Market Analysis | 2024-2032")

404

+1-313-307-4176

Data Center Computer Room Air Conditioning (CRAC) Market Analysis | 2024-2032

Market Analysis | 2024-2032")

Data Center Computer Room Air Conditioning (CRAC) Market Size, Share, Trend, Forecast, Competitive Analysis, and Growth Opportunity: 2024-2032 ... See more

Data Center Computer Room Air Conditioning (CRAC) Market is segmented by Product Type (Perimeter, In-row, and Overhead), by Cooling Capacity Type (<100 kW, 100-300 kW, >300 kW), by Data Center Type (Hyperscale, Colocation, Enterprise, and Edge), and by Region (North America [The USA, Canada, and Mexico], Europe [Germany, France, The UK, Russia, and Rest of Europe], Asia-Pacific [China, Japan, Australia, India, and Rest of Asia-Pacific], and Rest of the World [Brazil, Africa, and Others]).

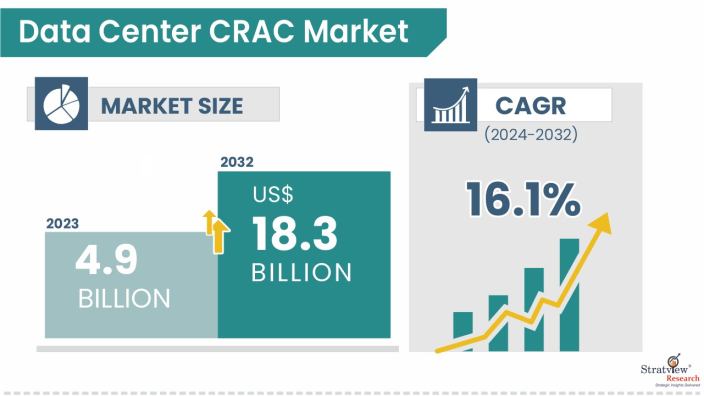

The data center computer room air conditioning (CRAC) market size was USD 4.9 billion in 2023 and is likely to grow at an impressive CAGR of 16.1% during 2024-2032 to reach USD 18.3 billion in 2032.

Want to know more about the market scope? Register Here

The Data Center Computer Room Air Conditioner (CRAC) market plays a vital role in supporting thermal stability across mission-critical IT environments where precise temperature and humidity control are essential. CRAC units are self-contained, air-based cooling systems equipped with integrated compressors and refrigeration circuits, enabling independent operation without reliance on centralized chilled-water infrastructure. This flexibility makes them ideal for edge, modular, and enterprise data centers. Modern CRAC systems feature variable-speed compressors, optimized airflow designs, advanced filtration, and intelligent controls that seamlessly integrate with building management systems to ensure reliable, consistent cooling performance.

Market growth is being driven by the expansion of distributed IT architectures, rising adoption of edge and modular data centers, and the need for rapid, plug-and-play cooling deployment. Increasing rack densities, fluctuating thermal loads, and heightened reliability requirements are further reinforcing demand for autonomous cooling solutions. Additionally, advancements in energy-efficient compressors, smart monitoring technologies, and sustainability-focused designs are enhancing CRAC system efficiency and operational flexibility. As data center operators prioritize resilience, scalability, and minimal infrastructure dependency, CRAC units continue to remain a preferred cooling choice across diverse data center environments.

A considerable number of strategic alliances, including M&As, JVs, etc., have been performed over the past few years:

Recent Product Development:

|

Segmentations |

List of Sub-Segments |

Segments with High-Growth Opportunity |

|

Product-Type Analysis |

Perimeter, In-row, and Overhead |

Perimeter CRAC systems lead the market, and the In-row CRACs are the fastest-growing too due to the rapid growth of large data centers. |

|

Cooling-Capacity-Type Analysis |

<100kW, 100-300kW, and >300kW |

The <100 kW segment leads installations; similarly, they show the fastest growth for hyperscale, high-density computing. |

|

Data-Center-Type Analysis |

Hyperscale, Colocation, Enterprise, and Edge |

Colocation data centers drive steady CRAC demand, while hyperscale facilities grow fastest due to cloud investment and high-power workloads. |

|

Region Analysis |

North America, Europe, Asia-Pacific, and The Rest of the World |

North America leads the market, while Asia-Pacific grows fastest, driven by rapid digitalization and data center infrastructure investment. |

“Perimeter CRAC systems capture the largest market share through superior thermal management precision and scalability, and In-row have the fastest growth driven by hyperscale facility requirements and space optimization benefits.”

Perimeter CRAC systems continue to dominate the data center CRAC market, largely due to their long-standing deployment across enterprise, colocation, and legacy facilities. These systems rely on room-based cooling architectures that deliver consistent airflow and integrate smoothly with hot- and cold-aisle containment strategies. Their proven reliability, ease of installation, and lower design complexity make them a preferred choice for operators managing moderate rack densities. Additionally, perimeter CRAC units align well with existing infrastructure, allowing data center owners to extend asset life while maintaining predictable thermal performance and operational stability.

In contrast, in-row CRAC systems are emerging as the fastest-growing segment, driven by hyperscale data center expansion and rapidly increasing rack power densities. By positioning cooling units closer to heat sources, in-row designs significantly reduce airflow losses and enhance thermal efficiency. This close-coupled approach supports precise temperature control, modular scalability, and effective cooling of high-density zones required by AI and high-performance computing workloads. Overhead CRAC systems are also gaining selective traction in space-constrained and next-generation facilities, but their adoption remains niche compared to the accelerating momentum of in-row solutions.

“CRAC systems in the <100 kW range lead current installed base, and they also exhibit the fastest growth, supporting other utility areas along with main server rooms.”

The data center CRAC market is segmented by cooling capacity type into <100 kW, 100-300 kW, and >300 kW. CRAC units with cooling capacities below 100 kW represent the largest installed base in the data center CRAC market, reflecting their broad deployment across edge facilities, legacy enterprise data centers, and auxiliary technical spaces. These systems are well-suited for environments with lower rack densities, decentralized IT loads, and requirements for standalone, self-contained cooling. Their compact footprint, ease of installation, and operational flexibility make them ideal for supporting non-white-space areas such as network rooms, control centers, and power rooms, reinforcing steady demand and sustained adoption across diverse facility types.

CRAC systems in the 100–300 kW capacity range maintain strong relevance due to their optimal balance of scalability, redundancy, and cost efficiency, making them a preferred choice for enterprise and colocation data centers. These units support moderate to rising rack densities while allowing operators to design resilient cooling architectures without excessive overprovisioning. Although CRAC units above 300 kW are deployed selectively in large-scale or specialized facilities, overall market demand remains volume-driven, with lower-capacity systems continuing to dominate installations due to their versatility and alignment with distributed and hybrid data center designs.

“Colocation facilities drive substantial CRAC demand through continuous expansion cycles and infrastructure upgrades, while hyperscale data centers demonstrate the highest growth rates fueled by cloud infrastructure investments and AI workload proliferation.”

Colocation data centers are projected to maintain their dominant position in the CRAC market throughout the forecast period, driven by their diverse tenant requirements and need for flexible, reliable cooling solutions. CRAC systems are widely preferred in colocation facilities due to their self-contained design, ease of deployment, and ability to support mixed rack densities across multiple customers. Many colocation operators continue to rely on perimeter and in-row CRAC configurations for predictable airflow management, rapid scalability, and redundancy. The growing demand from enterprises outsourcing IT infrastructure further reinforces sustained CRAC adoption in this segment.

Hyperscale data centers are expected to be the fastest-growing segment in the CRAC market, supported by rapid expansion of cloud services, AI workloads, and distributed computing architectures. While CRAH systems dominate large centralized campuses, CRAC units are increasingly deployed in modular, edge-adjacent, and specialized hyperscale environments where chilled-water infrastructure is limited or rapid deployment is required. Their ability to operate independently, handle variable loads, and support phased capacity expansion makes CRAC solutions attractive for hyperscale operators seeking agility, resilience, and accelerated time-to-market in high-growth digital ecosystems.

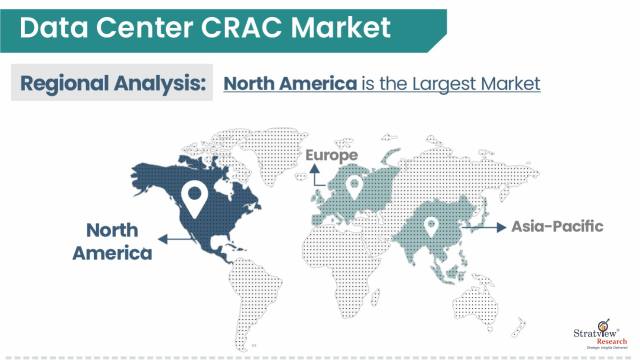

“North America leads the data center CRAH market, driven by hyperscale infrastructure concentration and technology sector maturity, while Asia-Pacific demonstrates the fastest regional growth, fueled by aggressive digital transformation and data center construction programs.”

North America dominates the data center CRAC market due to its well-established data center ecosystem, high density of mission-critical facilities, and continuous investments in cloud and colocation infrastructure. The region’s strong focus on operational resilience, redundancy, and regulatory compliance favors the adoption of reliable, self-contained CRAC systems. Moreover, modernization of aging enterprise data centers and the expansion of edge deployments to support low-latency applications continue to drive steady replacement demand, reinforcing North America’s leadership in overall market share.

Asia-Pacific, meanwhile, is experiencing the fastest growth in the data center CRAC market as digital economies expand rapidly across emerging and developed countries alike. Accelerated rollout of hyperscale and colocation data centers, rising data consumption, and increasing adoption of AI and cloud services are fueling new capacity additions. CRAC systems are particularly attractive in this region due to their flexibility, faster installation, and suitability for modular builds, supporting the region’s robust and sustained growth trajectory.

Know the high-growth countries in this report. Register Here

The market is moderately consolidated, with the presence of a fair number of players. Most of the major players compete in some of the governing factors, including price, product offerings, and regional presence, etc. The following are the key players in the data center computer room air conditioning (CRAC) market. Some of the major players provide a complete range of products.

Here is the list of the Top Players (Based on Dominance)

Note: The above list does not necessarily include all the top players in the market.

Are you the leading player in this market? We would love to include your name. Please write to us at [email protected]

This report provides market intelligence most comprehensively. The report structure has been kept so that it offers maximum business value. It provides critical insights into market dynamics and will enable strategic decision-making for existing market players as well as those willing to enter the market. The following are the key features of the report:

The data center computer room air conditioning (CRAC) market is segmented into the following categories.

By Data Center Type

By Cooling Capacity Type

By Product Type

By Region

With this detailed report, Stratview Research offers one of the following free customization options to our respected clients:

Company Profiling

Competitive Benchmarking

Custom Research: Stratview Research offers custom research services across industries. In case of any custom research requirement related to market assessment, competitive benchmarking, sourcing and procurement, target screening, and others, please send your inquiry to [email protected].

A data center CRAC is a precision air-side cooling unit that conditions recirculated air using an integrated refrigeration system with built-in compressors, delivering accurate temperature and humidity control without reliance on centralized chilled water infrastructure.

The global data center computer room air conditioning (CRAC) market is projected to reach USD 18.3 billion by 2032, growing from USD 4.9 billion in 2023.

By 2032, the global data center computer room air conditioning (CRAC) market is expected to increase at a compound annual growth rate (CAGR) of 16.1%.

Key drivers include hyperscale and colocation expansion, rising AI-driven rack densities, strict energy-efficiency mandates, sustainability goals, edge computing growth, and replacement of aging data center cooling infrastructure.

High-growth segments include In-row CRAC systems, <100 kW units for high-density deployments, edge data center solutions, intelligent CRAC platforms with predictive analytics, and high-efficiency models using advanced fans and heat exchangers.

North America holds the largest market share, driven by hyperscale concentration, mature colocation infrastructure, efficiency regulations, technology leadership, and ongoing data center modernization and replacement cycles.

Asia-Pacific demonstrates the highest regional growth rate, fueled by aggressive digital transformation initiatives, massive data center construction programs across China and India, government infrastructure development policies, expanding cloud adoption, rising internet penetration, and e-commerce platform growth.

Leading players in the global data center CRAC market include Vertiv Holdings Co., Schneider Electric SE, STULZ GmbH, Johnson Controls International plc, Carrier Global Corporation, Modine Manufacturing Company, Nortek Air Solutions, Munters Group AB, Rittal GmbH and Daikin Industries, Ltd.

WE ACCEPT