404

+1-313-307-4176

Data Center GPU Market Analysis | 2026-2034

Data Center GPU Market Size, Share, Trends, Dynamics, Forecast, & Growth Analysis: 2026-2034

"Data center GPU market size was USD 55.71 billion in 2025.”

Want to know more about the market scope? Register Here

Have a look at the sales opportunities presented by the data center GPU market in terms of growth and market forecast.

|

Data Center GPU Market Data & Statistics |

||

|

Market Statistics |

Value (in USD Billion) |

Market Growth (%) |

|

Annual Market Size in 2024 |

USD 86.53 billion |

- |

|

Annual Market Size in 2025 |

USD 98.90 billion |

YoY Growth in 2025: 14.30% |

|

Annual Market Size in 2026 |

USD 112.85 billion |

YoY Growth in 2026: 14.10% |

|

Annual Market Size in 2034 |

USD 304.26 billion |

CAGR 2026-2034: 13.20% |

|

Cumulative Sales Opportunity during 2026-2034 |

USD 1768.58 billion |

- |

|

Top 10 Countries’ Market Share in 2025 |

USD 79.12 billion + |

> 80% |

|

Top 10 Company’s Market Share in 2025 |

USD 49.45 billion to USD 69.23 billion |

50% - 70% |

Growth in AI and Machine Learning Workloads

Expansion of Cloud and Hyperscale GPU Infrastructure

Hyperscale cloud providers are investing heavily in GPU clusters to support on-demand computing workloads for enterprises. By offering GPU-as-a-Service, they enable access to high-performance computing without high upfront costs. In 2025, cloud operators accounted for more than 50% of global GPU usage, highlighting the pivotal role of cloud infrastructure in GPU adoption and distribution worldwide.

Increasing High-Performance Computing and Data Analytics Needs

GPUs are increasingly deployed for high-performance computing (HPC) tasks, including scientific simulations, big data analytics, and real-time data processing. Their ability to handle complex workloads faster and more efficiently than CPUs makes them critical for industries such as genomics, climate modeling, and engineering research, reinforcing the need for GPU-equipped data centers worldwide.

High Power Consumption and Infrastructure Strain

GPU clusters draw significant power, creating a major operational challenge that can limit the adoption and scaling of GPU infrastructure in data centers. As GPUs increase in performance and density, electricity demand is rising rapidly, putting pressure on grid capacity and energy infrastructure. According to S&P Global, global data center power demand is projected to nearly double by 2030, stressing utilities and necessitating major upgrades to power delivery systems.

Expansion of GPU‑Ready Data Center Infrastructure in Asia‑Pacific

The Asia‑Pacific region is emerging as a key hub for GPU-equipped data centers, accounting for around 30 % of global data center capacity. Rapid expansion of hyperscale and enterprise cloud infrastructure is driving IT power requirements to nearly 90 GW by 2028, creating substantial opportunities for GPU hardware and services. Rising demand for AI, machine learning, and compute-intensive workloads further reinforces the need for advanced GPU solutions across the region.

|

Segmentations |

List of Sub-Segments |

Segments with High-Growth Opportunity |

|

Deployment Analysis |

Cloud and On-Premises |

Cloud segment is anticipated to maintain its dominance in the data center GPU market during the forecast period. |

|

Function Analysis |

Training and Inference |

Inference segment is expected to witness the highest growth rate in the coming years. |

|

Application Analysis |

Generative AI, Machine Learning, Natural Language Processing, and Computer Vision |

Generative AI segment is projected to be the fastest-growing segment during the forecast period. |

|

End-User Analysis |

Cloud Service Providers, Enterprises, and Government Organizations |

Cloud Service Providers segment is expected to grow at the highest rate during the forecast period. |

|

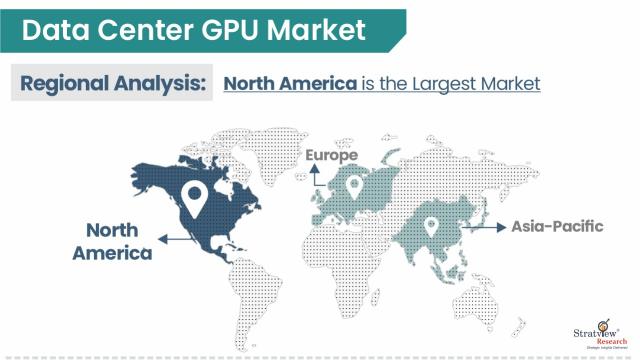

Regional Analysis |

North America, Europe, Asia-Pacific, and The Rest of the World |

North America is expected to be the dominant region over the forecasted period. |

"Cloud segment is projected to maintain dominance in the data center GPU market during the forecast period."

"Cloud service providers are expected to grow at the fastest rate during the forecast period."

"North America is expected to remain the dominant region over the forecasted period."

Know the high-growth countries in this report. Register Here

Most of the major players compete in some of the factors, including price, service offerings, regional presence, etc. The following are the key players in the data center GPU market:

Note: The above list does not necessarily include all the top players in the market.

Are you a leading player in this market? We would love to include your name. Please write to us at [email protected]

October 2025 – AMD Introduces Helios Rack‑Scale AI Platform

Advanced Micro Devices, Inc. (AMD) unveiled its Helios rack‑scale AI hardware platform at the OCP Global Summit 2025, designed for rack‑scale GPU deployments with significantly higher memory capacity and performance, with Oracle set to deploy thousands of MI450 GPUs starting in 2026.

September 2025 – NVIDIA and Intel Strategic Technology Collaboration

NVIDIA Corporation announced a $5 billion investment in Intel Corporation, along with collaboration to integrate NVIDIA’s GPU technology with Intel’s CPU hardware, signaling a major joint effort to develop hybrid GPU‑CPU data center systems optimized for AI workloads.

March 2025 – NVIDIA Unveils Next‑Generation AI Infrastructure Platform

At GTC 2025, NVIDIA Corporation announced a new AI Data Platform and next‑generation GPU roadmap, featuring enhanced enterprise infrastructure designs that integrate accelerated computing and networking for demanding AI inference workloads. This positions NVIDIA at the center of data center AI infrastructure development.

This report provides market intelligence most comprehensively. The report structure has been kept so that it offers maximum business value. It provides critical insights into market dynamics and will enable strategic decision-making for existing market players as well as those willing to enter the market.

The following are the key features of the report:

|

Market Study Period |

2019-2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Trend Period |

2019-2024 |

|

Number of Tables & Figures |

>100 |

|

Number of Segments Analysed |

5 (Function Type, Application Type, End-User Type, Deployment Type, and Region) |

|

Number of Regions Analysed |

4 (North America, Europe, Asia-Pacific, Rest of the World) |

|

Countries Analysed |

15 (The USA, Canada, Mexico, Germany, France, Italy, The UK, China, Japan, India, Brazil, Saudi Arabia, Rest of Europe, Rest of APAC, and Rest of the World) |

|

Free Customization Offered |

10% |

|

After Sales Support |

Unlimited |

|

Report Presentation |

Complimentary |

|

Market Dataset |

Complimentary |

|

Further Deep Dive & Consulting Services |

10% Discount |

The report provides detailed insights into the market dynamics to enable informed business decision-making and growth strategy formulation based on the opportunities present in the market.

The data center GPU market is segmented into the following categories:

By Deployment Type

By Function Type

By End-User Type

By Application Type

By Region

With this detailed report, Stratview Research offers one of the following free customization options to our respected clients:

Company Profiling

Detailed profiling of additional market players (up to three players)

SWOT analysis of key players (up to three players)

Competitive Benchmarking

Benchmarking of key players on the following parameters: Service portfolio, geographical reach, regional presence, and strategic alliances.

Custom Research: Stratview Research offers custom research services across industries. In case of any custom research requirement related to market assessment, competitive benchmarking, sourcing and procurement, target screening, and others, please send your inquiry to [email protected].

The report is delivered digitally through our online portal. Buyers receive login credentials from our team to access the report and may update their credentials at any time after the initial login.

Delivery timelines depend on the status of the report:

For the most accurate delivery timeline, please contact us to confirm the current status of the report.

Yes. You may request a complimentary preview of the report through a video conference with our team.

Yes. The scope of the report can be fully customized to align with your specific research objectives and information requirements.

Please contact us at [email protected], and our team will be happy to discuss your requirements and propose a tailored solution.

Yes. Selected sections of the report can be purchased separately based on your requirements. Please contact us at [email protected] to discuss your needs.

Yes, AI can help gather publicly available information, but its outputs are only as reliable as the data it accesses. Stratview Research reports are built using validated data, extensive primary interviews with industry stakeholders, and the expertise of our experienced research team.

Additionally, many critical insights, including market dynamics, competitive intelligence, and industry-specific trends, are not publicly available and therefore cannot be captured through AI alone.

The data center GPU market refers to the global industry involved in the design, manufacturing, and deployment of high-performance graphics processing units specifically for data centers. These GPUs are engineered to handle computationally intensive workloads, including AI training and inference, high-performance computing (HPC), big data analytics, and scientific simulations.

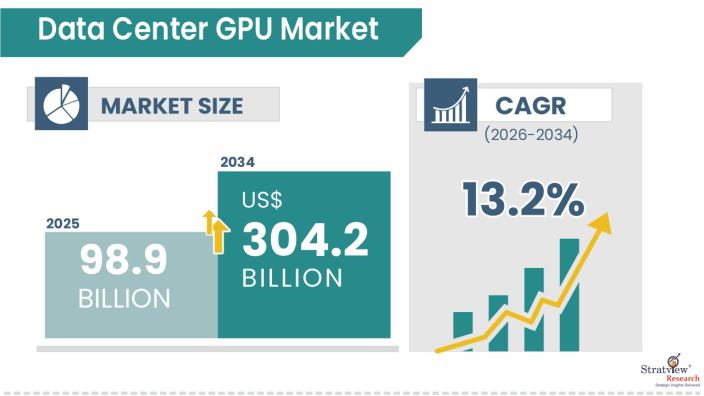

As of 2025, the data center GPU market is valued at USD 98.90 billion, up from USD 86.53 billion in 2024, reflecting a YoY growth of 14.30%. The growth is fueled by increasing adoption of AI workloads, expansion of cloud and hyperscale infrastructure, and rising HPC demands across multiple sectors.

The market is projected to reach USD 112.85 billion in 2026 and grow further to USD 304.26 billion by 2034, driven by ongoing investments in AI, machine learning, cloud computing, and GPU-equipped data centers.

During the forecast period from 2026 to 2034, the global data center GPU market is expected to grow at a compound annual growth rate (CAGR) of 13.20%, supported by expanding cloud adoption, AI deployment, and the increasing need for high-performance computing solutions.

• AI and Machine Learning: Over 60% of GPU usage in 2025 supported AI workloads across North America, Europe, and Asia-Pacific. • Cloud & Hyperscale Infrastructure: Cloud operators accounted for more than 50% of global GPU usage in 2025. • High-Performance Computing: GPUs accelerate complex simulations, big data analytics, and real-time processing.

The key end-users include cloud service providers, enterprises, and government organizations. Cloud service providers such as AWS, Microsoft Azure, and Google Cloud are deploying GPU-accelerated platforms to support AI, HPC, and big data workloads. Enterprises and research institutions increasingly rely on GPU-powered data centers to enhance computational efficiency and reduce processing times.

The top players in the data center GPU market include • NVIDIA Corporation • Intel Corporation • Advanced Micro Devices, Inc. • Micron Technology, Inc. • IBM

North America is expected to be the dominant region over the forecasted period, due to its strong presence of leading cloud service providers, advanced technological infrastructure, and early adoption of AI and machine learning.

WE ACCEPT