404

+1-313-307-4176

Insulation Market Growth Analysis | 2026-2034

Insulation Market Size, Share, Trend, Forecast, Competitive Landscape & Growth Opportunities: 2026-2034

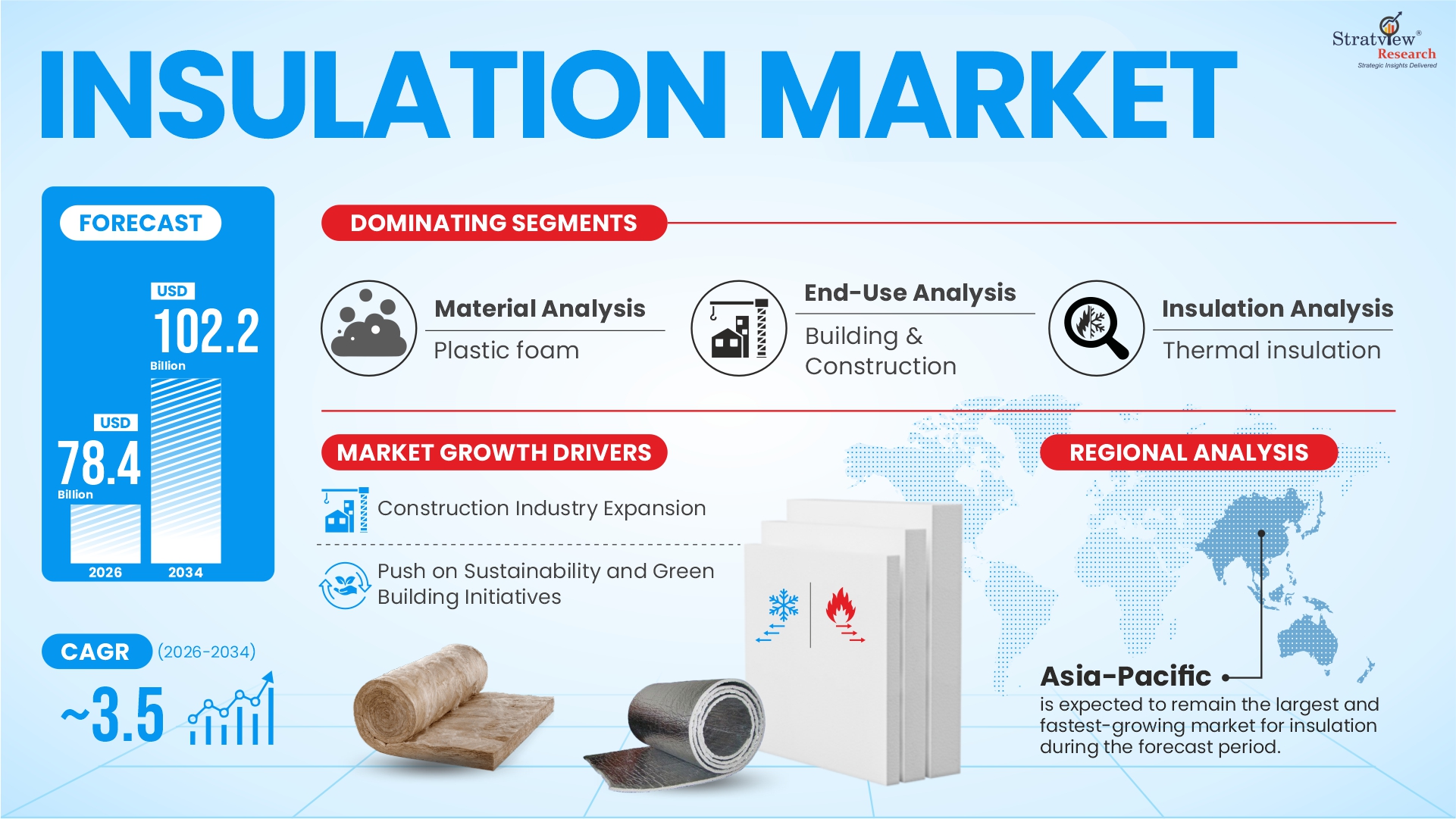

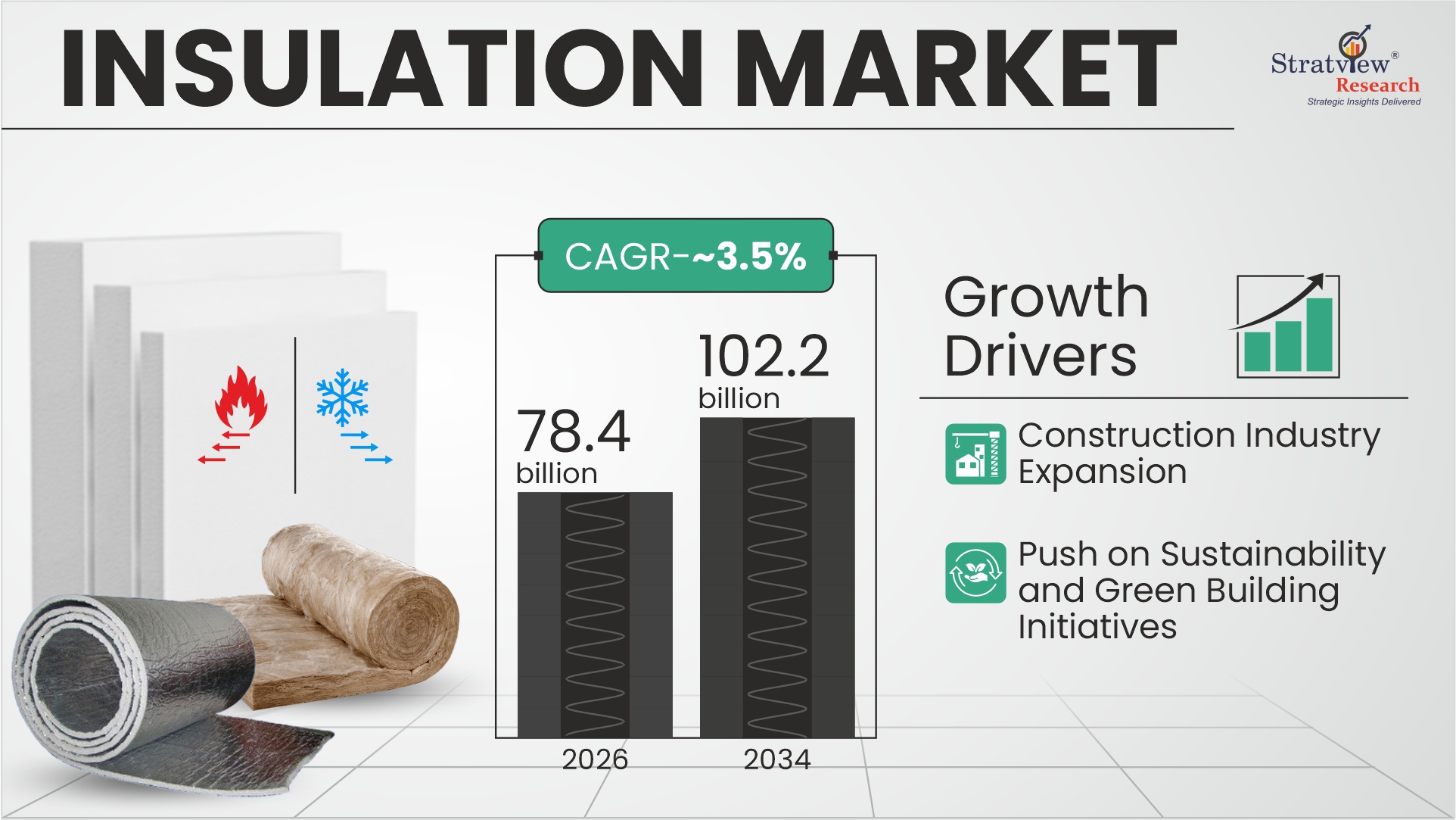

The annual demand for insulation was USD 75.7 billion in 2025 and is expected to reach USD 78.4 billion in 2026, reflecting a year-over-year (YoY) growth of 3.2% compared with 2025.

During the forecast period (2026-2034), the insulation market is expected to grow at a CAGR of 3.4%. The annual demand will reach USD 102.2 billion in 2034.

During 2026-2034, the insulation industry is expected to generate a cumulative sales opportunity of USD 812.3 billion.

Want to get a free sample? Register Here

Asia-Pacific is expected to dominate the market during the forecast period.

By material type, plastic foam is expected to remain the largest material type in the market during the forecast period.

By end-use type, building & construction is expected to remain the dominant and fastest-growing end-use type in the market during the forecast period.

By insulation type, thermal insulation is projected to remain the dominant insulation type in the market over the upcoming years.

Have a look at the sales opportunities presented by the insulation market in terms of growth and market forecast.

|

Insulation Market Data & Statistics |

||

|

Market Statistics |

Value (in USD Billion) |

Market Growth (%) |

|

Annual Market Size in 2024 |

USD 73.3 billion |

- |

|

Annual Market Size in 2025 |

USD 75.7 billion |

YoY Growth in 2025: 3.6% |

|

Annual Market Size in 2026 |

USD 78.4 billion |

YoY Growth in 2026: 3.2% |

|

Annual Market Size in 2034 |

USD 102.2 billion |

CAGR 2026-2034: 3.4% |

|

Cumulative Sales Opportunity during 2026-2034 |

USD 812.3 billion |

- |

|

Top 10 Countries’ Market Share in 2025 |

USD 60.6 billion+ |

> 80% |

|

Top 10 Companies’ Market Share in 2025 |

USD 37.8 billion - USD 53.0 billion |

50% - 70% |

Insulation refers to materials used to reduce heat transfer and control sound transmission, improving energy efficiency, indoor comfort, and operational performance across buildings and industrial systems. By limiting thermal exchange and noise propagation, insulation reduces reliance on heating and cooling systems while enhancing acoustic performance.

Insulation materials are widely used across residential buildings, commercial infrastructure, industrial equipment, and cold chain systems, driven by increasing focus on energy efficiency, thermal comfort, noise control, and emission reduction. Governments and regulatory bodies are integrating insulation into building energy codes and sustainability frameworks, positioning it as a core component of modern infrastructure development.

Want to get a free sample? Register Here

Construction Industry Expansion

The expansion of the global construction sector is a key driver for the insulation market, as insulation is a critical component in building envelopes for energy efficiency, thermal performance, and regulatory compliance. Rising investments in residential housing, commercial infrastructure, and urban development projects are directly increasing demand for insulation materials.

According to the World Economic Forum, the global building floor area is expected to double by 2060, adding the equivalent of a city the size of New York every month. This rapid expansion is structurally increasing demand for insulation materials, particularly as energy efficiency becomes a mandatory requirement in new construction.

In parallel, government-led infrastructure programs and smart city initiatives across the Asia-Pacific and the Middle East are accelerating construction activity. This is positioning insulation as a baseline requirement rather than an optional material, as building codes increasingly mandate energy-efficient and low-emission construction practices.

Sustainability and Green Building Initiatives Accelerating Insulation Adoption

The decarbonization push in the built environment is also one of the key growth drivers, with the United Nations Environment Programme reporting 32% of global energy use and 34% of CO₂ emissions from buildings, driving demand for energy-efficient insulation solutions.

Governments are enforcing energy efficiency regulations and net-zero building targets, making insulation a critical requirement to reduce HVAC energy demand and improve thermal performance.

The adoption of frameworks like Leadership in Energy and Environmental Design (LEED) and Building Research Establishment Environmental Assessment Method (BREEAM) is accelerating demand for high-performance insulation, increasing its usage across modern construction projects.

Adoption of Advanced High-Performance Insulation Materials

Advanced insulation materials such as aerogels, vacuum insulation panels (VIPs), and phase-change materials (PCMs) are emerging as a key growth opportunity in the insulation market, driven by their ultra-low thermal conductivity (~0.01–0.02 W/mK for aerogels). This enables superior thermal performance in space-constrained applications, accelerating demand across high-performance insulation segments, including advanced buildings and industrial systems.

The growing need for energy-efficient and compact system design is driving the adoption of these materials across high-value applications. Their ability to minimize heat transfer, improve thermal stability, and optimize system efficiency makes them critical in sectors such as energy-efficient construction, cold chain logistics, and advanced industrial processes, positioning them as a premium, technology-driven segment supporting insulation market growth during the upcoming years.

|

Segmentations |

List of Sub-segments |

Dominant/Fastest Growing Segment |

|

Material Analysis |

Fiberglass, Mineral Wool, Plastic Foam, and Others |

Plastic foam is expected to remain the largest material type in the market during the forecast period. |

|

End-Use Analysis |

Building & Construction and Industrial |

Building & Construction is expected to remain the dominant and fastest-growing end-use type in the market during the forecast period. |

|

Insulation Analysis |

Thermal and Acoustic |

Thermal insulation is projected to remain the dominant insulation type in the market over the upcoming years. |

|

Regional Analysis |

North America, Europe, Asia-Pacific, and the Rest of the World. |

Asia-Pacific is expected to remain the largest and fastest-growing market for insulation during the forecast period. |

"Plastic Foam Insulation Continues to Dominate Due to Superior Thermal Efficiency and Versatility."

Based on material type, the insulation market is segmented into fiberglass, mineral wool, plastic foam, and other materials. Among these, plastic foam insulation accounts for the largest market share and is expected to maintain its leadership throughout the forecast period due to its high R-value (thermal resistance), low thermal conductivity, and strong moisture resistance.

Plastic foam materials such as expanded polystyrene (EPS), extruded polystyrene (XPS), and polyurethane (PU) foam are widely used across residential, commercial, and industrial applications. Their lightweight structure, durability, and ease of installation make them highly suitable for energy-efficient building insulation systems.

Among these, expanded polystyrene (EPS) is projected to remain the leading sub-segment due to its wide availability, recyclability, and consistent performance in wall insulation, roofing systems, and foundation applications. The growing demand for high-performance insulation materials and sustainable construction solutions continues to support this segment.

Want to get more details about the segmentations? Register Here

"Building & Construction Remains the Primary Demand Center, Driven by Energy-Efficient Infrastructure Development."

Based on end-use type, the insulation market is segmented into building & construction and industrial applications. The building & construction segment dominates the market and is expected to remain the fastest-growing segment during the forecast period, driven by rising investments in residential housing, commercial infrastructure, and urban development projects.

Demand growth is supported by the increasing need for energy-efficient buildings, thermal insulation systems, and acoustic insulation solutions. Governments are implementing stricter building energy codes and green building standards, accelerating the adoption of advanced insulation materials.

Additionally, the trend of retrofitting existing buildings and the rising focus on indoor thermal comfort and noise reduction are boosting insulation demand. The integration across walls, roofs, HVAC systems, and flooring applications further strengthens long-term growth.

"Thermal Insulation Leads the Market, Supported by Global Energy Efficiency and Decarbonization Goals."

Based on insulation type, the market is segmented into thermal and acoustic insulation. Thermal insulation holds the largest share and is expected to maintain its dominance due to its role in reducing heat transfer, improving energy efficiency, and lowering energy consumption.

The increasing focus on climate change mitigation, carbon emission reduction, and sustainable construction is significantly driving demand for thermal insulation materials. In addition, regulatory frameworks and building energy performance standards are supporting the adoption of high-performance insulation solutions.

Thermal insulation is widely used across walls, roofs, pipelines, industrial equipment, and cold storage systems, making it essential across industries. The adoption of advanced materials with improved fire resistance and durability continues to enhance this segment.

Want to get more details about the segmentations? Register Here

"Asia-Pacific Leads the Global Insulation Market, Driven by Rapid Urbanization and Infrastructure Expansion."

Asia-Pacific holds the largest share in the insulation market and is expected to remain the fastest-growing region during the forecast period. Growth is driven by rapid urbanization, expanding construction activities, and infrastructure investments in emerging economies such as China and India.

China leads the regional market due to its large-scale construction sector, strong manufacturing base, and energy-efficient building regulations. Increasing investments in industrial insulation, transportation infrastructure, and smart city initiatives are further supporting demand.

Europe represents another key market, driven by strong regulatory frameworks, high adoption of green building technologies, and growing demand for sustainable insulation materials. Countries such as Germany, France, and the United Kingdom are leading this transition.

Most of the major players compete in some of the factors, including price, service offerings, and regional presence, etc. The following are the key players in the insulation market–

Owens Corning

Rockwool International

BASF SE

Kingspan Group

Note: The above list does not necessarily include all the top players in the market.

Are you a leading player in this market? We would love to include your name. Please write to us at [email protected]

This report provides market intelligence most comprehensively. The report structure has been kept so that it offers maximum business value. It provides critical insights into market dynamics and will enable strategic decision-making for existing market players as well as those willing to enter the market.

The following are the key features of the report:

Market structure: Overview, industry life cycle analysis, supply chain analysis.

Market environment analysis: Growth drivers and constraints, Porter’s five forces analysis, SWOT analysis.

Market trend and forecast analysis.

Market segment trend and forecast.

Competitive landscape and dynamics: Market share, Service portfolio, New Product Launches, etc.

COVID-19 impact and its recovery curve.

Attractive market segments and associated growth opportunities.

Emerging trends.

Strategic growth opportunities for the existing and new players.

Key success factors.

|

Market Study Period |

2019-2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Trend Period |

2019-2024 |

|

Number of Tables & Figures |

>100 |

|

Number of Segments Analysed |

4 (Material Type, End-Use Type, Insulation Type, and Region) |

|

Number of Regions Analysed |

4 (North America, Europe, Asia-Pacific, Rest of the World) |

|

Countries Analysed |

15 (The USA, Canada, Mexico, Germany, France, Italy, The UK, China, Japan, India, Brazil, Saudi Arabia, Rest of Europe, Rest of APAC, and Rest of the World) |

|

Free Customization Offered |

10% |

|

After Sales Support |

Unlimited |

|

Report Presentation |

Complimentary |

|

Market Dataset |

Complimentary |

|

Further Deep Dive & Consulting Services |

10% Discount |

The report provides detailed insights into the market dynamics to enable informed business decision-making and growth strategy formulation based on the opportunities present in the market.

The insulation market is segmented into the following categories:

By Material Type

Fiberglass

Mineral Wool

Plastic Foam

Others

By End-Use Type

Building & Construction

Industrial

By Insulation Type

Thermal

Acoustic

By Region

North America (Country Analysis: The USA and Others)

Europe (Country Analysis: Central Europe, Western Europe, and Eastern Europe)

Asia-Pacific (Country Analysis: China and Others)

Rest of the World (Country Analysis: The Middle East, Latin America, and Others)

This strategic assessment report provides a comprehensive analysis that reflects today’s insulation market realities and future market possibilities for the forecast period.

The report segments and analyzes the market in the most detailed manner to provide a panoramic view of the market.

This report offers high-quality insights and is the outcome of a detailed research methodology comprising extensive secondary research, rigorous primary interviews with industry stakeholders, and validation with internal databases and statistical tools.

More than 1,000 authenticated secondary sources, including company annual reports, industry publications, press releases, journals, and technical papers, were used to gather data.

Primary interviews were conducted with market participants across the value chain, including OEMs, suppliers, distributors, and industry experts to obtain both qualitative and quantitative insights.

With this detailed report, Stratview Research offers one of the following free customization options to our respectable clients:

Company Profiling

Competitive Benchmarking

Custom Research: Stratview Research offers custom research services across sectors. In case of any custom research requirement related to market assessment, competitive benchmarking, sourcing and procurement, target screening, and others, please send your inquiry to [email protected].

The global insulation market is estimated at USD ~16–18 billion in 2025 and is projected to reach USD ~22–25 billion by 2030, growing at a CAGR of ~3–5%. Growth is supported by expanding construction activity, rising retrofit demand, and increasing regulatory focus on energy-efficient buildings across major economies.

Asia-Pacific leads the global insulation market, driven by rapid urbanization, large-scale infrastructure development, and strong construction activity in countries such as China and India. Increasing government investments and the growing need for energy-efficient buildings further support regional market growth.

Key advancements include aerogels, vacuum insulation panels (VIPs), and phase-change materials (PCMs), which offer significantly lower thermal conductivity compared to conventional materials. These materials are increasingly used in high-performance buildings, cold chain logistics, and electric vehicle thermal management systems, where space efficiency and thermal performance are critical.

The insulation market is primarily driven by construction sector expansion, rapid urbanization, and stringent energy efficiency regulations. Sustainability initiatives are also accelerating adoption, as the United Nations Environment Programme highlights that buildings account for 32% of global energy consumption and 34% of CO? emissions, making insulation critical for reducing overall energy demand.

The building and construction sector dominates insulation demand, driven by residential and commercial infrastructure development. Industrial applications, including oil & gas, power generation, and manufacturing, also contribute significantly due to the need for thermal efficiency, process stability, and energy conservation.

Energy efficiency regulations are making insulation a mandatory component in modern construction practices. Certification frameworks such as Leadership in Energy and Environmental Design and Building Research Establishment Environmental Assessment Method are accelerating the adoption of high-performance insulation materials, as they directly contribute to improved building ratings and reduced energy consumption.

The future of the insulation market is shaped by advanced high-performance materials, green building adoption, and energy-efficient infrastructure development. Emerging opportunities include aerogel-based insulation, prefabricated construction solutions, circular insulation materials, and smart insulation systems, supporting steady long-term market growth.

Key players in the insulation market include Owens Corning, Saint-Gobain, Rockwool International, Knauf Insulation, BASF SE, and Kingspan Group.

WE ACCEPT