404

+1-313-307-4176

Aerospace Adhesives and Sealants Market Analysis | 2026-2032

Aerospace Adhesives and Sealants Market Size, Share, Trends, Dynamics, Forecast, & Growth Analysis: 2026-2032

Aerospace Adhesives and Sealants Market is segmented by Type (Adhesives and Sealants), by Resin Type (Epoxy, Silicone, Polyurethane, and Others), by Technology Type (Solvent-Based, Water-Based, and Others), by User Type (OEM and MRO), by End-Use Industry Type (Commercial, Military, and General Aviation), and by Region (North America [The USA, Canada, and Mexico], Europe [Germany, France, The UK, Russia, and Rest of Europe], Asia-Pacific [China, Japan, South Korea, India, and Rest of Asia-Pacific], and Rest of the World [Brazil, Saudi Arabia, and Others]).

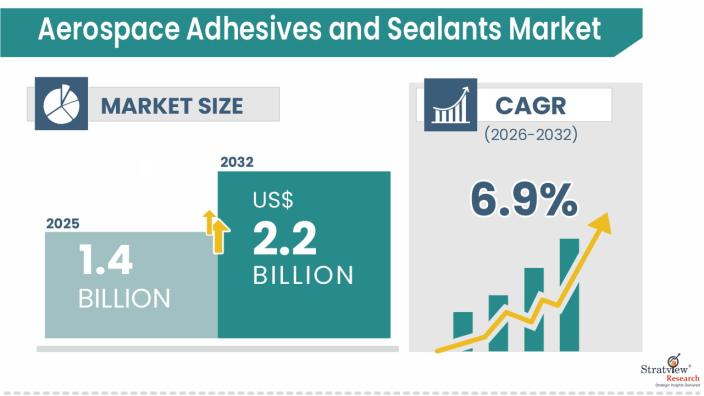

The aerospace adhesives and sealants market was estimated at USD 1.4 billion in 2025 and is likely to grow at a CAGR of 6.9% during 2026-2032 to reach USD 2.2 billion in 2032.

Want to know more about the market scope? Register Here

Market Dynamics

The aerospace adhesives and sealants market analysis indicates growing demand across commercial aviation, defense, and space applications due to the increasing use of lightweight composite structures and fuel-efficient aircraft technologies. The aerospace adhesives and sealants market forecast further highlights rising adoption of high-performance, low-VOC, and durable bonding solutions driven by next-generation aircraft manufacturing and sustainability initiatives.

Market drivers

Growing Aerospace & Defense Demand for Lightweight Materials

The advanced composite market growth is supported by increasing demand for lightweight, fuel-efficient, and high-performance materials across commercial aviation and defense applications. Advanced composites are widely used in aircraft structures, engine components, radomes, and military systems due to their high strength-to-weight ratio, corrosion resistance, and durability advantages.

Expansion of Wind Energy Installations

The advanced composite market demand is increasing due to the growing adoption of lightweight and high-strength materials in wind energy infrastructure. Wind turbine manufacturers are increasingly utilizing advanced composites in blade manufacturing to improve durability, reduce structural weight, and enhance overall power generation efficiency, particularly in large-scale offshore wind projects.

The increasing deployment of next-generation offshore wind turbines with longer blade structures is accelerating advanced composite market demand for carbon-fiber and glass-fiber materials, as manufacturers focus on improving turbine efficiency, operational lifespan, and energy output in harsh marine environments.

Increasing Adoption in Automotive Lightweighting

The advanced composite market demand is growing steadily due to the rising integration of lightweight materials in electric vehicles (EVs) and high-performance automotive applications. Automakers are increasingly adopting advanced composites to reduce vehicle weight, improve battery efficiency, extend driving range, and comply with stringent emission reduction regulations.

As per Dipesh, the global advanced composites industry is undergoing rapid technological transformation. While conducting the market analysis and interacting with leading industry participants, it is evident that the next decade will be shaped by trends such as lightweight aerospace structures, recyclable composite materials, and increasing adoption of advanced composites in electric vehicles and renewable energy applications.

Market Challenge

Complex Recycling and End-of-Life Management

The advanced composites market growth is challenged by the complex recycling process associated with thermoset composite materials. Limited recycling infrastructure and increasing regulatory focus on sustainable material disposal continue to create environmental and operational concerns across composite manufacturing industries.

High Raw Material and Manufacturing Costs

The advanced composites market growth is hindered by the high cost of carbon fibers, advanced resins, and specialized manufacturing technologies compared to conventional materials. Limited production capacity, energy-intensive processing, and expensive tooling continue to restrict broader adoption across price-sensitive industries.

Market Opportunity

Emerging Advanced Air Mobility (eVTOL) and Urban Aviation

The advanced composite market demand is increasing with the rapid development of electric vertical takeoff and landing (eVTOL) aircraft and urban air mobility platforms. eVTOL manufacturers are increasingly utilizing lightweight composite airframes and structural components to improve aircraft range, battery efficiency, payload capacity, and aerodynamic performance.

In 2025, Archer Aviation accelerated production and FAA certification activities for its “Midnight” eVTOL aircraft, with the company targeting commercial deployment for urban air mobility applications. The growing development of lightweight eVTOL aircraft is increasing advanced composite market demand for high-strength carbon-fiber composite structures and aerospace-grade materials.

Joby Aviation continued expanding FAA certification and manufacturing activities for its S4 eVTOL aircraft platform in 2025 and 2026, while also scaling production capabilities for commercial air taxi operations. The increasing commercialization of next generation eVTOL aircraft is expected to strengthen advanced composite market demand across advanced air mobility applications.

Development of Recyclable and Sustainable Composite Materials

The advanced composite market demand is increasing as manufacturers invest in recyclable thermoplastic composites and bio-based resin systems to address sustainability concerns and comply with evolving environmental regulations. The growing focus on circular economy initiatives and low-emission material technologies is accelerating innovation in sustainable composite manufacturing.

In 2025, the European Union continued supporting composite recycling and circular material innovation projects under Horizon Europe programs, focusing on recyclable thermoplastic composites and sustainable fiber-recovery technologies for aerospace, automotive, and wind energy applications.

In 2025, Hexcel expanded commercialization of its HexPly M49 bio-derived epoxy prepreg materials, developed to reduce the carbon footprint of aerospace composite structures. Similarly, Syensqo advanced its CYCOM EP2190 thermoplastic composite technology for recyclable aerospace applications, supporting lightweight and sustainable aircraft manufacturing. These developments are strengthening advanced composite market demand for environmentally sustainable material solutions.

|

Segmentations |

List of Sub-Segments |

Dominant and Fastest-Growing Segments |

|

Resin-Type Analysis |

Epoxy, Silicone, Polyurethane, and Others |

Epoxy is anticipated to remain the biggest demand generator in the years to come. |

|

Technology Analysis |

Solvent-Based, Water-Based, and Others |

Water-based technology will be the largest segment in the forecasted period. |

|

User Type Analysis |

OEM and MRO |

The OEM user type is expected to dominate the market. |

|

End-Use Industry Analysis |

Commercial, Military, and General Aviation |

The commercial end-use industry is likely to hold the largest market share. |

|

Regional Analysis |

North America, Europe, Asia-Pacific, and The Rest of the World |

North America is expected to remain the largest market over the next five years. |

“Epoxy is expected to remain the dominant resin in the market during the forecast period.”

The aerospace adhesives and sealants market is segmented into epoxy, silicone, polyurethane, and others. Epoxy is expected to remain the dominant resin in the market during the forecast period due to its exceptional performance characteristics. Epoxy resins exhibit high strength, excellent adhesion properties, and outstanding resistance to temperature extremes, making them ideal for the demanding conditions experienced in aerospace environments.

These materials provide robust bonding and sealing capabilities, ensuring structural integrity and preventing the ingress of moisture or other contaminants that could compromise the safety and reliability of aircraft and spacecraft. Epoxy adhesives are also known for their versatility, as they can be tailored to specific aerospace requirements through formulations that offer varying levels of flexibility, toughness, and curing times.

“Water-based is expected to remain the dominant technology in the market during the forecast period.”

The market is segmented into Solvent-based, Water-based, and others. Water-based is expected to remain the dominant technology in the market due to environmental concerns and regulatory requirements, which have spurred a shift towards more sustainable and eco-friendly solutions in aerospace manufacturing.

Water-based adhesives and sealants are inherently less harmful to the environment compared to Solvent-Based counterparts, as they emit fewer volatile organic compounds (VOCs) and have a lower environmental impact. This aligns with the aerospace industry's commitment to reducing its carbon footprint and adhering to stringent environmental regulations.

Additionally, Water-Based adhesives and sealants exhibit excellent performance characteristics that meet the demanding requirements of the aerospace sector. They offer strong bonding and sealing capabilities, good adhesion to various substrates, and resistance to temperature extremes, ensuring the structural integrity and safety of aircraft and spacecraft.

“The commercial is expected to remain the largest end-use industry in the market during the forecast period.”

The market is segmented into commercial, military, and general aviation. The commercial is expected to remain the largest end-use industry in the market due to the sheer scale and diversity of commercial aviation compared to other segments of the aerospace industry.

Commercial aviation encompasses passenger and cargo aircraft, including a wide range of commercial airliners, regional jets, and even emerging markets like urban air mobility.

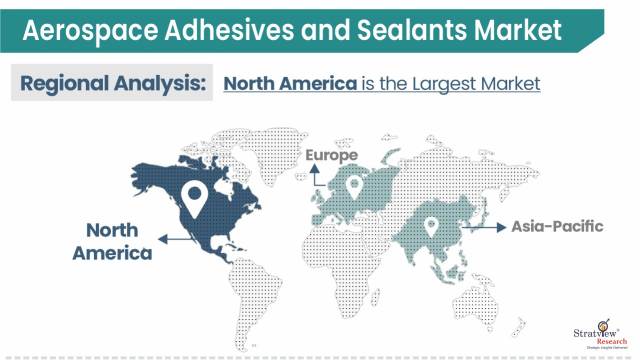

“North America is expected to remain the largest market, whereas Asia-Pacific is estimated to remain the fastest-growing market for aerospace adhesives & sealants in the foreseeable future.”

In terms of regions, North America is expected to remain the largest market for aerospace adhesives and sealants during the forecast period. Firstly, North America boasts a robust aerospace industry with a high concentration of major aerospace manufacturers, including Boeing and Airbus facilities, as well as numerous suppliers and aerospace research institutions.

This concentration of industry players results in a significant demand for high-quality adhesives and sealants. Secondly, North America places a strong emphasis on research and development in aerospace technology. This commitment to innovation drives the need for cutting-edge adhesive and sealant solutions that meet the stringent requirements of modern aircraft and spacecraft.

The Asia-Pacific is estimated to remain the fastest-growing market for aerospace adhesives & sealants in the foreseeable future. Firstly, APAC has emerged as a global hub for aerospace manufacturing, with countries like China, India, Japan, and South Korea investing significantly in their aerospace industries. Secondly, the APAC region benefits from a lower cost of production and labor, making it an attractive destination for aerospace manufacturing.

Know the high-growth countries in this report. Register Here

The following are the key players in the aerospace adhesives and sealants market (arranged alphabetically).

Note: The above list does not necessarily include all the top players in the market.

Are you the leading player in this market? We would love to include your name. Write to us at [email protected].

This report provides market intelligence in the most comprehensive way. The report structure has been kept such that it offers maximum business value. It provides critical insights into market dynamics and will enable strategic decision-making for existing market players as well as those willing to enter the market. The following are the key features of the report:

This report studies the market, covering a period of 12 years of trends and forecasts. The report provides detailed insights into the market dynamics to enable informed business decision-making and growth strategy formulation based on the opportunities present in the market.

The aerospace adhesives and sealants market is segmented into the following categories:

By Type

By Resin Type

By Technology Type

By User Type

By End-Use Industry Type

By Region

This strategic assessment report, from Stratview Research, provides a comprehensive analysis that reflects today’s aerospace adhesives and sealants market realities and future market possibilities for the forecast period of 2026 to 2032. After a continuous interest in our aerospace adhesives and sealants market report from the industry stakeholders, we have tried to further accentuate our research scope to the aerospace adhesives and sealants market to provide the most crystal-clear picture of the market. The report segments and analyses the market in the most detailed manner to provide a panoramic view of the market. The vital data/information provided in the report can play a crucial role for the market participants as well as investors in the identification of the low-hanging fruits available in the market as well as to formulate the growth strategies to expedite their growth process.

This report offers high-quality insights and is the outcome of a detailed research methodology comprising extensive secondary research, rigorous primary interviews with industry stakeholders, and validation and triangulation with Stratview Research’s internal database and statistical tools. More than 1000 authenticated secondary sources, such as company annual reports, fact books, press releases, journals, investor presentations, white papers, patents, and articles, have been leveraged to gather the data. We conducted more than 15 detailed primary interviews with the market players across the value chain in all four regions and industry experts to obtain both qualitative and quantitative insights.

With this detailed report, Stratview Research offers one of the following free customization options to our respectable clients:

Company Profiling

Competitive Benchmarking

Custom Research:

Stratview Research offers custom research services across sectors. In case of any custom research requirement related to market assessment, competitive benchmarking, sourcing and procurement, target screening, and others, please send your inquiry to [email protected].

The report is delivered digitally through our online portal. Buyers receive login credentials from our team to access the report and may update their credentials at any time after the initial login.

Delivery timelines depend on the status of the report:

For the most accurate delivery timeline, please contact us to confirm the current status of the report.

Yes. You may request a complimentary preview of the report through a video conference with our team.

Yes. The scope of the report can be fully customized to align with your specific research objectives and information requirements.

Please contact us at [email protected], and our team will be happy to discuss your requirements and propose a tailored solution.

Yes. Selected sections of the report can be purchased separately based on your requirements. Please contact us at [email protected] to discuss your needs.

Yes, AI can help gather publicly available information, but its outputs are only as reliable as the data it accesses. Stratview Research reports are built using validated data, extensive primary interviews with industry stakeholders, and the expertise of our experienced research team.

Additionally, many critical insights, including market dynamics, competitive intelligence, and industry-specific trends, are not publicly available and therefore cannot be captured through AI alone.

The aerospace adhesives and sealants market is likely to grow at a CAGR of 6.9% during 2026-2032.

The aerospace adhesives and sealants market was estimated at USD 1.4 billion in 2025.

The forecasted value of the aerospace adhesives and sealants market is expected to be USD 2.2 billion in 2032.

The market is driven by the industry's relentless pursuit of lightweight materials and designs, aimed at enhancing fuel efficiency and reducing emissions, fuels the demand for high-performance adhesives. Stringent safety and environmental regulations are secondly compelling aerospace manufacturers to seek eco-friendly adhesive solutions. Lastly, continuous advancements in aerospace technology and a growing global aerospace market drive the need for cutting-edge adhesive and sealant formulations that meet evolving industry requirements.

North America is estimated to remain dominant in the market in the foreseeable future, as North America's aerospace industry is known for its commitment to sustainability and environmental responsibility.

Asia-Pacific is estimated to remain the fastest-growing market for aerospace adhesives & sealants in the foreseeable future. Firstly, APAC has emerged as a global hub for aerospace manufacturing, with countries like China, India, Japan, and South Korea investing significantly in their aerospace industries. Secondly, the APAC region benefits from a lower cost of production and labor, making it an attractive destination for aerospace manufacturing.

Epoxy is expected to remain the dominant resin in the market during the forecast period due to its exceptional performance characteristics

3M, Henkel AG & Co., KGaA, Huntsman Corporation, PPG Industries Inc., and Cytec Solvay Group are the leading players in the market.

WE ACCEPT