404

+1-313-307-4176

Data Center Networking Market Analysis | 2025-2032

Data Center Networking Market Size, Share, Trends, Dynamics, Forecast, & Growth Analysis: 2025-2032

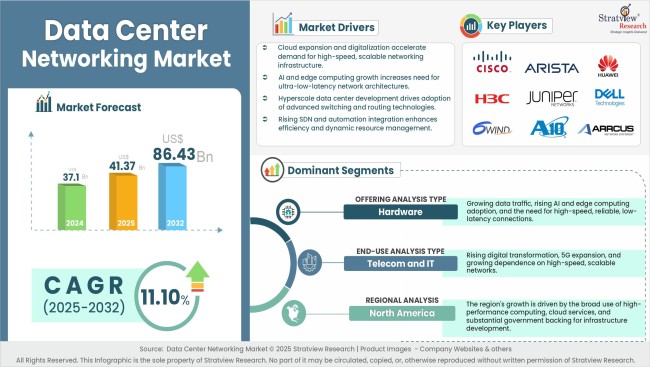

"Data Center Networking Market size was USD 37.1 billion in 2024.”

Want to get a free sample? Register Here

Have a look at the sales opportunities presented by the data center networking market in terms of growth and market forecast.

Data Center Networking Market Data & Statistics

|

Market Statistics |

Value (in USD Billion) |

Market Growth (%) |

|

Annual Market Size in 2023 |

USD 34.32 billion |

|

|

Annual Market Size in 2024 |

USD 37.1 billion |

YoY Growth in 2024: 8.1% |

|

Annual Market Size in 2025 |

USD 41.37 billion |

YoY Growth in 2025: 11.5% |

|

Annual Market Size in 2032 |

USD 86.43 billion |

CAGR 2025-2032: 11.10% |

|

Cumulative Sales Opportunity during 2025-2032 |

USD 493.90 billion |

|

|

Top 10 Countries’ Market Share in 2024 |

USD 29.68 billion + |

> 80% |

|

Top 10 Company’s Market Share in 2024 |

USD 18.55 billion to USD 25.97 billion |

50% - 70% |

The data center networking market is witnessing rapid growth, driven by the expansion of AI workloads, increasing deployment of hyperscale data centers, and the growing adoption of 5G and edge computing. Rising global digital connectivity is further accelerating investments in high-speed networking infrastructure, while the growing focus on energy-efficient and sustainable networking technologies is emerging as a key trend shaping the market's long-term growth.

AI-Driven Growth in Data Center Capacity is Accelerating Market Growth

The rapid expansion of AI workloads is accelerating the growth of the data center networking market. Increasing deployment of GPU clusters, AI training infrastructure, and hyperscale data centers is driving demand for high-speed Ethernet, optical interconnects, and advanced networking solutions.

Expansion of 5G and Edge Computing is Expanding Market Share

The expansion of 5G networks and edge computing is expanding the market share of the data center networking market. Growing deployment of distributed data centers is increasing demand for low-latency switching, routing, and edge networking infrastructure.

Rising Global Digital Connectivity is Driving Market Demand

Rising global digital connectivity is driving demand in the data center networking market. Increasing internet penetration and digital transformation initiatives are generating higher data traffic, encouraging investments in scalable and high-capacity networking infrastructure.

Increasing Energy Demand Restrains Market Growth

The increasing energy demand of AI-enabled data centers is restraining the growth of the data center networking market. Rising electricity requirements for computing and cooling are increasing operating costs while placing greater pressure on power infrastructure.

Growing Cybersecurity Threats Challenge Market Demand

Growing cybersecurity threats are challenging demand in the data center networking market. Increasing network complexity is exposing data center infrastructure to ransomware, distributed denial-of-service (DDoS), and supply chain attacks, requiring greater investments in network security.

Workforce and Skills Gap Challenges Market Growth

The shortage of skilled networking and cybersecurity professionals is challenging the growth of the data center networking market. Managing AI-enabled and software-defined networks requires specialized expertise, creating workforce constraints across the industry.

Growing Demand for Energy-Efficient Networking Solutions is Emerging as a Key Market Trend

The growing demand for energy-efficient networking solutions is emerging as a key trend in the data center networking market. Organizations are increasingly investing in energy-efficient switches, optical networking technologies, and intelligent traffic management systems to improve operational efficiency and reduce power consumption.

Sustainable Data Center Development Strengthens Market Forecast

The growing focus on sustainable data center development is strengthening the market forecast for the data center networking market. Increasing integration of renewable energy and energy-efficient digital infrastructure is creating long-term opportunities for sustainable networking technologies.

Digitalization Across Emerging Economies is Creating New Market Opportunities

The rapid digitalization of emerging economies is creating new opportunities in the data center networking market. Expanding internet connectivity and digital infrastructure investments are driving demand for new data center construction and networking upgrades.

|

Segmentations |

List of Sub-Segments |

Segments with High-Growth Opportunity |

|

Offering Type Analysis |

Hardware, Software, and Other Services |

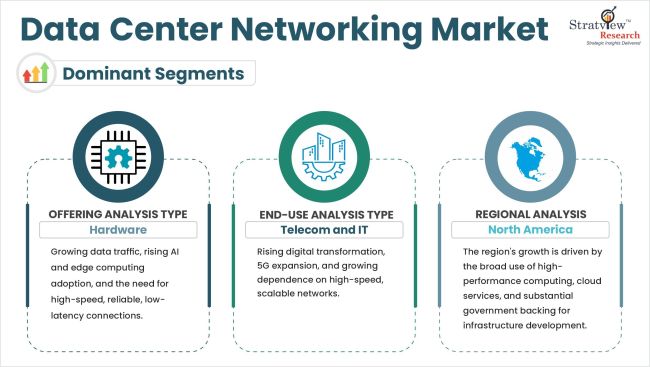

Hardware segment is projected to be the dominant segment during the forecast period. |

|

End-Use Type Analysis |

Enterprises, Telecom Service Providers, Cloud Service Providers, and Telecom and IT services |

Telecom and IT segment is expected to be the dominant during the forecast period. |

|

Regional Analysis |

North America, Europe, Asia-Pacific, and The Rest of the World |

North America is expected to be the dominant and fastest-growing region over the forecasted period. |

“Hardware segment is projected to be the dominant segment during the forecast period.”

Want to get a free sample? Register Here

"The IT & Telecom segment is expected to be the dominant segment during the forecast period.”

“North America is expected to be the dominant and the fastest-growing region over the forecasted period.”

Most of the major players compete in some of the factors, including price, service offerings, regional presence, etc. The following are the key players in the data center networking market:

Note: The above list does not necessarily include all the top players in the market.

Are you a leading player in this market? We would love to include your name. Please write to us at [email protected]

This report provides market intelligence most comprehensively. The report structure has been kept so that it offers maximum business value. It provides critical insights into market dynamics and will enable strategic decision-making for existing market players as well as those willing to enter the market.

The following are the key features of the report:

|

Market Study Period |

2019-2032 |

|

Base Year |

2024 |

|

Forecast Period |

2025-2032 |

|

Trend Period |

2019-2023 |

|

Number of Tables & Figures |

>100 |

|

Number of Segments Analysed |

3 (Offering Type, End-Use Industry Type, and Region) |

|

Number of Regions Analysed |

4 (North America, Europe, Asia-Pacific, Rest of the World) |

|

Countries Analysed |

15 (The USA, Canada, Mexico, Germany, France, Italy, The UK, China, Japan, India, Brazil, Saudi Arabia, Rest of Europe, Rest of APAC, and Rest of the World) |

|

Free Customization Offered |

10% |

|

After Sales Support |

Unlimited |

|

Report Presentation |

Complimentary |

|

Market Dataset |

Complimentary |

|

Further Deep Dive & Consulting Services |

10% Discount |

This report studies the market, covering a period of 15 years of trend and forecast. The report provides detailed insights into the market dynamics to enable informed business decision-making and growth strategy formulation based on the opportunities present in the market.

The data center networking market is segmented into the following categories:

By Offering Type

By End User Type

By Region

With this detailed report, Stratview Research offers one of the following free customization options to our respected clients:

Company Profiling

Competitive Benchmarking

Custom Research: Stratview Research offers custom research services across industries. In case of any custom research requirement related to market assessment, competitive benchmarking, sourcing and procurement, target screening, and others, please send your inquiry to [email protected].

The report is delivered digitally through our online portal. Buyers receive login credentials from our team to access the report and may update their credentials at any time after the initial login.

Delivery timelines depend on the status of the report:

For the most accurate delivery timeline, please contact us to confirm the current status of the report.

Yes. You may request a complimentary preview of the report through a video conference with our team.

Yes. The scope of the report can be fully customized to align with your specific research objectives and information requirements.

Please contact us at [email protected], and our team will be happy to discuss your requirements and propose a tailored solution.

Yes. Selected sections of the report can be purchased separately based on your requirements. Please contact us at [email protected] to discuss your needs.

Yes, AI can help gather publicly available information, but its outputs are only as reliable as the data it accesses. Stratview Research reports are built using validated data, extensive primary interviews with industry stakeholders, and the expertise of our experienced research team.

Additionally, many critical insights, including market dynamics, competitive intelligence, and industry-specific trends, are not publicly available and therefore cannot be captured through AI alone.

The data center networking is crucial for global business and industry digital transformation. As the demand for high-speed data transfer, efficient cloud services, and seamless connection develops, data centers adapt to satisfy these needs. This industry includes a wide range of technologies and components, such as networking hardware, software, and solutions aimed at improving data center performance, security, and scalability.

The forecasted value for the market is US$ 86.43 billion in 2032.

Data center networking market size was USD 37.1 billion in 2024 and is expected to grow from USD 41.37 billion in 2025 to USD 86.43 billion in 2032, witnessing an impressive market growth (CAGR) of 11.10% during the forecast period (2025-2032).

The key drivers of the data center networking market include increasing data traffic and bandwidth, which boost the adoption of data center networking components.

The top players in the data center networking market include • 6WIND (France) • A10 (US) • Alcatel-Lucent Enterprise (France) • Arista Networks (US) • Arrcus (US) • Cisco (US) • Dell (US) • Edgecore Networks (Taiwan) • Extreme Networks (US) • F5 (US) • H3C (China) • HPE (US) • Huawei (China) • Intel (US) • Juniper Networks (US) • Kaloom Networks (Canada) • Larch Networks (Israel)

North America is expected to be the dominant and the fastest-growing region of the data center networking market over the forecasted period, due to the increased adoption of high-performance computing and cloud services.

WE ACCEPT