404

+1-313-307-4176

Aerospace Elastomers Market Analysis | 2025-2034

Aerospace Elastomers Market Size, Share, Trend, Forecast, Competitive Analysis, and Growth Opportunity: 2025-2034

Aerospace Elastomers Market Is segmented by Platform Type (Commercial Aircraft, Regional Aircraft, General Aviation, Helicopter, Military Aircraft, and Spacecraft), by Elastomer Type (EPDM, Silicone, Fluoroelastomers, Nitrile Butadiene Rubber, Neoprene, and Other Elastomers), by Product Type (Seals, Gaskets, Encapsulation (Potting), and Other Products), by Application Type (Airframe; Propulsion; Interior; Landing Gear, Wheels, and Brakes; and Hydraulic & Actuation), and by Region (North America [The USA, Canada, and Mexico], Europe [Germany, France, The UK, Russia, and Rest of Europe], Asia-Pacific [China, Japan, India, and Rest of Asia-Pacific], and Rest of the World [Brazil, Saudi Arabia, and Others]).

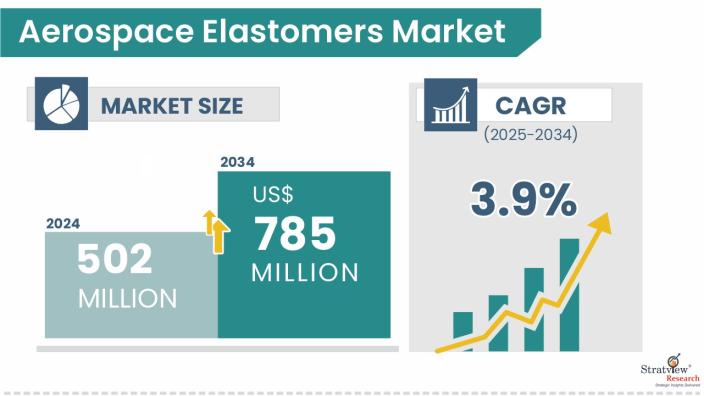

“The aerospace elastomers market size was US$ 502 million in 2024 and is likely to grow at a decent CAGR of 3.9% in the long run to reach US$ 785 million in 2034.”

Want to know more about the market scope? Register Here

Aerospace elastomers are high-performance rubber-like materials engineered to perform in extreme aerospace environments involving high temperatures, pressure variations, fuel exposure, and mechanical stress. Commonly used in sealing, vibration damping, and insulation, elastomers such as silicone, EPDM, and fluorocarbon-based compounds play critical roles in aircraft airframes, engines, interiors, and hydraulic systems. These materials offer excellent chemical resistance, thermal stability, and mechanical resilience, making them ideal for mission-critical aerospace applications.

The aerospace elastomers market is growing steadily due to rising global aircraft production, increased adoption of lightweight and high-performance sealing solutions, and growing demand for fuel-efficient next-gen aircraft. The integration of elastomeric components in propulsion and hydraulic systems is increasing in both OE and MRO segments. Furthermore, the push for weight reduction and operational efficiency in aerospace platforms is promoting the use of advanced elastomers that meet stringent safety and performance standards. Regulatory emphasis on fire, smoke, and toxicity (FST) compliance is further influencing elastomer formulation and certification trends.

A considerable number of strategic alliances, including M&As, JVs, etc., have been performed over the past few years:

|

Segmentations |

List of Sub-Segments |

Segments with High-Growth Opportunity |

|

Platform-Type Analysis |

Commercial Aircraft, Regional Aircraft, General Aviation, Military Aircraft, Helicopter, and Spacecraft |

Commercial aircraft are likely to continue to lead as the dominant platform of the market. |

|

Elastomer-Type Analysis |

EPDM, Silicone, Fluoroelastomers, Nitrile Butadiene Rubber, Neoprene, and Other Elastomers |

Fluoroelastomers took an indubitable lead (in terms of value) in the market, followed by silicone. |

|

Product-Type Analysis |

Seals, Gaskets, Encapsulation (Potting), and Other Products |

Seals lead the market throughout the study period, as their critical operating environment requires advanced and highly engineered materials. |

|

Application-Type Analysis |

Airframe; Propulsion; Interior; Landing Gear, Wheels, and Brakes; and Hydraulic & Actuation |

Airframe and propulsion are likely to remain the most attractive applications in the market. |

|

Regional Analysis |

North America, Europe, Asia-Pacific, and the Rest of the World |

North America is expected to continue to rank as the largest market in the coming years |

“Commercial aircraft is likely to continue leading the market, while also maintaining the fastest growth during 2025-2034.”

Based on platform type, the market is segmented into commercial aircraft, regional aircraft, general aviation, military aircraft, helicopter, and spacecraft.

Commercial aircraft dominate the aerospace elastomers market due to their high production volume and the extensive use of elastomeric products across multiple systems such as airframe, propulsion, interiors, and hydraulic lines. Seals and gaskets are used extensively in commercial aircraft fuel systems, hydraulic lines, and environmental systems for leak prevention and chemical resistance, especially with fluoroelastomers and silicone grades.

Despite aircraft deliveries plummeting in 2024, the market experienced staunch growth, fueled by consistent demand from a high number of aircraft in operation, spare parts, and leading players’ strategies against the unrelenting, volatile supply chain fiasco. OEMs' and tier players' stocking strategy has resulted in brimming inventories, which is ultimately likely to cause a growth slowdown in the market in 2025. Growth within the segment is well-backed by huge order backlogs of 15,304 (Airbus: 8,695 and Boeing: 6,609) commercial aircraft as of November 2025. Growth is further bolstered by increasing cabin retrofitting activities and higher maintenance frequencies in aging fleets.

Though spacecraft captured a minimal share in 2024, it is likely to offer healthy growth opportunities in the future. Spacecraft applications require ultra-high-performance elastomers capable of withstanding radiation, vacuum, and thermal extremes.

“Silicone and fluoroelastomers are likely to continue to lead in performance-critical applications, while EPDM remains a staple in general sealing.”

The market is segmented into EPDM, Silicone, Fluoroelastomers, Nitrile Butadiene Rubber (NBR), Neoprene, and Other Elastomers.

Fluoroelastomers took the biggest chunk of the pie in 2024 and are consistently gaining traction, owing to their excellent properties, such as outstanding high-temperature and weather resistance. Fluoroelastomers such as FKM are widely used in fuel systems, O-rings, and engine oil seals due to their exceptional resistance to oils, fuels, and hydraulic fluids. Their importance is growing with the shift toward sustainable aviation fuels and advanced propulsion systems.

Silicone elastomers are widely used in aerospace applications due to their -60 °C to 300 °C thermal stability, weathering resistance, and versatility across HTV, RTV, and LSR forms. Their inertness and performance across a wide temperature range make them ideal for door seals, thermal shielding, and engine interface components.

In the aerospace industry, fluoroelastomers are overwhelmingly used in seal and gasket applications, while silicone elastomers are preferred for hybrid components, overmolding, potting, and other molded aerospace parts. EPDM offers flexibility down to -55 °C, making it ideal for airframe seals and gaskets in cold or high-altitude conditions.

“Seals are likely to maintain their throne with the highest share in the market during the forecast period.”

Based on the product type, the market is segmented into seals, gaskets, encapsulation (potting), and other products. Seals, particularly O-rings, lip seals, and static seals, make up the bulk of elastomer usage in aerospace systems. These are deployed in airframes, hydraulic lines, fuel tanks, and brake systems where leakage prevention and chemical compatibility are essential. Modern platforms such as the A350 and B787 operate with higher-pressure fuel and hydraulic systems, driving even greater reliance on premium materials for seals.

Gaskets are vital in joining surfaces within propulsion systems, environmental control units, and air duct assemblies. These require high-precision molds and robust sealing under thermal cycling. Encapsulation products, including potting compounds, are gaining traction due to the increasing complexity and miniaturization of electronic modules. The need to protect sensitive avionics and electrical connectors from moisture, vibration, and EMI is accelerating adoption, especially in fly-by-wire and eVTOL platforms.

“Airframe, one of the most demanding areas of application is projected to remain at the forefront throughout the forecast period.”

Based on the application type, the market is segmented into airframe, propulsion, interior, landing gear, wheels and brakes, and hydraulic & actuation. Airframe applications use elastomers for door seals, fuselage panel gaskets, wing root fairings, and thermal insulation, areas exposed to wide pressure and temperature variations. Propulsion systems, including engines and nacelles, demand high-performance elastomers for thermal shielding, vibration damping, and sealing joints exposed to jet fuel, lubricants, and bleed air. Fluoroelastomers and silicone compounds dominate here. Elastomers are used in engine pylons or for anti-vibration mounts, or to isolate systems. Hutchinson SA is a large elastomer seal and vibration-control supplier in aerospace. Their aerospace-rubber business includes FKM, silicone, perfluoro-elastomer, etc. Fire seals (for engines, doors, pylons) often use specialized elastomers or fabric-reinforced elastomers. Freudenberg provides fireproof seals for engines/nacelles.

Landing gear and braking systems rely on elastomeric seals and bushings to handle shock loads, extreme pressures, and exposure to hydraulic fluids and debris.

“North America is expected to maintain its dominance, while Asia-Pacific is projected to witness the highest growth over the forecast period.”

North America is expected to remain the largest market for aerospace elastomers during the forecast period, underpinned by its position as the world’s leading aerospace manufacturing hub. The region is home to major OEMs like Boeing, Lockheed Martin, Raytheon Technologies, and GE Aerospace, along with a robust network of the aerospace supply chain. The high production rates of commercial aircraft, cutting-edge military programs like the F-35, B-21 Raider, and KC-46, keep the market demand highly active. The region also leads in technological innovation, including the integration of automation, Industry 4.0 monitoring, and environmentally friendly processing techniques.

Whereas, the Asia-Pacific region is expected to be the fastest-growing area, fueled by a rapid increase in aircraft manufacturing capacity, rising defense budgets, and the localization of supply chains. Countries such as China, India, and Japan are making significant investments in original equipment (OE), backed by homegrown aircraft programs like the COMAC C919, HAL Tejas, and Mitsubishi SpaceJet, as well as major fleet expansions.

Know the high-growth countries in this report. Register Here

The aerospace elastomers market presents a distinctly different competitive landscape for silicone elastomers and fluoroelastomers. The following are the key players in the aerospace elastomers market.

Here is the list of the Top Players (Distinct players for Silicone and Fluoroelastomers)

Note: The above list does not necessarily include all the top players in the market.

Are you the leading player in this market? We would love to include your name. Please write to us at [email protected]

This report provides market intelligence most comprehensively. The report structure has been kept so that it offers maximum business value. It provides critical insights into market dynamics and will enable strategic decision-making for existing market players as well as those willing to enter the market. The following are the key features of the report:

The global aerospace elastomers market is segmented into the following categories.

Aerospace Elastomers Market, by Platform Type

Aerospace Elastomers Market, by Elastomer Type

Aerospace Elastomers Market, by Product Type

Aerospace Elastomers Market, by Application Type

Aerospace Elastomers Market, by Region

With this detailed report, Stratview Research offers one of the following free customization options to our respected clients:

Company Profiling

Competitive Benchmarking

Custom Research: Stratview Research offers custom research services across industries. In case of any custom research requirement related to market assessment, competitive benchmarking, sourcing and procurement, target screening, and others, please send your inquiry to [email protected]

The report is delivered digitally through our online portal. Buyers receive login credentials from our team to access the report and may update their credentials at any time after the initial login.

Delivery timelines depend on the status of the report:

For the most accurate delivery timeline, please contact us to confirm the current status of the report.

Yes. You may request a complimentary preview of the report through a video conference with our team.

Yes. The scope of the report can be fully customized to align with your specific research objectives and information requirements.

Please contact us at [email protected], and our team will be happy to discuss your requirements and propose a tailored solution.

Yes. Selected sections of the report can be purchased separately based on your requirements. Please contact us at [email protected] to discuss your needs.

Yes, AI can help gather publicly available information, but its outputs are only as reliable as the data it accesses. Stratview Research reports are built using validated data, extensive primary interviews with industry stakeholders, and the expertise of our experienced research team.

Additionally, many critical insights, including market dynamics, competitive intelligence, and industry-specific trends, are not publicly available and therefore cannot be captured through AI alone.

The aerospace elastomers market is estimated to grow at a CAGR of 3.9% by 2034, driven by increasing aircraft production rates, increasing aircraft production rates, increased adoption of lightweight and high-performance sealing solutions, and growing demand for fuel-efficient next-gen aircraft.

Elkem ASA, Evonik Industries AG, Freudenberg & Co. KG, Momentive Performance Materials, Inc., Shin-Etsu Chemical Co., Ltd., The Dow Chemical Company, TransDigm, and Wacker Chemie AG are the leading players in the aerospace elastomers market.

North America is estimated to remain dominant in the aerospace elastomers market in the foreseeable future. North America remains a leading market driven by large OEMs (Boeing, GE, Collins, UTC/Pratt & Whitney suppliers) and a deep MRO network that sustains steady demand for high-performance seals, gaskets, and specialty elastomers. The region’s strict reliance on AMS and MIL material qualifications means suppliers must maintain wide, certified elastomer portfolios and local manufacturing to support fast delivery needs.

Asia-Pacific is estimated to remain the fastest-growing market in the foreseeable future, driven by the rapid expansion of commercial airline fleets, increasing defense modernization programs, and rising indigenous aircraft production in countries like China and India.

Commercial aircraft is expected to remain the largest segment of the aerospace elastomers market during the study period, driven by surging global air passenger traffic, accelerated production of fuel-efficient aircraft models such as the Airbus A320neo and Boeing 737 MAX, increasing adoption of lightweight and high-performance materials, and the rising need for fuel efficiency.

WE ACCEPT