")

404

+1-313-307-4176

Industrial Flooring Market Growth Analysis Report (2023-2028)

")

Industrial Flooring Market Size, Share, Trend, Forecast, Competitive Analysis, and Growth Opportunity: 2023-2028

Industrial Flooring Market, by Material Type (Epoxy, PU Resin, PU Cement, MMA, and Others), Application Type (Food & Beverage, Healthcare, Industrial Manufacturing, Automotive Manufacturing, and Others), and Region (North America [The USA, Canada, and Mexico], Europe [Germany, France, The UK, Austria, Italy, Spain, and Rest of Europe], Asia-Pacific [China, India, Japan, and Rest of Asia-Pacific], and Rest of the World [Brazil, Saudi Arabia, and Others]).

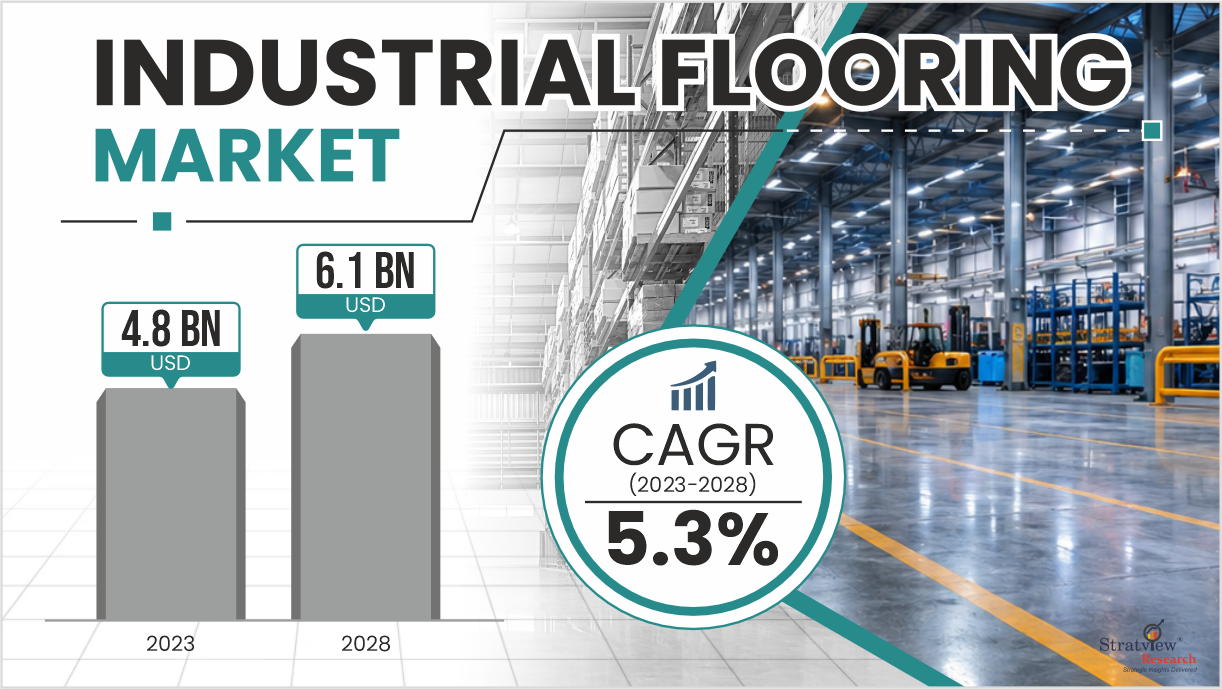

"The global industrial flooring market was valued at USD 4.8 billion in 2023 and is likely to register a promising CAGR of 5.3% to reach USD 6.1 billion by 2028."

Want to get a free sample? Register Here

For industrial environments, there are a variety of flooring solutions, each with different characteristics. It is a big challenge for the company to simultaneously maintain its flooring along with the business operations. This gives birth to huge repair and maintenance costs. Therefore, it is vital for companies to invest in durable, resistant, and low-maintenance floors. Industrial floors are majorly classified according to the material from which they are made, which can be epoxy, polyurethane, and MMA. The company must understand the type of industrial floor that is best suited for its operations. Cost, durability, aesthetics, and maintenance requirements are some of the major criteria in the selection of a type of flooring. Currently, epoxy and concrete are referred to as the best industrial flooring options.

Epoxy flooring is the preferred choice for industrial workplaces, which is commonly selected because of its high versatility and durability. Epoxy flooring is made from several strong epoxy layers, as opposed to just one layer in epoxy coating. Therefore, it can withstand constant and heavy traffic and is also easy to clean and maintain.

|

Industrial Flooring Market Report Overview |

|

|

Market Size in 2023 |

USD 4.8 Billion |

|

Market Size in 2028 |

USD 6.1 Billion |

|

Market Growth (2023-2028) |

CAGR of 5.3% |

|

Base Year of Study |

2022 |

|

Trend Period |

2017-2021 |

|

Forecast Period |

2023-2028 |

The market for industrial flooring is gradually consolidating every year as many companies are engaged in mergers & acquisitions to quickly gain a market-leading position and tap the growing opportunities in the briskly expanding market. For example, in 2021, RPM’s division Carboline acquired Dudik Inc., a standalone world leader in high-performance coatings, flooring, and tank linings. Similarly, The Sherwin-Williams Company acquired Tennant Coatings in 2021, and COVESTRO Group acquired Industrials & Functional Materials Business from Royal DSM, which will enhance its global network.

Growing emphasis on workplace safety and hygiene compliance across industries such as food processing, pharmaceuticals, healthcare, and manufacturing is increasing demand for anti-slip, chemical-resistant, and seamless industrial flooring systems.

According to the U.S. Bureau of Labor Statistics (2025), fatal workplace injuries in the U.S. declined by 4.0% in 2024, reflecting stronger industrial focus on occupational safety standards. This broader emphasis on safer work environments is supporting industrial flooring market growth through increased adoption of anti-slip and durable flooring solutions

Expansion of manufacturing plants, warehouses, logistics hubs, and commercial facilities is increasing installation demand for high-performance industrial flooring materials. Rising industrialization and infrastructure investments in emerging economies are further supporting industrial flooring market growth.

According to the U.S. Census Bureau, U.S. construction spending reached a seasonally adjusted annual rate of USD 2.19 trillion in March 2026, reflecting continued growth in industrial and commercial infrastructure projects, which is increasing demand for epoxy, polyurethane, and concrete-based flooring systems.

Supporting this trend, India’s Index of Industrial Production (IIP) increased by 7.8% in December 2025, indicating strong growth in manufacturing activity and industrial output, thereby increasing demand for durable flooring solutions across production and storage facilities.

Downtime During Flooring Installation

Industrial flooring installation and repair activities often require temporary shutdowns of manufacturing lines or warehouse operations, leading to production delays and operational losses for facility operators, which may hinder overall market growth.

Flooring systems such as epoxy and polyurethane coatings often require extended curing and drying periods, limiting operational continuity in facilities running 24/7 production schedules.

Stringent Environmental Compliance Requirements

Increasing regulations related to VOC emissions, hazardous chemicals, and sustainable construction materials are creating challenges for flooring manufacturers to develop environmentally compliant products without compromising durability and performance.

Growing adoption of green building standards and sustainability certifications is increasing pressure on manufacturers to invest in low-VOC and eco-friendly flooring formulations, raising production and compliance costs.

Growing Adoption of Sustainable Flooring Materials

Increasing demand for low-VOC, recyclable, and environmentally friendly flooring solutions is creating growth opportunities for manufacturers developing sustainable and energy-efficient flooring materials.

According to the United Nations Environment Programme, the buildings sector accounts for approximately 37% of global CO₂ emissions, accelerating demand for sustainable construction materials across industrial and commercial infrastructure projects. This is creating opportunities for industrial flooring manufacturers offering low-emission, recyclable, and environmentally compliant flooring systems.

Growing Demand for Renovation & Facility Upgradation

Increasing renovation and modernization activities across aging industrial facilities are creating opportunities for advanced flooring materials with improved durability, chemical resistance, and safety performance.

Industries are increasingly replacing conventional concrete surfaces with high-performance coatings and seamless flooring materials to improve operational efficiency and comply with evolving workplace safety standards, expanding the industrial flooring market trend.

|

Segmentations |

List of Sub-Segments |

Dominant and Fastest-Growing Segments |

|

|

Material Type |

Epoxy, PU Resin, PU Cement, MMA, and Others |

|

|

|

Application Type |

Food & Beverage, Healthcare, Industrial Manufacturing, Automotive Manufacturing, and Others |

|

|

|

Region |

North America, Europe, Asia Pacific, and the Rest of the World |

Asia-Pacific is expected to remain the dominant region, whereas Europe is likely to remain the second-leading regional market. |

“Epoxy is expected to remain the dominant material type, whereas MMA is likely to witness the fastest growth during the forecast period.”

Based on material type, the industrial flooring market is segmented into epoxy, PU resin, PU cement, MMA (methyl methacrylate), and others. Epoxy is expected to maintain its dominance during the forecast period due to its cost-effectiveness, strong adhesion, chemical resistance, and durability across industrial environments.

Epoxy flooring is widely used across manufacturing plants, warehouses, automotive facilities, and commercial buildings owing to its low maintenance requirements and long service life. Increasing industrial construction and facility modernization activities are further supporting industrial flooring market growth for epoxy-based systems.

MMA is projected to witness the fastest growth during the forecast period due to its rapid curing capability, superior low-temperature performance, and reduced installation downtime. The material is increasingly gaining traction in food processing, cold storage, and healthcare facilities where operational continuity is critical.

“Industrial manufacturing accounted for the largest market share.”

Based on application type, the market is segmented into food & beverage, healthcare, automotive manufacturing, industrial manufacturing, and others. Industrial manufacturing is expected to remain the dominant application segment due to rising investments in manufacturing facilities, warehouses, logistics hubs, and heavy industrial infrastructure.

Industrial flooring systems are increasingly used in manufacturing environments requiring abrasion resistance, heavy-load tolerance, chemical protection, and operational safety. Expansion of industrial production activities across emerging economies is further driving industrial flooring market demand.

Food & Beverage is projected to witness the fastest growth during the forecast period owing to increasing hygiene regulations, demand for seamless flooring systems, and rising adoption of anti-microbial and chemical-resistant flooring materials in processing facilities.

“Asia-Pacific is expected to remain the dominant region, whereas Europe is likely to remain the second-leading regional market."

In terms of region, Asia-Pacific is expected to remain the dominant market for industrial flooring during the forecast period. Rapid industrialization, expanding manufacturing activities, increasing warehouse construction, and rising infrastructure investments in China, India, and Southeast Asian countries are driving regional market growth.

China accounts for a major share of the regional market due to its large industrial base and continuous investments in manufacturing and logistics infrastructure. Growing penetration of industrial flooring solutions across automotive, electronics, food processing, and pharmaceutical industries is further supporting market expansion.

Europe is likely to remain the fastest-growing market for industrial flooring owing to the strong presence of automotive manufacturing, food & beverage processing, and pharmaceutical industries. Increasing focus on workplace safety, sustainability standards, and facility modernization is contributing to steady demand for high-performance flooring systems across the region.

Want to get a free sample? Register Here

The market is highly populated with the presence of several local, regional, and global players. Most of the major players compete in some of the governing factors including price, product offerings, regional presence, etc. The following are the key players in the industrial flooring market:

Note: The above list does not necessarily include all the top players in the market.

Are you the leading player in this market? We would love to include your name. Write to us at [email protected]

This report provides market intelligence in the most comprehensive way. The report structure has been kept such that it offers maximum business value. It provides critical insights into market dynamics and will enable strategic decision-making for existing market players as well as those willing to enter the market.

What deliverables will you get in this report?

|

Key questions this report answers |

Relevant contents in the report |

|

How big is the sales opportunity? |

In-depth analysis of the Industrial Flooring Market |

|

How lucrative is the future? |

Market forecast and trend data and emerging trends |

|

Which regions offer the best sales opportunities? |

Global, regional and country level historical data and forecasts |

|

Which are the most attractive market segments? |

Market segment analysis and forecast |

|

Which are the top players and their market positioning? |

Competitive landscape analysis, Market share analysis |

|

How complex is the business environment? |

Porter’s five forces analysis, PEST analysis, Life cycle analysis |

|

What are the factors affecting the market? |

Drivers & challenges |

|

Will I get the information on my specific requirement? |

10% free customization |

The industrial flooring market is segmented into the following categories:

By Material Type

By Application Type

By Region

This strategic assessment report, from Stratview Research, provides a comprehensive analysis that reflects today’s industrial flooring market realities and future market possibilities for the forecast period. The report segments and analyzes the market in the most detailed manner in order to provide a panoramic view of the market. The vital data/information provided in the report can play a crucial role for market participants as well as investors in the identification of the low-hanging fruits available in the market as well as to formulate the growth strategies to expedite their growth process.

This report offers high-quality insights and is the outcome of a detailed research methodology comprising extensive secondary research, rigorous primary interviews with industry stakeholders, and validation and triangulation with Stratview Research’s internal database and statistical tools. More than 1,000 authenticated secondary sources, such as company annual reports, fact books, press releases, journals, investor presentations, white papers, patents, and articles, have been leveraged to gather the data. We conducted more than 15 detailed primary interviews with the market players across the value chain in all four regions and industry experts to obtain both qualitative and quantitative insights.

With this detailed report, Stratview Research offers one of the following free customization options to our respectable clients:

Company Profiling

Competitive Benchmarking

Custom Research: Stratview Research offers custom research services across sectors. In case of any custom research requirement related to market assessment, competitive benchmarking, sourcing and procurement, target screening, and others, please send your inquiry to [email protected]

The industrial flooring market is estimated to grow at a CAGR of 5.3% during 2023-2028. The increase in construction activities, the growing significance of safety and environmental regulations, and the benefits of flooring are some of the market's major driving factors.

Asia Pacific is estimated to remain the dominant region during the forecast period as it is home to numerous processing, manufacturing, and assembly facilities for the pharmaceutical, food & beverage, and automotive industries, ensuring a strong demand in the years to come.

Sika AG, Covestro Group, The Sherwin-Williams Company, BASF SE, PPG Industries, Inc., Jotun, RPM International Inc., and Ardex Group are the leading players in the market.

Europe is estimated to grow at a significant pace in the coming years, driven by increasing industrial facility modernization, stringent workplace safety regulations, and rising demand for sustainable and high-performance flooring solutions across manufacturing and food & beverage industries.

Epoxy is estimated to be dominant in the market in the coming years. Epoxy is preferred for all major applications because of its durability, ease of maintenance, chemical and impact resistance, and ability to prevent wear and tear.

Distributors, suppliers, manufacturers, logistics organizations, and government bodies.

WE ACCEPT