacific [China, Australia, Japan, India, and Rest of Asia-Pacific], and Rest of the World [Brazil, Africa, and Others]).

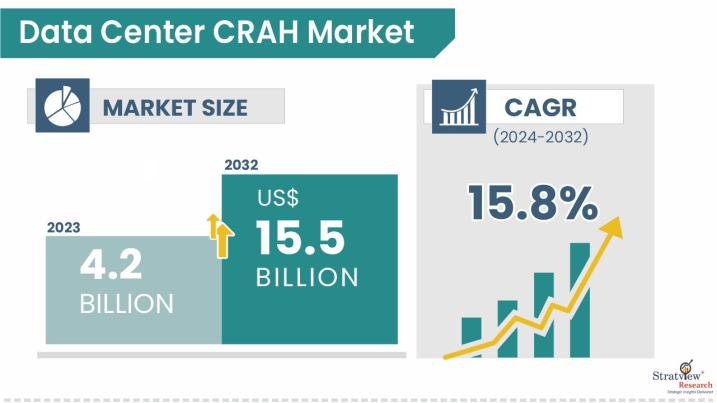

The data center computer room air handler (CRAH) market size was USD 4.2 billion in 2023 and is likely to grow at an impressive CAGR of 15.8% during 2024-2032 to reach USD 15.5 billion in 2032.

Want to know more about the market scope? Register Here

The Data Center Computer Room Air Handler (CRAH) market plays a vital role in supporting the thermal stability and operational reliability of modern data centers and mission-critical IT environments. CRAH units are air-based cooling systems engineered for precise temperature and humidity control, ensuring optimal performance of sensitive computing equipment. Unlike conventional comfort cooling systems, CRAH units operate without compressors and instead rely on centrally supplied chilled water to remove heat from recirculated air. This design delivers superior energy efficiency, simplified system architecture, and improved environmental control across high-availability computing facilities.

Market growth is being driven by rising rack densities fueled by artificial intelligence, cloud computing, and high-performance workloads that generate intense heat loads. Increasing focus on energy efficiency and sustainability is accelerating the adoption of CRAH systems equipped with variable-speed fans, intelligent controls, and seamless integration with building management systems. Additionally, the rapid expansion of edge data centers is creating demand for compact, modular, and scalable cooling solutions capable of operating efficiently under variable loads. These factors collectively position CRAH systems as a cornerstone technology in next-generation data center cooling strategies.

A considerable number of strategic alliances, including M&As, JVs, etc., have been performed over the past few years:

|

Segmentations |

List of Sub-Segments |

Segments with High-Growth Opportunity |

|

Product-Type Analysis |

Perimeter, In-row, and Overhead |

Perimeter CRAH systems lead the market, and In-row CRAH systems are the fastest-growing too, due to the rapid growth of large data centers. |

|

Cooling-Capacity-Type Analysis |

<100kW, 100-300kW, and >300kW |

The >300 kW segment leads installations; similarly,>300 kW CRAH units grow fastest for hyperscale, high-density computing. |

|

Data-Center-Type Analysis |

Hyperscale, Colocation, Enterprise, and Edge |

Colocation data centers drive steady CRAH demand, while hyperscale facilities grow fastest due to cloud investment and high-power workloads. |

|

Region Analysis |

North America, Europe, Asia-Pacific, and The Rest of the World |

North America leads the market, while Asia-Pacific grows fastest, driven by rapid digitalization and data center infrastructure investment. |

“Perimeter CRAH systems capture the largest market share through superior thermal management precision and scalability, and In-row have the fastest growth driven by hyperscale facility requirements and space optimization benefits.”

By product type, the data center CRAH market is segmented into Perimeter, In-row, and Overhead. Perimeter CRAH systems continue to represent the largest share of the data center CRAH market, supported by their proven reliability, room-based cooling approach, and compatibility with traditional data center layouts. These systems provide uniform airflow distribution and integrate effectively with hot- and cold-aisle containment strategies, making them a preferred choice for colocation and enterprise facilities. Their scalability, ease of maintenance, and cost-effectiveness further reinforce widespread adoption, particularly in large facilities where centralized cooling remains practical and efficient for managing moderate-to-high heat loads.

In-row CRAH systems are emerging as the fastest-growing segment, driven by hyperscale expansion, rising rack power densities, and the need for close-coupled cooling solutions. By positioning cooling units directly between server racks, in-row systems minimize airflow losses, improve thermal efficiency, and enable precise temperature control for high-density zones. This design supports modular growth and targeted cooling, making it ideal for AI and HPC environments. Overhead CRAH systems are also gaining traction in space-constrained and next-generation facilities, though their adoption remains comparatively limited.

“CRAH systems in the >300 kW range lead current installed base, and they also exhibit the fastest growth supporting extreme density requirements in hyperscale infrastructure.”

By cooling capacity type, the data center CRAH market is segmented into <100 kW, 100-300 kW, and >300 kW. CRAH systems in the >300 kW capacity range represent both the largest installed base and the fastest-growing segment of the data center CRAH market, CRAH systems with the highest cooling capacities command a leading position in the data center market, reflecting the rapid evolution of hyperscale infrastructure and compute-intensive workloads. The surge in artificial intelligence, machine learning, and high-performance computing has significantly increased rack densities, making high-capacity cooling essential. CRAH units in this range efficiently manage concentrated heat loads, support centralized chilled-water architectures, and enable operators to deploy fewer yet more powerful cooling systems. This consolidation improves energy efficiency, simplifies airflow management, and enhances scalability across large-scale data center campuses.

The growth momentum of this segment is further reinforced by hyperscale expansion strategies that prioritize modularity, future-ready designs, and operational efficiency. Operators are increasingly shifting investments toward high-density environments, reducing reliance on mid-capacity systems over time. While CRAH units in the mid-capacity range continue to serve enterprise and colocation facilities, their relative importance is gradually declining. Lower-capacity CRAH systems are now largely confined to edge sites and legacy facilities, as new deployments favor advanced, high-capacity solutions aligned with modern data center performance demands.

“Colocation facilities drive substantial CRAH demand through continuous expansion cycles and infrastructure upgrades, while hyperscale data centers demonstrate the highest growth rates fueled by cloud infrastructure investments and AI workload proliferation.”

The data center CRAH market is segmented by cooling data center type into hyperscale, colocation, enterprise, and edge. Colocation data centers are expected to maintain their dominant position in the data center CRAH market throughout the forecast period, supported by the growing preference for shared infrastructure and cost-efficient cooling solutions. Enterprises across industries increasingly rely on colocation facilities to scale IT capacity without heavy capital investment, driving consistent demand for reliable, energy-efficient CRAH systems. High equipment utilization, multi-tenant environments, and the need for precise temperature and humidity control further strengthen adoption. Additionally, frequent retrofit activities and upgrades to improve energy efficiency sustain long-term CRAH demand in colocation facilities.

Hyperscale data centers are anticipated to emerge as the fastest-growing segment in the CRAH market, driven by rapid expansion of cloud computing, artificial intelligence, and high-performance computing workloads. These facilities operate at extremely high rack densities, requiring advanced, high-capacity CRAH systems capable of handling concentrated thermal loads. Hyperscale operators prioritize scalable, modular cooling architectures that improve efficiency while reducing operational complexity. Continuous investments by global technology leaders, combined with rising data consumption and digital transformation initiatives, are accelerating CRAH adoption across hyperscale data center deployments worldwide.

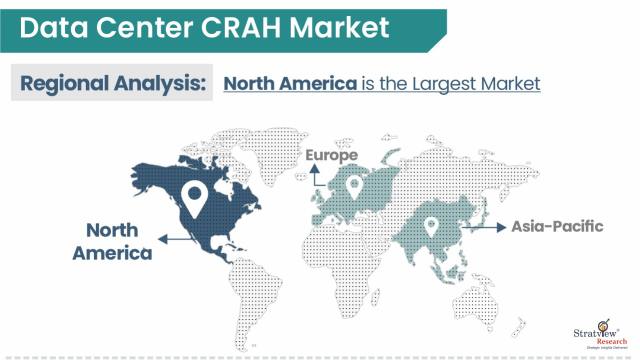

“North America leads the data center CRAH market, driven by hyperscale infrastructure concentration and technology sector maturity, while Asia-Pacific demonstrates the fastest regional growth fueled by aggressive digital transformation and data center construction programs.”

North America continues to hold the largest share of the Data Center Computer Room Air Handlers (CRAH) market, driven by its mature data center ecosystem and early adoption of advanced cooling technologies. The region hosts a dense concentration of hyperscale and colocation data centers, supported by strong cloud adoption, AI deployment, and digital transformation initiatives. High awareness of energy efficiency, stringent thermal management standards, and widespread integration of chilled-water cooling infrastructure further strengthen CRAH demand. Additionally, the presence of leading data center operators, technology providers, and established supply chains reinforces North America’s sustained market leadership.

Asia-Pacific is emerging as the fastest-growing region in the CRAH market, propelled by rapid data center construction, expanding digital economies, and surging internet and cloud usage. Countries such as China, India, Japan, and Southeast Asian nations are witnessing strong investments in hyperscale and edge facilities to support AI workloads, 5G rollout, and growing data consumption. Increasing focus on energy-efficient cooling, favorable government policies, and rising colocation demand are accelerating CRAH adoption. As operators prioritize scalable, high-capacity cooling solutions, Asia-Pacific is positioned for robust and sustained growth.

Know the high-growth countries in this report. Register Here

The market is moderately consolidated, with the presence of a fair number of players. Most of the major players compete in some of the governing factors, including price, product offerings, and regional presence, etc. The following are the key players in the data center computer room air handler (CRAH) market. Some of the major players provide a complete range of products.

Here is the list of the Top Players (Based on Dominance)

Note: The above list does not necessarily include all the top players in the market.

Are you the leading player in this market? We would love to include your name. Please write to us at [email protected]

This report provides market intelligence most comprehensively. The report structure has been kept so that it offers maximum business value. It provides critical insights into market dynamics and will enable strategic decision-making for existing market players as well as those willing to enter the market. The following are the key features of the report:

The global data center computer room air handler (CRAH) market is segmented into the following categories.

Data Center Computer Room Air Handler (CRAH) Market by Data Center Type

Data Center Computer Room Air Handler (CRAH) Market by Cooling Capacity Type Type

Data Center Computer Room Air Handler (CRAH) Market by Product Type

Data Center Computer Room Air Handler (CRAH) Market by Region Type

With this detailed report, Stratview Research offers one of the following free customization options to our respected clients:

Company Profiling

Competitive Benchmarking

Custom Research: Stratview Research offers custom research services across industries. In case of any custom research requirement related to market assessment, competitive benchmarking, sourcing and procurement, target screening, and others, please send your inquiry to [email protected].

A data center CRAH is a precision air-side cooling unit using chilled water to condition recirculated air, delivering efficient temperature and humidity control without integrated refrigeration compressors.

The global data center computer room air handler (CRAH) market is projected to reach US$ 15.5 billion by 2032, growing from US$ 4.2 billion in 2023.

By 2032, the global data center computer room air handler (CRAH) market is expected to increase at a compound annual growth rate (CAGR) of 15.8%.

Key drivers include hyperscale and colocation expansion, rising AI-driven rack densities, strict energy-efficiency mandates, sustainability goals, edge computing growth, and replacement of aging data center cooling infrastructure.

High-growth segments include overhead CRAH systems, >300 kW units for high-density deployments, edge data center solutions, intelligent CRAH platforms with predictive analytics, and high-efficiency models using advanced fans and heat exchangers.

North America holds the largest market share, driven by hyperscale concentration, mature colocation infrastructure, efficiency regulations, technology leadership, and ongoing data center modernization and replacement cycles.

Asia-Pacific demonstrates the highest regional growth rate, fueled by aggressive digital transformation initiatives, massive data center construction programs across China and India, government infrastructure development policies, expanding cloud adoption, rising internet penetration, and e-commerce platform growth.

Leading players in the global data center CRAH market include Vertiv Holdings Co., Schneider Electric SE, STULZ GmbH, Johnson Controls International plc, Carrier Global Corporation, Modine Manufacturing Company, Nortek Air Solutions, Munters Group AB, Rittal GmbH and Daikin Industries, Ltd.

WE ACCEPT