404

+1-313-307-4176

Prepreg Market Growth Analysis | 2026-2031

Prepreg Market Size, Share, Trend, Forecast, Competitive Landscape & Growth Opportunities: 2026-2031

“The prepreg market will reach USD 5.9 billion in 2026 and offers robust growth opportunities for the market stakeholders. With the market expected to grow at a CAGR of 6.5%, the annual sales will hit USD 8.1 billion mark in 2031, driven by the sustained expansion of high-performance composite applications across multiple industries. Growth will be primarily supported by increasing commercial aircraft production to fulfill record order backlogs, rising global defense expenditures, and the growing adoption of lightweight composite materials in aerospace, automotive, marine, and emerging mobility applications.”

The annual demand for prepregs was USD 5.1 billion in 2025 and is expected to reach USD 5.9 billion in 2026, up 15.0% than the value in 2025.

During the forecast period (2026-2031), the market is expected to grow at a CAGR of 6.5%. The annual demand will reach USD 8.1 billion in 2031.

North America had a market share of >40% in 2025, generating the largest demand across regions.

By end-use industry type, aerospace & defense is expected to remain the largest and the fastest-growing segment throughout the forecast period.

By resin type, thermoset prepregs, particularly epoxy-based prepregs, will continue to dominate the market in the coming years.

By fiber type, carbon fiber prepregs are projected to maintain the largest market share during the forecast period.

By form type, unidirectional (UD) prepregs are anticipated to remain the leading segment in the market during the study period.

By process type, autoclave curing is expected to retain its position as the dominant process category in the market.

“According to a senior analyst at Stratview Research, the global prepreg market will generate a cumulative sales opportunity worth USD 40+ billion during 2026-2031. Over the forecast period, Aerospace & Defense will continue to be the primary demand driver, while thermoplastic prepregs, carbon fiber prepregs, unidirectional (UD) prepregs, out-of-autoclave (OoA) processing, and North America are expected to emerge as the most attractive growth opportunities.”

Sharpen Your Strategies To Explore This USD 40+ Billion Opportunity. Get Free Sample Of Our Report: Here.

Have a look at the sales opportunities presented by the prepreg market in terms of growth and market forecast.

|

Market Statistics |

Value (in USD Billion) |

Market Growth (%) |

|

Market Size in 2025 |

USD 5.1 billion |

- |

|

Market Size in 2026 |

USD 5.9 billion |

YoY Growth in 2026: 15.0% |

|

Market Size in 2031 |

USD 8.1 billion |

CAGR 2026-2031: 6.5% |

|

Cumulative Sales Opportunity during 2026-2031 |

USD 40+ billion |

- |

|

Top 10 Countries’ Market Share in 2025 |

USD 4.5 billion+ |

90%+ |

|

Top 5 Companies’ Market Share in 2025 |

USD 2.5 billion+ |

50% - 60% |

Want To Explore The Market Opportunities? Get Free Sample Here

The global prepreg market is being driven by the increasing demand for lightweight, high-strength composite materials across aerospace & defense, automotive, sporting goods, marine, and industrial applications. Prepregs offer superior fiber-resin consistency, excellent mechanical properties, high fatigue resistance, and enhanced manufacturing precision, making them the preferred material for critical structural components. The continued ramp-up in commercial aircraft production, rising defense procurement, and the growing adoption of composite-intensive platforms are significantly accelerating demand for advanced prepreg materials. In addition, the increasing penetration of electric vehicles, advanced air mobility (AAM), and next-generation mobility solutions are creating new growth opportunities for lightweight composite structures.

At the same time, continuous advancements in prepreg manufacturing technologies, including automated fiber placement (AFP), automated tape laying (ATL), and out-of-autoclave (OoA) processing, are improving production efficiency while reducing manufacturing costs and cycle times. The growing commercialization of thermoplastic prepregs, supported by their recyclability, faster processing, and superior impact resistance, is further expanding application areas beyond traditional aerospace markets.

Align With The Mega Trends Shaping The Industry. Get Free Sample Here.

Growing Demand Across Multiple End-Use Industries

The prepreg market growth is being driven by the increasing adoption of high-performance composite materials across multiple end-use industries, including aerospace, automotive, wind energy, and sports equipment. Prepregs provide an excellent strength-to-weight ratio, superior fatigue resistance, and consistent material quality, making them well suited for lightweight structural applications that demand high durability and performance. Their expanding use across these industries continues to support long-term market demand.

For example, the Boeing 787 Dreamliner and Airbus A350 each contain more than 50% composite materials by structural weight. The Boeing 787's composite airframe is approximately 40,000 pounds (18,100 kg) lighter than a conventional design and delivers about 20% better fuel efficiency. Such extensive use of composite structures drives the demand for carbon fiber prepregs used in manufacturing lightweight, high-strength primary aircraft components.

Source:Airbus Commercial Outlook 2026

According to WindEurope, rotor blades are manufactured from composite materials, primarily glass- and carbon-fiber reinforced polymers, because they enable lighter, longer, and more aerodynamic blades. These composite blades improve turbine performance, and the latest wind turbine models are 6–10 times more powerful than early-generation turbines.

Accelerating Global Clean Energy Initiatives

The prepreg market demand is gaining momentum with the global transition toward clean energy and decarbonization. Governments worldwide are expanding renewable energy capacity and implementing policies to reduce carbon emissions, driving investments in advanced wind turbines and other clean energy infrastructure. As prepregs enable the production of lightweight, high-strength, and durable composite components, particularly wind turbine blades, their demand continues to rise alongside clean energy deployment.

In 2025, the U.S. Department of Energy announced over USD 20 million in Bipartisan Infrastructure Law investments to advance recycling technologies for composite wind turbine blades. The initiative highlights the strategic role of composite materials in supporting a more sustainable wind energy sector, reinforcing long-term prepreg market demand.

According to the IEA, global investment in clean energy is expected to exceed USD 2.2 trillion in 2025, nearly twice the investment in fossil fuels. Growing investments in renewable energy infrastructure, particularly wind power, are increasing the demand for composite-intensive components manufactured using prepregs.

Expanding Hydrogen Storage Infrastructure

The prepreg market demand is being driven by the rapid expansion of hydrogen storage infrastructure to support the global hydrogen economy. High-pressure hydrogen storage systems require lightweight, high-strength composite pressure vessels capable of safely storing hydrogen at elevated pressures. Carbon fiber prepregs are widely used in manufacturing Type III and Type IV composite storage tanks, making them a critical material for hydrogen production, transportation, and refueling infrastructure.

According to the International Energy Agency (IEA), more than 1,500 hydrogen projects had been announced globally by 2025, with approximately USD 75 billion reaching final investment decision. The resulting expansion of hydrogen infrastructure is expected to increase the adoption of Type IV carbon fiber composite storage tanks, driving prepreg market demand.

“As per our analyst, the prepreg industry is entering a new phase where advanced material innovation, lightweight engineering, manufacturing automation, and sustainability are becoming the primary competitive differentiators. Future growth will be driven by increasing aircraft production, rising defense investments, expanding adoption of lightweight composites across transportation and industrial sectors, rapid commercialization of thermoplastic prepregs, and continuous advancements in automated composite manufacturing technologies.”

High Capital Investment and Processing Costs

The prepreg market growth is restrained by the high capital investment and processing costs associated with prepreg manufacturing. Producing prepregs requires specialized equipment, controlled production environments, and precise resin impregnation processes to ensure consistent material quality. In addition, downstream manufacturing often relies on energy-intensive curing methods, such as autoclaves, increasing production costs and limiting adoption among cost-sensitive industries.

According to the U.S. Department of Energy's Oak Ridge National Laboratory (ORNL), autoclave processing for aerospace-grade composites requires temperatures of approximately 120–180°C and pressures of 85–700 kPa (12–100 psi) to achieve high-quality laminates. These specialized processing conditions contribute to higher manufacturing and capital costs for prepreg components.

Cold Chain Logistics and Limited Shelf Life

The prepreg market growth is challenged by the need for refrigerated storage and transportation, along with the limited shelf life of prepreg materials. Most thermoset prepregs require continuous cold-chain logistics to prevent premature resin curing and maintain material performance. These storage and handling requirements increase logistics costs, complicate inventory management, and can lead to material waste if the allowable storage or out-life is exceeded.

According to Hexcel, most aerospace prepregs require continuous freezer storage at approximately −18°C until use, and each prepreg system has a specified out-life at ambient conditions. Exceeding the allowable out-life can degrade processing characteristics and mechanical performance, increasing the risk of material scrap and production delays.

Advancements in Out-of-Autoclave Processing and Manufacturing Automation

The prepreg market trend is shifting toward out-of-autoclave (OOA) processing and automated composite manufacturing to improve production efficiency and reduce costs. OOA prepregs eliminate the need for expensive autoclave curing in many applications, while automation technologies, such as automated fiber placement (AFP) and automated tape laying (ATL), enhance manufacturing precision, reduce material waste, and support higher production rates across aerospace, automotive, and industrial applications.

According to NASA's Hi-Rate Composite Aircraft Manufacturing (HiCAM) project (2025), advanced out-of-autoclave manufacturing technologies are being developed with the goal of increasing composite primary structure manufacturing rates by 4–6 times compared with current production methods, creating significant opportunities for prepreg systems compatible with high-rate production.

Additionally, it also demonstrated high-rate automated fiber placement (AFP) of thermoplastic composites at a layup speed of 0.76 m/s (1,800 in./min.), highlighting the potential of automated composite manufacturing to improve production efficiency while supporting greater adoption of prepreg materials.

Expanding Applications in Electric Mobility and Advanced Air Mobility

The prepreg market trend is creating significant opportunities in electric mobility and advanced air mobility (AAM), including electric vehicles (EVs), eVTOL aircraft, and unmanned aerial vehicles (UAVs). These platforms require lightweight, high-strength composite structures to maximize energy efficiency, extend battery range, and improve payload capacity. As a result, carbon fiber prepregs are increasingly being adopted for airframes, battery enclosures, rotor blades, and structural components.

According to the U.S. Department of Energy, reducing a vehicle's weight by 10% can improve fuel economy by approximately 6%–8%. For battery-electric vehicles, lightweight composite structures also help extend driving range and improve overall energy efficiency, supporting the adoption of prepregs in structural automotive applications.

\

Get Insights On High-Growth Segments. Get Free Sample Here.

“Aerospace & Defense is expected to remain the largest and fastest-growing end-use industry in the prepreg market throughout the forecast period.”

The prepreg market is segmented into aerospace & defense, wind energy, sporting goods, automotive, civil engineering, marine, and other industries. Among these, Aerospace & Defense dominates the market owing to its extensive use of lightweight, high-performance composite materials in both commercial and military aircraft. Prepregs offer an exceptional combination of high strength-to-weight ratio, superior mechanical performance, excellent fatigue resistance, and precise fiber-resin consistency, making them the preferred material for manufacturing critical structural components such as wings, fuselage sections, empennages, engine nacelles, control surfaces, and aircraft interiors.

The segment's leadership is further reinforced by the continued increase in global aircraft production, record commercial aircraft order backlogs, and rising defense expenditures aimed at modernizing military fleets. Additionally, the growing adoption of composite-intensive aircraft designs, coupled with ongoing advancements in automated composite manufacturing technologies and next-generation prepreg systems, is further expanding the use of prepregs across commercial aviation, defense, and space applications.

“Commercial Aircraft is expected to retain its dominance in the prepreg market, while Urban Air Mobility (UAM) is projected to witness the fastest growth during the forecast period.”

The Commercial Aircraft category is expected to remain the largest consumer of prepregs throughout the forecast period, primarily driven by the sustained recovery and expansion of global air travel, record aircraft order backlogs, and increasing production rates by major aircraft manufacturers. Modern commercial aircraft extensively utilize carbon fiber prepregs in primary and secondary structures, including wings, fuselage sections, empennages, engine nacelles, and control surfaces, to reduce weight, improve fuel efficiency, and enhance structural performance. Furthermore, the industry's continued transition toward composite-intensive aircraft platforms and ongoing fleet modernization programs are expected to support robust demand for aerospace-grade prepregs over the coming years.

Meanwhile, the Urban Air Mobility (UAM) category is anticipated to register the fastest growth during the forecast period. The rapid development of electric vertical take-off and landing (eVTOL) aircraft, air taxis, cargo drones, and other advanced air mobility platforms is creating significant demand for lightweight, high-strength composite materials. In addition, increasing investments from aerospace OEMs, startups, and government agencies, coupled with advancements in composite manufacturing technologies and certification activities, are expected to accelerate the commercialization of UAM platforms, making this the fastest-growing aerospace sub-segment for prepreg consumption.

“Thermoset prepregs are expected to remain the dominant resin type, while thermoplastic prepregs are projected to witness the fastest growth during the forecast period.”

Thermoset prepregs, particularly epoxy prepregs, are expected to maintain their dominant position in the global prepreg market due to their proven performance, high reliability, and extensive qualification across aerospace & defense applications. Epoxy prepregs offer an excellent combination of high mechanical strength, outstanding fatigue and corrosion resistance, superior adhesion, low shrinkage, and excellent dimensional stability, making them ideal for manufacturing primary aircraft structures such as wings, fuselage sections, empennages, engine nacelles, and control surfaces. Their widespread adoption in aerospace, sporting goods, marine, and industrial applications is expected to sustain their market leadership throughout the forecast period.

Meanwhile, thermoplastic prepregs, led by PEEK (Polyether Ether Ketone) prepregs, are anticipated to register the highest growth during the forecast period. PEEK prepregs offer several advantages over conventional thermoset systems, including faster processing cycles, excellent toughness and impact resistance, superior chemical and wear resistance, high-temperature performance, and the ability to be welded, reshaped, and recycled.

“Carbon fiber prepreg remains the dominant category by fiber type and is also witnessing the fastest growth in the prepreg market globally.”

Carbon fiber prepregs are expected to dominate the global prepreg market owing to their exceptional strength-to-weight ratio, high stiffness, excellent fatigue resistance, superior corrosion resistance, and outstanding dimensional stability. These properties make them the preferred material for manufacturing lightweight, high-performance structural components across aerospace & defense, automotive, sporting goods, marine, and industrial applications. In the aerospace sector, carbon fiber prepregs are extensively used in primary aircraft structures such as wings, fuselage sections, empennages, engine nacelles, and control surfaces, where reducing weight while maintaining structural integrity is critical for improving fuel efficiency, increasing payload capacity, and lowering operating costs.

Carbon fiber prepregs are also expected to witness the fastest growth during the forecast period, driven by the increasing production of commercial and military aircraft, rising defense modernization programs, and the growing adoption of lightweight composites in electric vehicles, urban air mobility (UAM) platforms, and high-performance industrial applications.

“Autoclave curing is expected to remain the dominant process type, while Out-of-Autoclave (OoA) processing is projected to register the fastest growth in the global prepreg market during the forecast period.”

Autoclave curing is expected to retain its dominant position in the prepreg market due to its ability to consistently produce high-quality composite components with superior mechanical properties, excellent fiber consolidation, low void content, and exceptional dimensional accuracy. The process has long been the industry standard for manufacturing critical aerospace and defense structures, where stringent certification, safety, and performance requirements demand the highest levels of product quality and reliability.

Meanwhile, Out-of-Autoclave (OoA) processing is expected to witness the fastest growth during the forecast period as manufacturers seek to reduce production costs, shorten manufacturing cycle times, and improve production flexibility. OoA technologies eliminate the need for expensive autoclave equipment while enabling the production of high-quality composite parts using vacuum bag-only curing or other low-pressure processes.

“North America is projected to lead the prepreg market in terms of market share and is expected to register the fastest growth during the forecast period.”

North America is expected to maintain its leadership in the global prepreg market, supported by its well-established aerospace and defense ecosystem, the presence of leading aircraft OEMs and composite manufacturers, and continuous investments in advanced composite technologies. The region is home to major industry participants, including Boeing, Lockheed Martin, Northrop Grumman, RTX, Hexcel, and Toray Advanced Composites, which collectively generate substantial demand for high-performance prepregs.

North America is also projected to witness the fastest market growth owing to rising defense expenditure, expanding production of next-generation commercial and military aircraft, and increasing investments in advanced air mobility (AAM), urban air mobility (UAM), and space exploration programs.

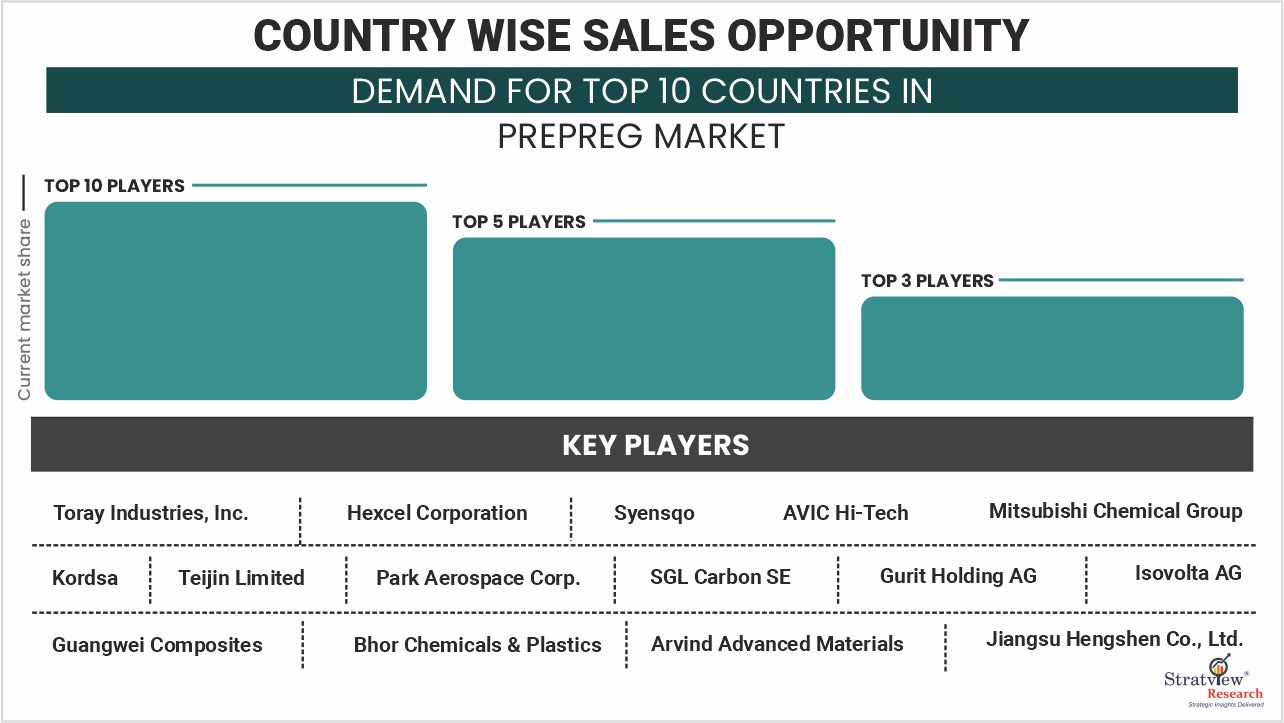

“The study indicates that over 90% of the global prepreg market is concentrated within the top 10 countries, reflecting the industry's strong alignment with aerospace & defense manufacturing ecosystems, robust composite supply chains, significant R&D investments, and high-value advanced manufacturing capabilities.”

Speak To Us For Deep-Diving Into A Country/Region-Specific Opportunity. Contact Us Here

The market is concentrated, with fewer than 50 global and regional players. Leading players hold excellent market positions with a vast product portfolio, a wide distribution network, and years of track record.

The following are the key players in the prepreg market.

Toray Industries, Inc.

Hexcel Corporation

Syensqo

AVIC Hi-Tech

Mitsubishi Chemical Group

Kordsa

Teijin Limited

Park Aerospace Corp.

SGL Carbon SE

Gurit Holding AG

Isovolta AG

Guangwei Composites

Bhor Chemicals & Plastics

Arvind Advanced Materials

Jiangsu Hengshen Co., Ltd.

Note: The above list is not an exhaustive list of the key players in the market. If your company is active in this market and would like to be considered for inclusion in future editions of this study, please contact us at [email protected].

Have The Competitive Edge With Our Intelligence. Get Free Sample Here

Recent mergers & acquisitions and other developments in the prepreg market reflect evolving market trends and impact the market. Below are a few recent developments in the market –

In 2025, Syensqo and Terma formed a strategic partnership to integrate Syensqo's advanced adhesives, composite materials, and specialty polymers into Terma's aerospace and defense systems.

In 2025, Syensqo expanded its collaboration with Boeing to jointly develop next-generation aerospace composite materials and advanced prepreg technologies for future aircraft platforms.

In June 2025, Hexcel Corporation and Kongsberg Defence & Aerospace signed a five-year partnership agreement for the supply of HexWeb® engineered honeycombs and HexPly® prepregs for advanced defense and aerospace applications.

Prepregs (pre-impregnated composites) are advanced composite materials consisting of continuous reinforcement fibers, such as carbon fiber, glass fiber, or aramid fiber, that are pre-impregnated with a precisely controlled amount of thermoset or thermoplastic resin. These engineered materials are supplied in a partially cured (B-stage) or fully consolidated state, enabling manufacturers to produce lightweight, high-strength composite components with exceptional consistency and performance. Prepregs are extensively used in aerospace & defense, automotive, sporting goods, marine, civil engineering, and industrial applications where superior mechanical properties, dimensional accuracy, fatigue resistance, and structural reliability are critical.

Prepregs offer a unique combination of high strength-to-weight ratio, excellent fiber-resin uniformity, superior fatigue and corrosion resistance, low void content, and outstanding processability, making them the preferred material for manufacturing high-performance structural components. Their compatibility with advanced manufacturing technologies, including autoclave curing, automated fiber placement (AFP), automated tape laying (ATL), and out-of-autoclave (OoA) processing, enables the production of complex composite structures with enhanced quality and manufacturing efficiency.

This report provides the most comprehensive market intelligence. The report structure has been kept so that it offers maximum business value. It provides critical insights into market dynamics and will enable strategic decision-making for existing market players and those looking to enter the market.

The following are the key features of the report:

Market structure: Overview, industry life cycle analysis, supply chain analysis.

Market environment analysis: Growth drivers and constraints, Porter’s five forces analysis, SWOT analysis.

Market trend and forecast analysis.

Market segment trend and forecast.

Competitive landscape and dynamics: Market share, Service portfolio, New Product Launches, etc.

Attractive market segments and associated growth opportunities.

Emerging trends.

Strategic growth opportunities for the existing and new players.

Key success factors.

|

Market Study Period |

2020-2031 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2031 |

|

Trend Period |

2020-2025 |

|

Number of Tables & Figures |

50+ |

|

Number of Segments Analyzed |

8 (End-Use Industry, Aerospace & Defense Sub-Type, Commercial Aircraft Structure-Type, Resin Type, Fiber Type, Form Type, Process Type, and Region) |

|

Number of Regions Analyzed |

4 (North America, Europe, Asia-Pacific, Rest of the World) |

|

Countries Analysed |

10+ (The USA, Canada, Mexico, Germany, France, The UK, Russia, China, Japan, India, Brazil, Saudi Arabia, and Rest of the World) |

|

Free Customization Offered |

10% |

|

After Sales Support |

Unlimited |

|

Report Presentation |

Complimentary |

|

Market Dataset |

Complimentary |

|

Further Deep Dive & Consulting Services |

10% Discount |

Want A Report Tailor-Made To Your Objectives? Speak With Our Analyst At [email protected]

The report provides detailed insights into market dynamics to enable informed business decision-making and the formulation of growth strategies based on market opportunities.

The prepreg market is segmented into the following categories:

Prepreg Market, By End-Use Industry Type

Aerospace & Defense

Wind Energy

Sporting Goods

Automotive

Civil Engineering

Marine

Other End-Use Industries

Prepreg Market, By Aerospace & Defense Sub-Type

Commercial Aircraft

Business Jets

Helicopter

Defense

Engine

Space

UAM

Prepreg Market, By Commercial Aircraft Structure Type

Primary Structure

Secondary Structure

Prepreg Market, By Resin Type

Thermoset Prepreg

Epoxy Prepreg

Phenolic Prepreg

BMI Prepreg

Cyanate Ester Prepreg

Other Thermoset Prepregs

Thermoplastic Prepreg

PPS Prepreg

PEEK Prepreg

Other Thermoplastic Prepregs

Prepreg Market, By Fiber Type

Carbon Fiber Prepreg

Glass Fiber Prepreg

Aramid Fiber Prepreg

Prepreg Market, By Form Type

UD Prepreg

Fabric Prepreg

Prepreg Market, By Process Type

Autoclave

Out-of-Autoclave

Other Processes

Prepreg Market, By Region

North America (Country Analysis: The USA, Canada, and Mexico)

Europe (Country Analysis: Germany, France, The UK, Russia, and the Rest of Europe)

Asia-Pacific (Country Analysis: Japan, China, India, and Rest of Asia-Pacific)

Rest of the World (Country Analysis: Brazil, Saudi Arabia, and Others)

Looking For A Deep Dive? Speak with Our Analyst At [email protected]

This strategic assessment report from Stratview Research provides a comprehensive analysis that reflects today’s prepreg market realities and future market possibilities for the forecast period.

The report segments and analyzes the market in the most detailed manner to provide a panoramic view. The vital data/information provided in the report can play a crucial role for market participants and investors in identifying low-hanging fruit in the market and formulating growth strategies to expedite their growth.

This report offers high-quality insights and is the outcome of a detailed research methodology comprising extensive secondary research, rigorous primary interviews with industry stakeholders, and validation and triangulation with Stratview Research’s internal database and statistical tools.

More than 1,000 authenticated secondary sources, such as company annual reports, fact books, press releases, journals, investor presentations, white papers, patents, and articles, have been leveraged to gather the data.

We conducted more than 50 detailed primary interviews with market players across the value chain in all four regions, as well as with industry experts, to obtain both qualitative and quantitative insights.

With this detailed report, Stratview Research offers one of the following free customization options to our respected clients:

Company Profiling

Detailed profiling of additional market players (up to three players)

SWOT analysis of key players (up to three players)

Competitive Benchmarking

Benchmarking of key players on the following parameters: Service portfolio, geographical reach, regional presence, and strategic alliances

Custom Research: Stratview Research offers custom research services across industries. In case of any custom research requirement related to market assessment, competitive benchmarking, sourcing and procurement, target screening, and others, please send your inquiry to [email protected]

The report is delivered digitally through our online portal. Buyers receive login credentials from our team to access the report and may update their credentials at any time after the initial login.

Delivery timelines depend on the status of the report:

For the most accurate delivery timeline, please contact us to confirm the current status of the report.

Yes. You may request a complimentary preview of the report through a video conference with our team.

Yes. The scope of the report can be fully customized to align with your specific research objectives and information requirements.

Please contact us at [email protected], and our team will be happy to discuss your requirements and propose a tailored solution.

Yes. Selected sections of the report can be purchased separately based on your requirements. Please contact us at [email protected] to discuss your needs.

Yes, AI can help gather publicly available information, but its outputs are only as reliable as the data it accesses. Stratview Research reports are built using validated data, extensive primary interviews with industry stakeholders, and the expertise of our experienced research team.

Additionally, many critical insights, including market dynamics, competitive intelligence, and industry-specific trends, are not publicly available and therefore cannot be captured through AI alone.

Prepreg market size was USD 5.1 billion in 2025. The market is expected to grow from USD 5.9 billion in 2026 to USD 8.1 billion in 2031, witnessing a decent market growth (CAGR) of 6.5% during the forecast period (2026-2031).

The forecasted value of the prepreg market is USD 8.1 billion in 2031.

The Aerospace & Defense is the leading end-use industry in the global prepreg market, due to the extensive use of prepregs in commercial aircraft, military aircraft, helicopters, UAVs, and spacecraft. Prepregs provide an exceptional combination of lightweight properties, high strength-to-weight ratio, superior fatigue resistance, dimensional stability, and consistent mechanical performance, making them the preferred material for manufacturing critical structural components such as wings, fuselage sections, empennages, engine nacelles, and control surfaces.

Celanese Corporation, Gurit Holdings, AG, Hexcel Corporation, Mitsubishi Chemical Carbon Fiber and Composites, Inc. (MCCFC), Park Electrochemical Corp., SGL Group SE, Solvay S.A., Teijin Group, and Toray Industries, Inc. are among the key players in the market.

WE ACCEPT