404

+1-313-307-4176

Ceramic Matrix Composites Market | 2026-2034

Ceramic Matrix Composites Market Size, Share, Trend, Forecast, Competitive Analysis, and Growth Opportunity: 2026-2034

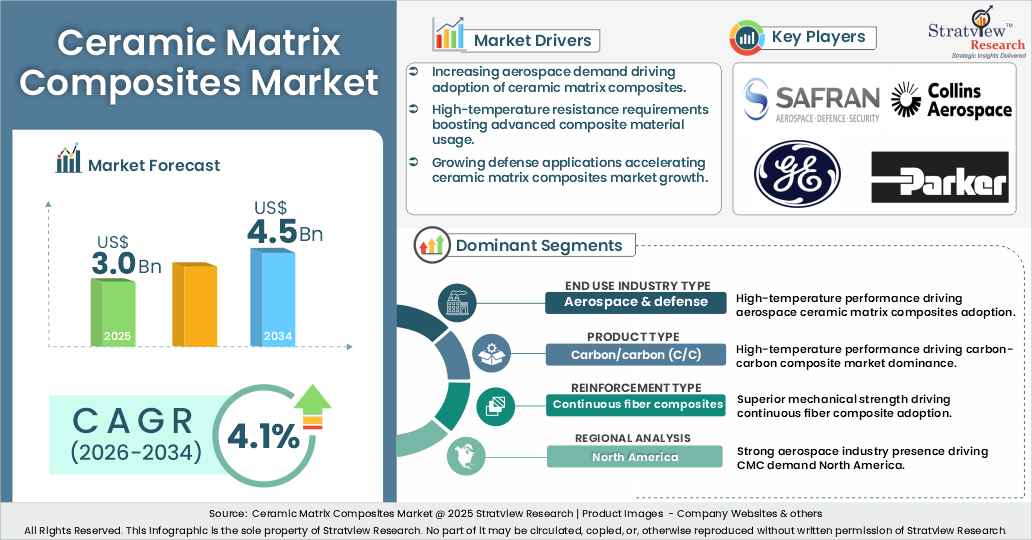

“The ceramic matrix composites market size/value was US$ 3.0 billion in 2025 and is likely to grow at a decent CAGR of 4.1in the long run to reach US$ 4.5 billion in 2034.”

Want to get a free sample? Register Here

Ceramic Matrix Composites (CMCs) are advanced materials combining ceramic matrices with fiber reinforcements, offering exceptional thermal stability, oxidation resistance, and lightweight characteristics. These materials are increasingly used in high-temperature and performance-critical applications such as aircraft engines, braking systems, energy systems, and semiconductor processing equipment. Their ability to operate at higher temperatures than conventional metals enable improved efficiency, reduced emissions, and enhanced durability across industries, driven by rising aircraft production, increasing engine demand, and a strong focus on fuel-efficient technologies; however, their broader adoption remains constrained by high production costs, limited fiber supply, complex manufacturing processes, and limited advanced manufacturing infrastructure. The CMCs market is witnessing steady product development driven by increasing adoption in aerospace engines, ongoing investments in manufacturing capacity, and growing interest from automotive, defense, and energy applications. Engine manufacturers are integrating more CMC components to improve efficiency and high-temperature performance, while material suppliers are expanding silicon-carbide fiber and composite production to support future demand.

The CMC market is witnessing a clear shift from early-stage R&D collaborations to industrial-scale strategic alliances and vertically integrated partnerships, particularly across the aerospace value chain. Companies are increasingly co-investing in upstream materials and downstream component manufacturing to secure supply chains, overcome fiber bottlenecks, and accelerate commercialization. Additionally, recent spin-offs and institutional collaborations highlight a growing focus on scaling production, improving cost efficiency, and strengthening regional manufacturing ecosystems. A considerable number of strategic alliances, including M&As, JVs, etc., have been performed over the past few years:

|

Ceramic Matrix Composites Market Report Overview |

|

|

Trend & Forecast Period |

2026-2034 |

|

Regions Covered |

North America, Europe, Asia-Pacific, Rest of the World |

|

CAGR (2026-2034) |

4.1% |

|

Countries/Subregions Covered |

The USA, Canada, Mexico, Germany, France, Russia, The UK, China, Japan, India, Brazil, Argentina and Others |

|

Figures & Tables |

>150 |

|

Customization |

Up to 10% customization available free of cost |

|

Segmentations |

List of Sub-Segments |

Segments with High-Growth Opportunity |

|

End Use Industry Type Analysis |

Aerospace & Defense, Transportation, Electrical & Electronics, Industrial, and Other Industries |

The Aerospace & Defense accounts for the largest share of the CMCs market due to the material’s high-temperature resistance and low weight, followed by transportation. |

|

Product-Type Analysis |

Oxide/Oxide (Ox/Ox), Silicon Carbide/Silicon Carbide (SiC/SiC), Carbon/Carbon (C/C), and Others |

C/C composites dominate the CMCs market, reflecting their long-established use in extreme-high-temperature environments such as aerospace and automotive brakes and thermal protection systems. |

|

Reinforcement-Type Analysis |

Continuous Fiber Composites, Short Fiber Composites, and Other Composites |

Continuous fibre composites are expected to remain dominant due to their superior mechanical strength, fracture toughness, and high-temperature performance. |

|

Region Analysis |

North America, Europe, Asia-Pacific, and The Rest of the World |

North America leads the global CMCs market, supported by the strong presence of major A&D OEMs, advanced materials innovation, and well-established manufacturing capabilities, followed by Europe. |

“Aerospace & defense is expected to remain dominant, whereas electrical & electronics and transportation are likely to be the fastest-growing end users during the forecast period.”

The ceramic matrix composites market is segmented into aerospace & defense, transportation, electrical & electronics, industrial, and other industries. Aerospace & defense is expected to remain dominant, whereas electrical & electronics and transportation are likely to be the fastest-growing end users during the forecast period.

The dominance of aerospace & defense is driven by the extensive use of CMCs in aircraft engines and braking systems, where high-temperature resistance, lightweight properties, and superior mechanical performance are critical. The presence of leading aerospace OEMs, high defense spending, and continuous investments in next-generation propulsion systems further support sustained demand for CMCs in this segment.

The fastest growth in electrical & electronics and transportation is primarily attributed to increasing adoption of CMCs in semiconductor processing equipment, high-power electronics, and high-performance braking systems. Rising demand for energy-efficient systems, miniaturization of electronic components, and the need for durable materials in extreme environments are accelerating CMC penetration beyond traditional aerospace applications.

“Carbon/carbon (C/C) is expected to remain dominant, whereas SiC/SiC and oxide/oxide (Ox/Ox) are likely to be the fastest-growing product types during the forecast period.”

The ceramic matrix composites market is segmented into oxide/oxide (Ox/Ox), silicon carbide/silicon carbide (SiC/SiC), carbon/carbon (C/C), and others. Carbon/carbon (C/C) is expected to remain dominant, whereas SiC/SiC and Ox/Ox are likely to be the fastest-growing product types during the forecast period. The dominance of carbon/carbon (C/C) is driven by its extensive use in aerospace braking systems and high-temperature applications, where its lightweight nature, high thermal shock resistance, and superior friction performance are critical. Its established presence in aircraft brake systems and long-standing commercial adoption continue to support its leading position in the market.

The fastest growth in SiC/SiC and Ox/Ox composites is primarily attributed to their superior oxidation resistance, higher durability, and increasing adoption in next-generation aircraft engines and industrial applications. As demand for higher efficiency, lower emissions, and longer component life increases, these materials are gaining traction across aerospace, energy, and electronics applications.

Want to get more details about the segmentations? Register Here

“Continuous fiber composites are expected to remain dominant, whereas short fiber is likely to be the fastest-growing reinforcement type during the forecast period.”

The ceramic matrix composites market is segmented into continuous fiber composites, short fiber composites, and other composites. Continuous fiber composites are expected to remain dominant, whereas short fiber composites are likely to be the fastest-growing reinforcement type during the forecast period. The dominance of continuous fiber composites is driven by its superior mechanical strength, high-temperature stability, and load-bearing capability, making it the preferred choice for critical aerospace applications such as aircraft engines and braking systems. Its ability to deliver reliable performance under extreme operating conditions continues to support its widespread adoption.

The fastest growth in short fiber composites is primarily attributed to their cost advantages and suitability for near-net-shape manufacturing processes such as injection molding and slip casting. These characteristics make them increasingly attractive for transportation, industrial, and electronics applications, where complex geometries and cost efficiency are key requirements.

“North America is expected to remain dominant, whereas Asia-Pacific is likely to be the fastest-growing region during the forecast period.”

The dominance of North America is driven by the strong presence of leading aerospace and defense players, advanced manufacturing capabilities, and high defense spending, particularly in the US, which serves as the key market in the region. Additionally, continuous investments in next-generation aircraft engines and propulsion systems further strengthen regional demand. Europe also holds a significant share, led by countries such as France, Germany, and the UK, supported by established aerospace OEMs and a robust industrial base.

The fastest growth in Asia-Pacific is primarily driven by increasing aerospace investments, expanding industrial capabilities, and growing demand for advanced materials, particularly in China, Japan, and India. Government initiatives to develop domestic aerospace manufacturing and the rising adoption of high-performance materials across industries are further accelerating market growth in the region.

The market is moderately concentrated, with the top five players having relatively higher market share, and the remaining shares are covered by many regional players. Most of the major players compete in some of the governing factors, including price, service offerings, and regional presence, etc. The following are the key players in the ceramic matrix composites market. Some of the major players provide a complete range of services, including engine and airframe.

Here is the list of the Top Players (Based on Dominance)

Note: The above list does not necessarily include all the top players in the market.

Are you the leading player in this market? We would love to include your name. Please write to us at [email protected]

This report provides market intelligence most comprehensively. The report structure has been kept so that it offers maximum business value. It provides critical insights into market dynamics and will enable strategic decision-making for existing market players as well as those willing to enter the market. The following are the key features of the report:

The global ceramic matrix composites market is segmented into the following categories.

By End Use Industry Type

By Product Type

By Reinforcement Type

By Region

With this detailed report, Stratview Research offers one of the following free customization options to our respected clients:

Company Profiling

Competitive Benchmarking

Custom Research: Stratview Research offers custom research services across industries. In case of any custom research requirement related to market assessment, competitive benchmarking, sourcing and procurement, target screening, and others, please send your inquiry to [email protected]

Ceramic matrix composites (CMCs) are engineered materials made by embedding high-strength fibers within a ceramic base, resulting in a lightweight structure that can withstand extreme temperatures, mechanical stress, and harsh operating environments better than conventional materials.

The global ceramic matrix composites market is projected to reach approximately US$ 4.5 billion by 2034, driven by increasing adoption in aerospace engines, braking systems, and high-temperature industrial applications.

The ceramic matrix composites market is estimated to grow at a CAGR of 4.1% by 2034, driven by increasing adoption in aerospace engines, high-performance braking systems, and energy applications.

The key drivers include the rising production of aircraft and increasing engine output, along with the growing adoption of CMC components in next-generation engines. Additionally, the strong industry focus on fuel efficiency and low-emission technologies is further accelerating the demand for CMCs across aerospace and related applications.

Aerospace & defense is the key segment offering high-growth opportunities in the ceramic matrix composites market, driven by increasing adoption in aircraft engines, braking systems, and thermal protection systems, supported by rising demand for lightweight, high-temperature, and fuel-efficient technologies.

North America holds the largest market share in the ceramic matrix composites market, primarily driven by the US, which leads due to its strong aerospace and defense ecosystem, advanced manufacturing capabilities, and significant investments in next-generation propulsion technologies.

Asia-Pacific is expected to witness the highest market growth in the ceramic matrix composites market during the forecast period, driven by expanding aerospace investments, strengthening domestic manufacturing capabilities, and increasing adoption of advanced materials across countries such as China, Japan, and India.

Safran S.A., Collins Aerospace, Honeywell Aerospace Technologies, Brembo SGL Carbon Ceramic Brakes, Parker Meggitt, GE Aerospace, CoorsTek, CeramTec GmbH, Morgan Advanced Materials, and Pratt & Whitney are the leading players in the ceramic matrix composites market.

WE ACCEPT