404

+1-313-307-4176

Eva Film Market Report

EVA Film Market Size, Share, Trend, Forecast, Competitive Analysis, and Growth Opportunity: 2025-2031

EVA Film Market segmented by Type (Standard EVA Films and Anti-PID EVA Films), by Production method (Extrusion and Casting), by Application (Solar Panel Encapsulation, Lamination, and Heat Seal), by End Use Industry (Renewable Energy, Packaging, and Automotive), and by Region (North America [The USA, Canada, and Mexico], Europe [Germany, France, The UK, Russia, and Rest of Europe], Asia-Pacific [China, Japan, India, and Rest of Asia-Pacific], and Rest of the World [Brazil, Saudi Arabia, and Others]).

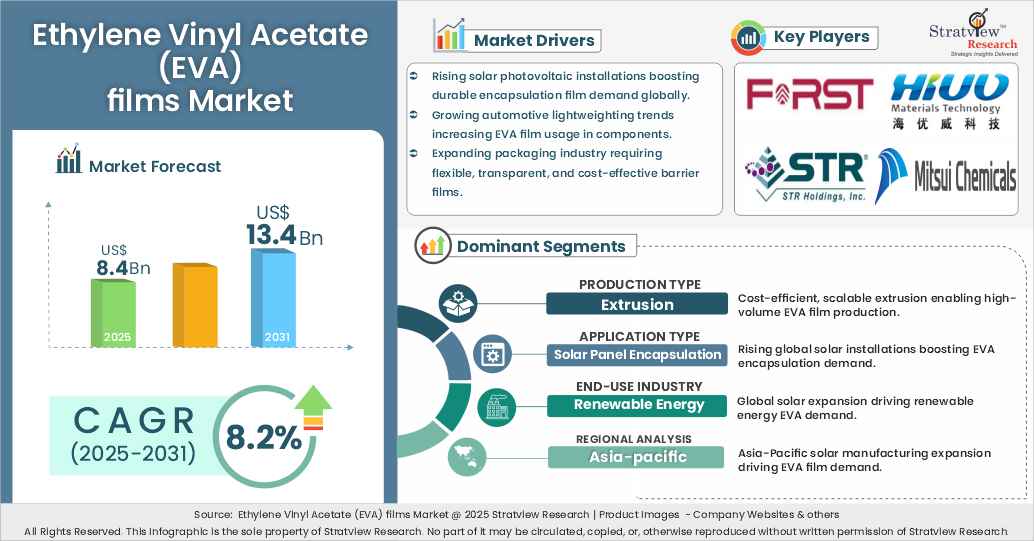

“The EVA film market size value was US$8.4 billion in 2025 and is likely to grow at a robust CAGR of 8.2% in the long run to reach US$13.4 billion in 2031.”

Want to get a free sample? Register Here

Introduction

Ethylene Vinyl Acetate (EVA) films consist of a specialized polymeric material with toughness, flexibility, and superior optical clarity. They are a copolymer of ethylene and vinyl acetate and are used in various industries due to their superior adhesive properties, thermal stability, and resistance to UV. EVA films also appear in the solar industry in the form of encapsulants for photovoltaic (PV) modules, protecting solar cells from moisture, dirt, and mechanical stress. EVA films are also employed in packaging, laminated glass, agriculture, and electronics, where clarity and strength with elasticity are most critical.

Increased emphasis on sustainable energy, high-performance construction materials, and creative packaging has transformed the demand for films across the world. EVA films are extensively utilized because of their resistance to extreme temperatures, in both industrial and consumer uses. The development of new technologies and changes in legislation that seek to preserve the environment have led to increased dependence on EVA films, and this is expected to persist in the future.

Recent Market Developments:

A considerable number of strategic alliances, market development, etc., have been performed over the past few years:

Recent JVs, acquisitions, mergers:

|

Segmentations |

List of Sub-Segments |

Segments with High-Growth Opportunity |

|

Type Analysis |

Standard EVA Films and Anti-PID EVA Films |

Anti-PID EVA films are the faster growing type because they prevent power loss in solar panels due to anti-PID property, making them more reliable for long-term and high-performance solar applications. |

|

Production Method Analysis |

Extrusion and Casting |

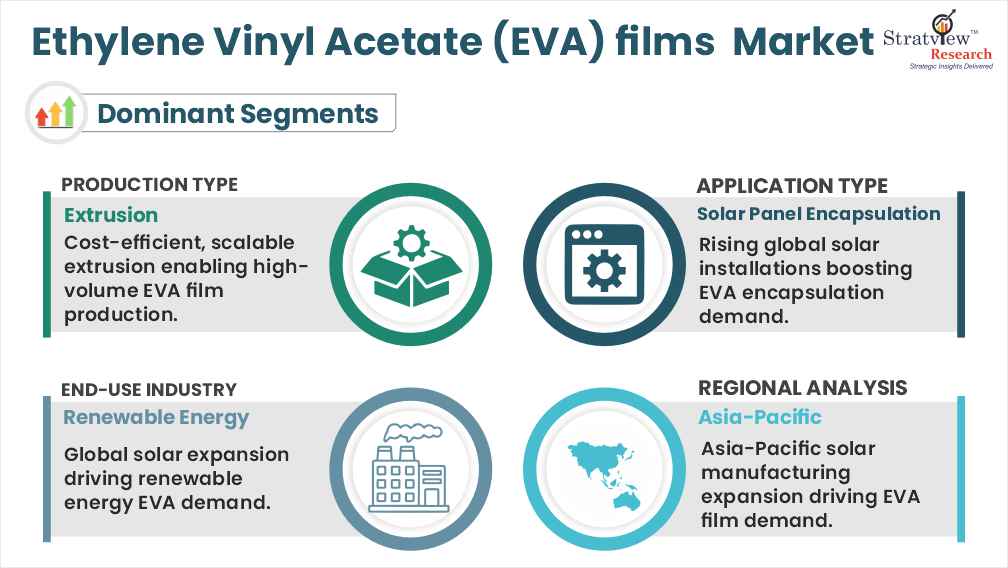

Extrusion is the dominant and faster-growing EVA film production method for EVA film production due to its cost efficiency, speed, and suitability for applications like solar encapsulation and packaging. |

|

Application Analysis |

Solar Panel Encapsulation, Lamination, and Heat Seal |

Solar panel encapsulation is expected to experience the fastest growth in the forecasted period due to the rising global adoption of solar energy systems. |

|

End Use Industry |

Renewable Energy, Packaging, and Automotive

|

Due to the global surge in sustainable energy, especially solar energy deployment, renewable energy is the leading and fastest-growing end-use industry for EVA films. |

|

Region Analysis |

North America, Europe, Asia-Pacific, and The Rest of the World |

Asia-Pacific is both the largest and fastest-growing region for the EVA films market, driven by its dominance in solar module manufacturing and strong industrial growth. |

By Type

“Anti-PID EVA films are witnessing the fastest growth, fueled by the rising demand for improved protection and durability in solar modules.”

Standard EVA films dominate the market because of their cost-effectiveness, good performance, and extensive application, particularly in the encapsulation of solar panels, packaging, and industry. They possess good transparency, adhesion, and flexibility, making them a good choice for bulk-conscious manufacturers. Their extensive application in established solar module production lines has ensured they maintain a considerable market share around the world.

Whereas, Anti-PID EVA films are expected to be the fastest-growing category, triggered by the growing awareness of Potential Induced Degradation (PID) and the demand for higher efficiency solar modules. As solar farms move into high-humidity and high-voltage conditions, demand for long durability and low power loss is spurring growth for Anti-PID solutions. These films are emerging as popular choices among high-end solar module manufacturers seeking to provide longer warranties and superior long-term performance

By Production Method Analysis

“Extrusion is the dominant and fastest-growing production method for EVA films, because of its cost-efficiency, scalability, and high-quality output.”

Extrusion leads the EVA films market because it can easily produce large quantities and high-performance films at low cost. It is common in most of the high-demand applications, such as solar panel encapsulation, flexible, and construction materials. The method provides greater control of film thickness, uniformity, and mechanical strength, favouring large-scale industrial applications. Due to an increase in demand for efficient and scalable production, extrusion continues to be the dominant and preferred manufacturing method in the EVA films market.

Want to get more details about the segmentations? Register Here

Application Analysis

“Solar panel encapsulation is the dominant and fastest-growing application of EVA films, driven by the global acceleration in solar energy installations and the need for long-lasting, high-performance encapsulants.”

The solar panel encapsulation is the dominant and fastest growing application of EVA films, because EVA films are used in the solar panel encapsulation, which is important in protecting the photovoltaic (PV) modules. EVA has high durability, UV stability, and good adhesion to glass and cells-excellent performance during extended use under changing environmental conditions. As the world has witnessed the explosive growth in solar capacity, the need to use high-quality encapsulation materials has multiplied.

By End-Use Industry

“Renewable energy is the dominant and fastest-growing end-use industry for EVA films, driven by the global surge in solar installations and the need for reliable encapsulation materials.”

EVA films find extensive applications in photovoltaic (PV) modules due to their longevity, resistance to UV, and protective characteristics, thus being critical to ensure long-term solar panel efficiency. China, India, and the U.S. are aggressively increasing solar capacity, driving demand for EVA encapsulants.

While consumer and packaging products also account for a considerable portion of EVA film usage, their expansion is relatively sluggish. Automotive uses are slowly on the rise, particularly in electric vehicles and lightweight parts, but are still a limited portion of the market. With aggressive policy encouragement and ongoing solar growth, renewable energy will likely propel the market growth of EVA film in the coming years

Regional Analysis

“The Asia-Pacific region is the dominant as well as the fastest-growing market in the EVA film, driven by the rapid expansion of solar energy, strong industrial growth, and rising demand for advanced packaging solutions.”

Key countries such as China, India, Japan, and South Korea are driving EVA film adoption, particularly for solar panel encapsulation. China's huge solar manufacturing facilities and India's ambitious renewable energy targets are major growth drivers. Government policies favouring domestic manufacturing growth and improvement in anti-PID EVA technology are further enhancing the market share of the region. With increasing supply chain localization, the Asia-Pacific region is poised to retain its leadership in production as well as consumption of EVA films.

The market is moderately fragmented, with over 80 players. Most of the major players compete in some of the governing factors, including price, service offerings, and regional presence, etc. The following are the key players in the EVA films market.

Here is the list of the Top Players (Based on Dominance)

Note: The above list does not necessarily include all the top players in the market.

Are you the leading player in this market? We would love to include your name. Please write to us at [email protected]

This report provides market intelligence most comprehensively. The report structure has been kept so that it offers maximum business value. It provides critical insights into market dynamics and will enable strategic decision-making for existing market players as well as those willing to enter the market. The following are the key features of the report:

The EVA films market is segmented into the following categories.

EVA films Market, by Type

EVA films Market, by Production method

EVA films Market, by Application

EVA films Market, by End Use Industry

EVA films Market by Region

With this detailed report, Stratview Research offers one of the following free customization options to our respected clients:

Company Profiling

Competitive Benchmarking

Custom Research: Stratview Research offers custom research services across sectors. In case of any custom research requirement related to market assessment, competitive benchmarking, sourcing and procurement, target screening, and others, please send your inquiry to [email protected]

The report is delivered digitally through our online portal. Buyers receive login credentials from our team to access the report and may update their credentials at any time after the initial login.

Delivery timelines depend on the status of the report:

For the most accurate delivery timeline, please contact us to confirm the current status of the report.

Yes. You may request a complimentary preview of the report through a video conference with our team.

Yes. The scope of the report can be fully customized to align with your specific research objectives and information requirements.

Please contact us at [email protected], and our team will be happy to discuss your requirements and propose a tailored solution.

Yes. Selected sections of the report can be purchased separately based on your requirements. Please contact us at [email protected] to discuss your needs.

Yes, AI can help gather publicly available information, but its outputs are only as reliable as the data it accesses. Stratview Research reports are built using validated data, extensive primary interviews with industry stakeholders, and the expertise of our experienced research team.

Additionally, many critical insights, including market dynamics, competitive intelligence, and industry-specific trends, are not publicly available and therefore cannot be captured through AI alone.

EVA films are a copolymer of ethylene and vinyl acetate, and films consist of a specialized polymeric material with toughness, flexibility, and superior optical clarity.

The EVA films market is forecasted to reach US$13.4 billion in 2031.

The EVA films market is expected to grow at a CAGR of 8.2% by 2031, driven by the rising use of solar energy systems across the world, with the EVA films used to encapsulate and protect solar modules against moisture, UV, and mechanical pressure.

Solar panel encapsulation is the dominant and fastest-growing application of EVA films, driven by the global acceleration in solar energy installations and the need for long-lasting, high-performance encapsulants.

The Asia-Pacific region is the dominant as well as the fastest-growing market in the EVA film market, driven by the rapid expansion of solar energy, strong industrial growth, and rising demand for advanced packaging solutions.

Hangzhou First Applied Material Co., Ltd., Shanghai HIUV New Materials Co., Ltd., STR Holdings, Inc., Mitsui Chemicals, Inc., Bridgestone, 3M, Hanwha Solutions, H.B. Fuller, Astenik Solar, and Guangzhou Lushan New Materials Co., Ltd., are the leading players in the EVA films market.

WE ACCEPT