404

+1-313-307-4176

Spunlaid Nonwoven Market Analysis | 2024-2031

Spunlaid Nonwoven Market Size, Share, Trends, Dynamics, Forecast, & Growth Analysis: 2024-2031

Spunlaid Nonwoven Market is segmented by Application Type (Hygiene, Automobile, Geotextile, Filtration, Medical, Building Roofing & Flooring, Foods & Beverages, and Other Applications), by Process Type (Spun-Bond, Melt-Blown and Other Processes), by Material Type (Polyethylene, Polypropylene, Polyester, and Other Materials), and by Region (North America [The USA, Canada, and Mexico], Europe [Germany, France, The UK, Russia, and Rest of Europe], Asia-Pacific [China, Japan, India, and Rest of Asia- Pacific], and Rest of the World [Brazil, Saudi Arabia, and Others]).

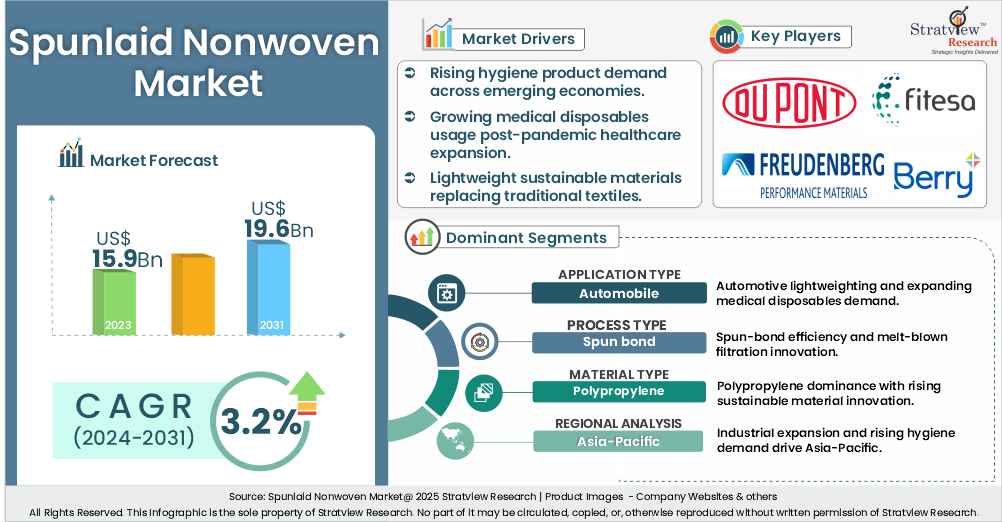

“The spunlaid nonwoven market value was USD 15.9 billion in 2023 and is likely to grow at a CAGR of 3.2% in the long run to reach USD 19.6 billion in 2031.”

Want to know more about the market scope? Register Here

The spunlaid nonwoven market is emerging as a dynamic market within the textile and material industry, recognized for its efficiency and adaptability. Produced by melting thermoplastic polymers like polypropylene and polyester, the fibers are extruded and spun into continuous filaments, then laid directly onto a conveyor to form a fabric web. This web is bonded through thermal, chemical, or mechanical methods, creating strong and uniform materials. Its unique properties make spunlaid nonwovens essential for applications in hygiene, medical textiles, packaging, geotextiles, automotive, building, filtration, and food & beverage industries.

One of the major factors driving this market is its exceptional versatility across industries. In hygiene, spunlaid nonwovens are widely used in diapers, sanitary napkins, and wipes due to their softness, strength, and absorbency. The medical industry also relies heavily on these fabrics for masks, gowns, and disposable products that ensure safety and comfort. Additionally, their durability and adaptability make them vital for geotextiles, automotive interiors, and construction projects, where performance, longevity, and cost efficiency are critical. This cross-industry adoption continues to strengthen demand globally.

The market’s growth is further supported by evolving consumer preferences and technological innovation. Rising demand for sustainable, eco-friendly, and lightweight materials has accelerated the adoption of spunlaid nonwovens in packaging, filtration, and roofing applications. Advances in production processes now enable higher efficiency and improved fabric properties, making them more competitive than traditional textiles. As industries seek solutions that balance cost, performance, and environmental impact, spunlaid nonwovens are positioned as the preferred choice, driving sustained global expansion across a wide spectrum of applications.

Innovations in the spunlaid nonwoven market are reshaping its role across industries, with manufacturers focusing on advanced materials, eco-friendly solutions, and enhanced performance features. Product development emphasizes biodegradable and recyclable nonwovens to meet rising sustainability goals, while high-strength, lightweight fabrics are being engineered for automotive, geotextile, and filtration applications. Smart nonwovens integrated with antimicrobial and moisture-management properties are gaining traction in hygiene and medical industries. Additionally, automation, precision extrusion, and digital quality-control systems are improving production efficiency, consistency, and cost-effectiveness, positioning spunlaid fabrics as the backbone of next-generation nonwoven solutions.

|

Segmentations |

List of Sub-Segments |

Segments with High-Growth Opportunity |

|

Application-Type Analysis |

Hygiene, Automobile, Geotextile, Filtration, Medical, Building Roofing & Flooring, Foods & Beverages, and Other Applications. |

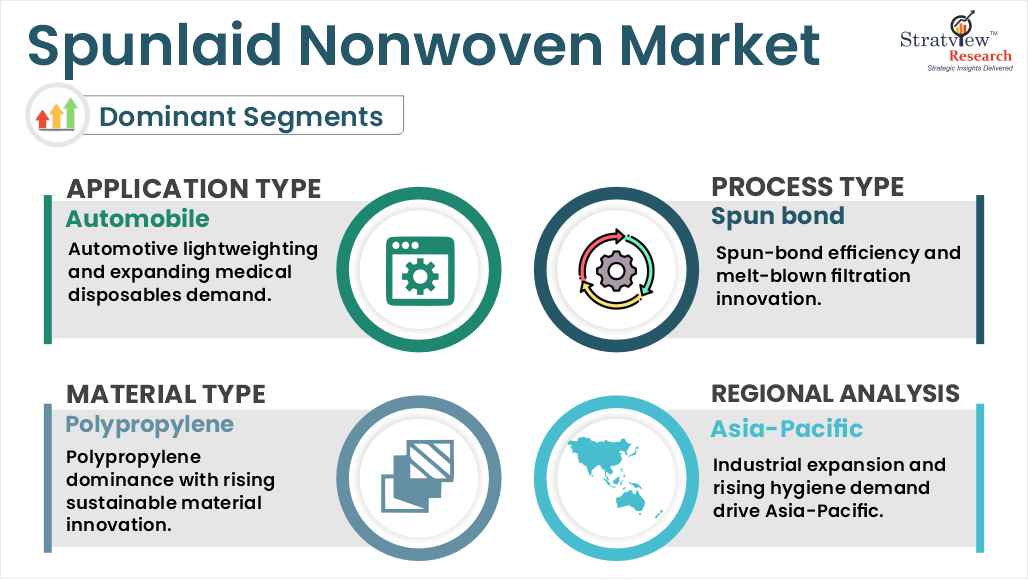

The automobile category is expected to dominate the spunlaid nonwoven market, driven by its rising demand for lightweight, durable, and cost-efficient materials that enhance vehicle performance, safety, and fuel efficiency. |

|

Process-Type Analysis |

Spun-bond, Melt-blown, and Other Processes. |

Spun bond process is expected to be the most preferred process type of the spunlaid nonwoven market, owing to its cost-efficiency, high production speed, superior fabric uniformity, and wide applicability across hygiene, medical, automotive, and geotextile industries. |

|

Material-Type Analysis |

Polyethylene, Polypropylene, Polyester, and Other Materials. |

Polypropylene is anticipated to hold the largest market share in the spunlaid nonwoven market due to its lightweight nature, cost-effectiveness, durability, versatility, and widespread adoption across hygiene, medical, and packaging applications. |

|

Region Analysis |

North America, Europe, Asia-Pacific, and The Rest of the World |

Asia-Pacific is expected to experience the fastest growth over the forecast period. |

“The automobile category is expected to be the widely used application, while the medical category is expected to be the fastest-growing application of the spunlaid market during the forecast period.”

Based on application type, the market is segmented into hygiene, automobile, geotextile, filtration, medical, building roofing & flooring, foods & beverages, and other applications. The automobile is likely to hold the largest share of the spunlaid nonwoven market, driven by its extensive use in vehicle interiors, insulation, carpets, and cabin air filtration. Automakers prefer spunlaid nonwovens for their durability, lightweight properties, and cost-effectiveness, which contribute to improved fuel efficiency and performance. Additionally, growing demand for electric and hybrid vehicles further boosts the adoption of advanced nonwoven materials for noise reduction, thermal management, and design flexibility. This strong reliance on spunlaid fabrics positions the automobile industry as the dominant application area in the market.

On the other hand, the medical category is projected to experience the fastest growth, fueled by rising healthcare needs, increasing surgical procedures, and heightened infection control standards post-pandemic. Spunlaid nonwovens are widely used in surgical gowns, drapes, masks, and sterilization wraps due to their breathability, barrier protection, and cost efficiency. Continuous innovation in antimicrobial and biodegradable fabrics further supports demand, while expanding healthcare infrastructure in emerging economies accelerates adoption. Together, these factors make the medical industry the leading growth driver in the forecast period.

“Spun-bond leads with efficiency and versatility, while melt-blown processes accelerate growth through advanced filtration, specialized applications, and rising demand in the spunlaid nonwoven market.”

Based on process type, the market is segmented into spun-bond and melt-blown & other processes. Spun-bond technology holds the largest share of the spunlaid nonwoven market, driven by its cost-effectiveness, high production efficiency, and ability to create strong, lightweight, and durable fabrics. Widely used across industries such as hygiene, automotive, packaging, and geotextiles, spun-bond nonwovens provide versatility and scalability, making them the preferred choice for high-volume production. Their uniformity, coupled with excellent mechanical properties, ensures consistent quality across applications. The rising global demand for sustainable and affordable nonwoven solutions further strengthens the dominance of spun-bond processes in the spunlaid nonwoven market.

In contrast, melt-blown and other processes are expected to record the fastest growth during the forecast period, propelled by their superior filtration efficiency and ability to produce ultra-fine fibers. This process gained significant momentum during the COVID-19 pandemic for use in medical masks, respirators, and filtration systems, highlighting its critical role in healthcare and environmental applications. As industries prioritize high-performance, value-added materials, melt-blown technology continues to gain traction. Its ability to support specialized applications like medical textiles, air filtration, and protective clothing positions this segment as a key driver of innovation and rapid market expansion.

Want to have a closer look at this market report? Click Here

“Polypropylene secures market leadership with versatility and cost-effectiveness, while polyethylene, polyester, and emerging sustainable materials drive specialized applications and future growth in the spunlaid nonwoven market.”

Based on material type, the market is segmented into polyethylene, polypropylene, polyester, and other materials. Polypropylene holds the largest share in the spunlaid nonwoven market due to its superior versatility, cost-effectiveness, and performance. Its lightweight structure, durability, and excellent chemical resistance make it highly suitable across diverse industries, including hygiene, medical, automotive, and packaging. With increasing demand for disposable hygiene products, polypropylene-based nonwovens remain the preferred material. The material’s ability to deliver strength, softness, and absorbency at a competitive cost drives widespread adoption, while regulatory compliance and sustainability advancements further strengthen its dominance across global markets.

While polypropylene dominates, materials like polyethylene and polyester are also gaining momentum in niche applications. Polyethylene offers flexibility and softness, making it favorable in hygiene and medical uses, while polyester provides enhanced durability for geotextiles, roofing, and automotive industries. Growing innovation in blended materials and the development of biodegradable and recyclable alternatives are fueling opportunities for eco-friendly applications. Rising environmental awareness, coupled with demand for sustainable nonwoven solutions, is pushing manufacturers to diversify material choices, ensuring future growth across multiple industries within the spunlaid nonwoven market.

“Asia-Pacific leads the spunlaid nonwoven market with an expanding industrial base, rising hygiene demand, and rapid growth across healthcare, automotive, and construction industries, driving future global dominance.”

Asia-Pacific secures the largest share of the spunlaid nonwoven market, supported by its rapidly expanding industrial base, population growth, and rising disposable incomes. The region’s dominance is strongly influenced by the increasing consumption of hygiene products, automotive applications, and healthcare textiles, particularly in countries like China, India, and Southeast Asian nations. Expanding infrastructure, a strong presence of local manufacturers, and competitive production costs further enhance the region’s leadership. With robust supply chains and high demand across multiple industries, Asia-Pacific remains the central hub driving global market momentum.

Asia-Pacific is not only the largest but also the fastest-growing region in the spunlaid nonwoven market. This growth is fueled by urbanization, greater health awareness, and rising adoption of hygiene and medical products post-pandemic. Government initiatives supporting healthcare infrastructure, along with technological advancements in nonwoven production, further strengthen regional growth prospects. The booming automotive and construction industries add to the demand, while the affordability of spunlaid fabrics ensures widespread adoption. With strong domestic consumption and expanding exports, the Asia-Pacific is set to reinforce its market leadership in the forecast period.

The market is fragmented, with more than 200 players. Most of the major players compete in some of the governing factors, including price, product offerings, and regional presence, etc. The following are the key players in the spunlaid nonwoven market. Some of the major players provide a complete range of products:

Here is the list of the Top Players (Based on Dominance)

Note: The above list does not necessarily include all the top players in the market.

Are you the leading player in this market? We would love to include your name. Please write to us at [email protected]

This strategic assessment report, from Stratview Research, provides a comprehensive analysis that reflects today’s spunlaid nonwoven market realities and future market possibilities for the forecast period of 2024 to 2031. After a continuous interest in our spunlaid nonwoven market report from the industry stakeholders, we have tried to further accentuate our research scope to the spunlaid nonwoven market to provide the most crystal-clear picture of the market. The report segments and analyses the market in the most detailed manner to provide a panoramic view of the market. The vital data/information provided in the report can play a crucial role for the market participants as well as investors in the identification of the low-hanging fruits available in the market as well as to formulate the growth strategies to expedite their growth process.

This report offers high-quality insights and is the outcome of a detailed research methodology comprising extensive secondary research, rigorous primary interviews with industry stakeholders, and validation and triangulation with Stratview Research’s internal database and statistical tools. More than 1000 authenticated secondary sources, such as company annual reports, fact books, press releases, journals, investor presentations, white papers, patents, and articles, have been leveraged to gather the data. We conducted more than 15 detailed primary interviews with the market players across the value chain in all four regions and industry experts to obtain both qualitative and quantitative insights.

This report provides market intelligence most comprehensively. The report structure has been kept so that it offers maximum business value. It provides critical insights into market dynamics and will enable strategic decision-making for existing market players as well as those willing to enter the market. The following are the key features of the report:

The spunlaid nonwoven market is segmented into the following categories.

Spunlaid Nonwoven Market, by Application Type

Spunlaid Nonwoven Market, by Process Type

Spunlaid Nonwoven Market, by Material Type

Spunlaid Nonwoven Market by Region

With this detailed report, Stratview Research offers one of the following free customization options to our respected clients:

Company Profiling

Competitive Benchmarking

Custom Research: Stratview Research offers custom research services across industries. In case of any custom research requirement related to market assessment, competitive benchmarking, sourcing and procurement, target screening, and others, please send your inquiry to [email protected].

The report is delivered digitally through our online portal. Buyers receive login credentials from our team to access the report and may update their credentials at any time after the initial login.

Delivery timelines depend on the status of the report:

For the most accurate delivery timeline, please contact us to confirm the current status of the report.

Yes. You may request a complimentary preview of the report through a video conference with our team.

Yes. The scope of the report can be fully customized to align with your specific research objectives and information requirements.

Please contact us at [email protected], and our team will be happy to discuss your requirements and propose a tailored solution.

Yes. Selected sections of the report can be purchased separately based on your requirements. Please contact us at [email protected] to discuss your needs.

Yes, AI can help gather publicly available information, but its outputs are only as reliable as the data it accesses. Stratview Research reports are built using validated data, extensive primary interviews with industry stakeholders, and the expertise of our experienced research team.

Additionally, many critical insights, including market dynamics, competitive intelligence, and industry-specific trends, are not publicly available and therefore cannot be captured through AI alone.

Spunlaid nonwovens are fabrics produced by melting thermoplastic polymers, extruding them into continuous filaments, and directly laying them into webs, bonded through thermal, chemical, or mechanical processes for versatile applications.

The forecasted value of the spunlaid nonwoven market is projected to reach US$19.6 billion by 2031, driven by rising demand across hygiene, medical, automotive, and construction applications.

The spunlaid nonwoven market is estimated to grow at a CAGR of 3.2% by 2031, due to steady demand for hygiene products, medical applications, and advancements in production technologies. Growing eco-friendly trends and expanding applications in packaging and geotextiles also support this moderate growth.

The Asia-Pacific region records the highest market growth in the spunlaid nonwoven market, driven by rapid industrialization, rising hygiene product demand, expanding automotive industry, and increasing healthcare infrastructure investments.

Berry Global, Freudenberg Performance Materials, Fitesa S.A., DuPont de Nemours, Inc., Hollingsworth & Vose, John Manville, Sandler’s Corp., Avgol America Inc., Gulsan Group, and Ahlstrom are the leading players of the spunlaid nonwoven market.

The leading segment by application type in the spunlaid nonwoven market is automobile, driven by high demand for lightweight, durable, and cost-effective materials that enhance performance, safety, and fuel efficiency.

WE ACCEPT