404

+1-313-307-4176

Aircraft Engine Valves Market Analysis | 2025-2034

Aircraft Engine Valves Market Size, Share, Trends, Dynamics, Forecast, Growth Analysis: 2025-2034

Aircraft Engine Valves Market is segmented by Valve Type (Pneumatic Valves [Starter Valve, Bleed Air Valve, Pressure Relief Valve, Shut-off Valve, and Other Valves], Hydraulic Valves [Selector Valve, Shut-off Valve, and Other Valves], Fuel Valves [Solenoid Valve, Motor-Operated Valve, Manually Operated Gate Valve, Hand Operated Valve, and Other Valves], and Other Valves), by Aircraft Type (Commercial Aircraft, General Aviation, Business Aircraft, Military Aircraft, Helicopter, and Unmanned Air Vehicle), by Material Type (Stainless Steel, Titanium, Aluminium, and Composites), by End-User Type (OEM and Aftermarket), and by Region (North America [The USA, Canada, and Mexico], Europe [Germany, France, The UK, Russia, and Rest of Europe], Asia-Pacific [China, Japan, India, and Rest of Asia-Pacific], and Rest of the World [Brazil, Saudi Arabia, and Others]).

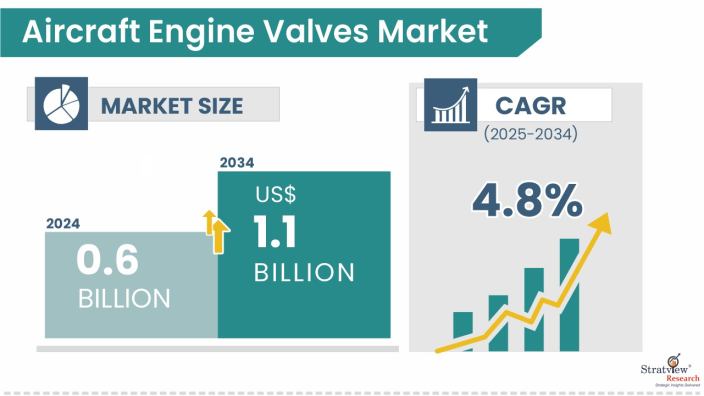

The aircraft engine valves market was estimated at USD 0.6 billion in 2024 and is likely to grow at a CAGR of 4.8% during 2025-2034 to reach USD 1.1 billion in 2034.

Wish to get a free sample? Click Here

Aircraft engine valves are critical components in modern aircraft systems, responsible for controlling the flow of fluids and gases, such as air, fuel, oil, and hydraulic fluids, within various subsystems of the engine. These valves ensure efficient combustion, temperature control, pressure regulation, and overall engine performance, making them essential to both the safety and functionality of aircraft engines. Depending on their application, these valves are categorized into pneumatic valves (such as starter valves, bleed air valves, and pressure relief valves), hydraulic valves (such as selector and shut-off valves), and fuel valves (such as solenoid and motor-operated valves), among others.

The aircraft engine valves market is poised for steady growth, driven by the ongoing expansion of the global aviation industry. Key growth factors include the increasing production of commercial aircraft to meet the surging demand for air travel, growing defense budgets supporting military aircraft modernization, and the rising popularity of unmanned aerial vehicles (UAVs) in both defense and commercial applications. Moreover, the continuous technological advancements in valve materials, such as the integration of lightweight, high-strength alloys like titanium and composites, are enhancing valve performance, reducing weight, and increasing fuel efficiency, which aligns with the aviation industry's push for sustainability.

Furthermore, the aftermarket segment is witnessing growing demand due to the need for regular maintenance, repair, and overhaul (MRO) services across aging aircraft fleets, especially in developing regions. The shift toward next-generation aircraft engines, which demand more sophisticated and reliable valve systems, is also expected to boost the adoption of advanced engine valves. Together, these factors are contributing to the robust outlook for the aircraft engine valves market across both OEM and aftermarket channels, across various aircraft types, including commercial jets, business jets, general aviation aircraft, helicopters, and military platforms.

A considerable number of strategic alliances, including M&As, JVs, etc., have been performed over the past few years:

|

Segmentations |

List of Sub-Segments |

Segments with High-Growth Opportunity |

|

Valve-Type Analysis |

Pneumatic Valves, Hydraulic Valves, Fuel Valves, and Other Valves |

Pneumatic valves are estimated to dominate the market and register the fastest growth in the coming years |

|

Aircraft-Type Analysis |

Commercial Aircraft, General Aviation, Business Aircraft, Military Aircraft, Helicopter, and Unmanned Air Vehicle |

Commercial aircraft are expected to account for the largest market share and witness the fastest growth throughout the forecast period. |

|

Material-Type Analysis |

Stainless Steel, Titanium, Aluminium, Composites |

Titanium is anticipated to be the dominant material type in the market during the forecast period. |

|

End-User-Type Analysis |

OEM and Aftermarket |

OEMs are projected to be the dominant end user, while the aftermarket segment is expected to grow at the fastest rate during the forecast period. |

|

Regional Analysis |

North America, Europe, Asia-Pacific, and The Rest of the World |

North America is expected to retain its leading position throughout the forecast period, while Asia-Pacific is projected to grow at the fastest pace. |

“Pneumatic valves are projected to lead the aircraft engine valves market and grow at the fastest pace during the forecast period.”

Based on valve type, the aircraft engine valves market is segmented as hydraulic valves, pneumatic valves, fuel valves, and other valves.

Pneumatic valves are expected to dominate the aircraft engine valves market, and this dominance is primarily attributed to the growing adoption of advanced air management systems in modern aircraft engines. Pneumatic valves play a crucial role in managing various engine functions such as starting procedures, air bleed control, pressure relief, and temperature regulation, all of which are vital for optimal engine performance and fuel efficiency. Their usage is expanding due to the increasing complexity of aircraft engines, which require more precise and responsive control systems.

Additionally, the emphasis on lightweight systems in the aviation industry has accelerated the preference for pneumatic actuation over hydraulic systems in certain engine applications. Pneumatic systems are generally lighter and less complex, leading to reduced maintenance requirements and improved operational efficiency, which aligns well with the current trends in aircraft design. The growing number of commercial aircraft deliveries, especially in emerging economies, and the expanding global aircraft fleet further contribute to the increasing demand for pneumatic valves.

Moreover, with the rising focus on sustainable aviation, newer engine designs are incorporating more advanced and electronically controlled pneumatic valves to support enhanced fuel economy and reduced emissions. These trends, coupled with continuous innovation in valve technologies and materials, are expected to propel the growth of pneumatic valves faster than other valves, such as hydraulic and fuel valves, solidifying their leading position in the market.

“Commercial aircraft are projected to be the major demand generator for aircraft engine valves throughout the forecast period.”

Based on aircraft type, the aircraft engine valves market is categorized into commercial aircraft, general aviation, business aircraft, military aircraft, helicopters, and unmanned aerial vehicles.

Commercial aircraft are expected to remain the primary demand driver for aircraft engine valves throughout the forecast period. This dominance is largely fueled by the significant growth in global air travel, which has led to a continuous rise in the production and delivery of commercial aircraft by major OEMs such as Airbus and Boeing. As airlines expand their fleets to meet increasing passenger traffic, especially in emerging economies across Asia-Pacific and the Middle East, the demand for engine components, including a wide range of valves for pneumatic, hydraulic, and fuel systems, is experiencing a parallel surge.

The stringent regulatory requirements related to fuel efficiency, emissions reduction, and noise control have prompted aircraft manufacturers to develop next-generation engines with more complex and efficient valve systems. These advanced engines require a higher number of precisely engineered valves to manage air and fluid flow effectively, thus boosting demand in the commercial aviation industry.

Furthermore, the high utilization rate of commercial aircraft, compared to other aircraft types, results in frequent maintenance, repair, and overhaul (MRO) cycles. This drives consistent demand for replacement and upgraded engine valves in the aftermarket segment. With large backlogs of commercial aircraft orders, rising low-cost carrier operations, and an increasing emphasis on fleet modernization, the commercial aircraft segment will continue to represent the largest and most dynamic market for aircraft engine valves during the forecast period.

“Titanium is likely to be the most preferred material type for aircraft engine valves during the forecast period.”

By material type, the aircraft engine valves market is segmented as stainless steel, titanium, aluminum, and composites.

Titanium is anticipated to be the most preferred material for aircraft engine valves in the coming years due to its exceptional strength-to-weight ratio, high temperature resistance, and superior corrosion resistance. In modern aircraft engines, components are subjected to extreme thermal and mechanical stress. Titanium offers the structural integrity required to withstand these harsh operating conditions while significantly reducing overall weight, an essential factor for improving fuel efficiency and performance in aviation.

The growing trend toward lightweighting in aerospace design, aimed at reducing emissions and improving operational efficiency, further reinforces the use of titanium in critical engine components such as valves. Unlike stainless steel, which is heavier, or aluminum, which lacks the necessary high-temperature strength, titanium provides an ideal balance between durability and weight savings, making it a material of choice for next-generation engine designs.

Additionally, with the increasing use of turbofan and high-bypass ratio engines in commercial and military aircraft, the demand for high-performance materials like titanium is gaining momentum. OEMs are incorporating more titanium components into their engines to meet performance, efficiency, and regulatory standards. As a result, titanium is expected to see accelerated adoption across both new aircraft manufacturing and retrofit applications, positioning it as the leading material type in the aircraft engine valves market.

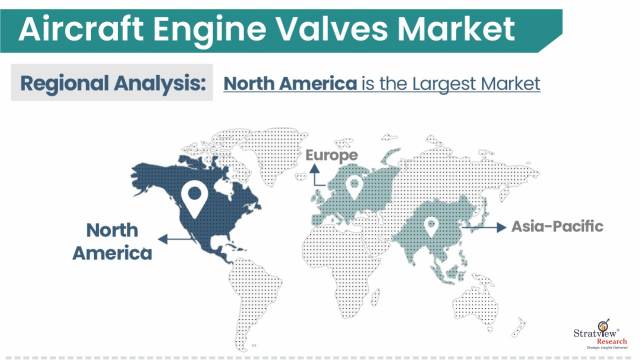

“North America is projected to remain the dominant market, whereas Asia-Pacific is anticipated to expand at the highest growth rate in the coming years.”

North America is anticipated to retain its position as the dominant market for aircraft engine valves throughout the forecast period. This is primarily due to the region’s strong presence of major aircraft and engine OEMs such as Boeing, Lockheed Martin, General Electric, and Pratt & Whitney, which significantly contribute to sustained demand for engine components, including valves. The region also benefits from a robust defense aviation industry, with consistent government spending on military aircraft modernization and maintenance programs, further driving the consumption of high-performance engine valves.

In addition, the large commercial aircraft fleet operating in North America generates steady aftermarket demand for maintenance, repair, and overhaul (MRO) activities, including the replacement of engine valves. The U.S. Federal Aviation Administration's (FAA) strict safety and performance regulations encourage the adoption of advanced valve technologies, thereby supporting market maturity and technological innovation in the region.

On the other hand, Asia-Pacific is anticipated to register the highest growth rate in the aircraft engine valves market, driven by a combination of rapid economic development, rising air passenger traffic, and aggressive fleet expansion by regional airlines. Countries like China, India, and Southeast Asian nations are investing heavily in both commercial and defense aviation industries. This is leading to increased procurement of new aircraft and development of indigenous manufacturing capabilities, including engine components.

Moreover, the region is becoming a manufacturing hub for global aerospace companies, with growing investments in setting up production and MRO facilities. As a result, Asia-Pacific is not only emerging as a major consumption center but also as a contributor to the global aircraft supply chain. These factors collectively position Asia-Pacific as the fastest-growing region, poised to capture a larger share of the aircraft engine valves market in the years to come.

Know the high-growth countries in this report. Register Here

The following are the key players in the aircraft engine valves market.

Here is the list of the Top Players (Based on Dominance)

Note: The above list does not necessarily include all the top players in the market.

Are you the leading player in this market? We would love to include your name. Please write to us at [email protected]

This strategic assessment report, from Stratview Research, provides a comprehensive analysis that reflects today’s aircraft engine valves market realities and future market possibilities for the forecast period of 2025 to 2034. After a continuous interest in our aircraft engine valves market report from the industry stakeholders, we have tried to further accentuate our research scope to the aircraft engine valves market to provide the most crystal-clear picture of the market. The report segments and analyses the market in the most detailed manner to provide a panoramic view of the market. The vital data/information provided in the report can play a crucial role for the market participants as well as investors in the identification of the low-hanging fruits available in the market as well as to formulate the growth strategies to expedite their growth process.

This report offers high-quality insights and is the outcome of a detailed research methodology comprising extensive secondary research, rigorous primary interviews with industry stakeholders, and validation and triangulation with Stratview Research’s internal database and statistical tools. More than 1000 authenticated secondary sources, such as company annual reports, fact books, press releases, journals, investor presentations, white papers, patents, and articles, have been leveraged to gather the data. We conducted more than 15 detailed primary interviews with the market players across the value chain in all four regions and industry experts to obtain both qualitative and quantitative insights.

This report provides market intelligence most comprehensively. The report structure has been kept so that it offers maximum business value. It provides critical insights into market dynamics and will enable strategic decision-making for existing market players as well as those willing to enter the market. The following are the key features of the report:

This report studies the market, covering a period of 12 years of trends and forecasts. The report provides detailed insights into the market dynamics to enable informed business decision-making and growth strategy formulation based on the opportunities present in the market.

The aircraft engine valves market is segmented into the following categories:

By Valve Type

By Aircraft Type

By Material Type

By End-User Type

By Region

With this detailed report, Stratview Research offers one of the following free customization options to our respectable clients:

Company Profiling

Competitive Benchmarking

Custom Research: Stratview Research offers custom research services across sectors. In case of any custom research requirement related to market assessment, competitive benchmarking, sourcing and procurement, target screening, and others, please send your inquiry to [email protected]

The report is delivered digitally through our online portal. Buyers receive login credentials from our team to access the report and may update their credentials at any time after the initial login.

Delivery timelines depend on the status of the report:

For the most accurate delivery timeline, please contact us to confirm the current status of the report.

Yes. You may request a complimentary preview of the report through a video conference with our team.

Yes. The scope of the report can be fully customized to align with your specific research objectives and information requirements.

Please contact us at [email protected], and our team will be happy to discuss your requirements and propose a tailored solution.

Yes. Selected sections of the report can be purchased separately based on your requirements. Please contact us at [email protected] to discuss your needs.

Yes, AI can help gather publicly available information, but its outputs are only as reliable as the data it accesses. Stratview Research reports are built using validated data, extensive primary interviews with industry stakeholders, and the expertise of our experienced research team.

Additionally, many critical insights, including market dynamics, competitive intelligence, and industry-specific trends, are not publicly available and therefore cannot be captured through AI alone.

Aircraft engine valves are mechanical components used to control the flow of fluids and gases, such as air, fuel, oil, and hydraulic fluids, within an aircraft engine. They play a critical role in managing engine operations, including starting, combustion, pressure regulation, cooling, and shutdown. Depending on their function and the system they serve, these valves can be pneumatic, hydraulic, or fuel-related, and are designed to withstand extreme temperatures, pressures, and vibrations to ensure safe and efficient engine performance.

The aircraft engine valves market is projected to expand at a CAGR of 4.8% in the coming years, reaching a value of approximately USD 1.1 billion by 2034.

The key drivers propelling the aircraft engine valves market include the rising global demand for air travel, which is leading to increased production of commercial aircraft, and the modernization of military fleets across various countries. Additionally, the growing need for fuel-efficient and lightweight engines is pushing the adoption of advanced valve technologies made from high-performance materials like titanium. The expanding aftermarket for aircraft maintenance and repair, especially due to aging aircraft fleets, also contributes significantly to market growth.

North America represents the largest market for aircraft engine valves, primarily due to its advanced aerospace ecosystem, high defence expenditure, and the presence of leading aircraft and engine manufacturers such as Boeing, Raytheon Technologies, GE Aerospace, and Honeywell. The region benefits from a well-established network of OEMs, MRO providers, and suppliers, which supports consistent demand for both new engine valves and aftermarket replacements. Additionally, continuous investments in military modernization programs, rising aircraft deliveries, and a strong focus on technological innovation, such as the integration of smart valve systems, further reinforce North America's dominance in this market. The region's regulatory environment and emphasis on aircraft safety and performance also drive the adoption of advanced valve solutions.

Asia-Pacific is the fastest-growing market for aircraft engine valves, fuelled by rapid expansion in commercial aviation, increasing air passenger traffic, and rising investments in indigenous aircraft manufacturing across countries like China, India, and Japan. The region is witnessing significant growth in fleet size, infrastructure development, and defense modernization programs, which are driving demand for new aircraft and associated engine components. Additionally, the emergence of local OEMs and growing MRO capabilities are further accelerating the adoption of advanced valve technologies in the region.

Parker Hannifin Corporation, Honeywell International Inc., Woodward Inc., Transdigm Group Inc., Liebherr Group, Raytheon Technologies Corporation, General Electric Company, and Safran S.A. are the leading players in the aircraft engine valves market.

Commercial aircraft represent the dominant segment in the aircraft engine valves market. This is primarily due to the large global fleet size and the high production rates of commercial jets to meet growing passenger and cargo demand. These aircraft require a significant number of engine valves for various functions, including air, fuel, and hydraulic flow control. Additionally, frequent maintenance and overhaul cycles in commercial aviation drive consistent demand for replacement valves, further solidifying this segment’s leading position in the market.

WE ACCEPT