EV Battery Retirement is Now a Core Supply Chain Strategy

The global conversation around electric vehicles has largely focused on adoption rates, battery chemistry innovation, and charging infrastructure. Less attention has been given to what happens after the battery reaches end-of-life.

Yet as the first large wave of electric vehicles approaches retirement cycles, battery disposal is transitioning into a structured material recovery opportunity.

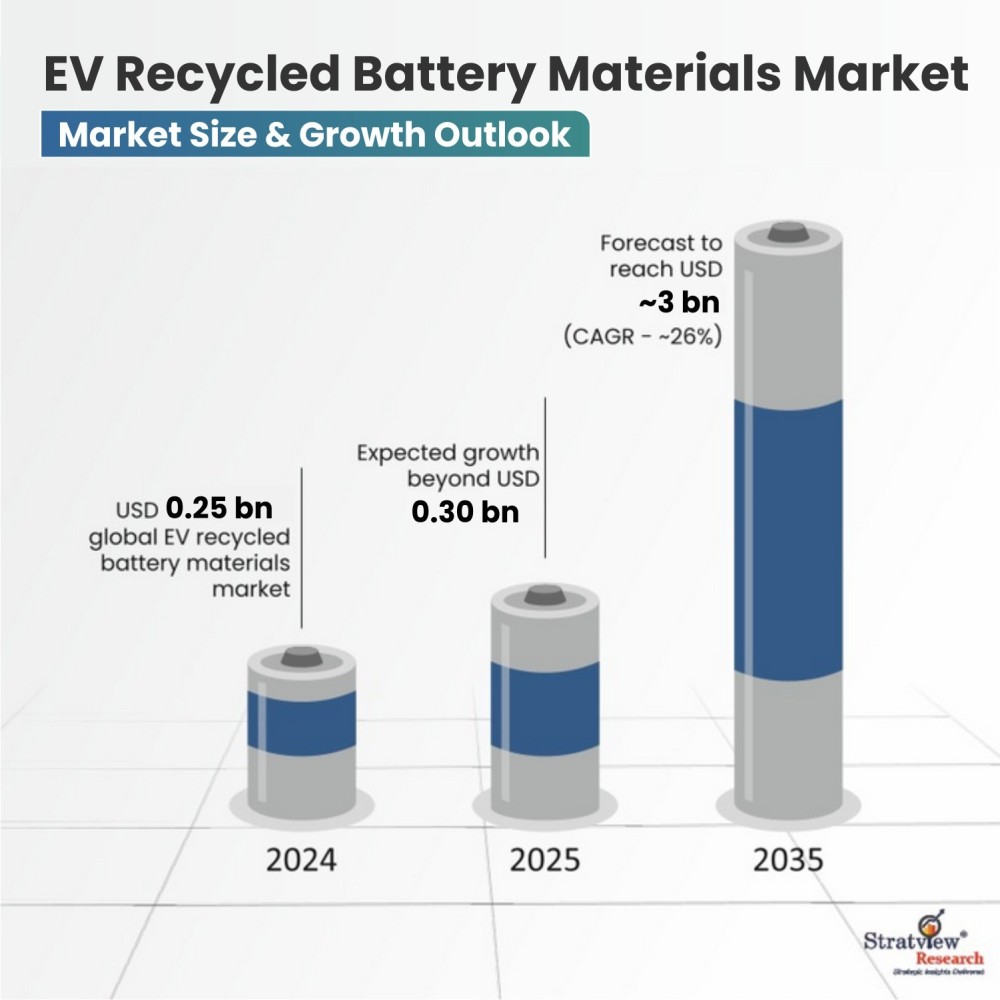

EV Recycled Battery Materials Market Forecast

In 2024, the EV recycled battery materials market stood at approximately USD 0.25 billion. It is projected to exceed USD 3.00+ billion by 2035, expanding at a CAGR of roughly 25–26%. This trajectory reflects the emergence of a secondary raw material channel that is gradually integrating into EV supply planning.

The Material Reserve Already on the Road

A 75 kWh lithium-ion battery pack, such as one used in a Tesla Model 3 configuration, contains roughly 12 kg of lithium, 50 kg of nickel, 4.5 kg of cobalt, 4 kg of manganese, and nearly 70 kg of graphite, along with 20 kg of aluminum and 25 kg of copper. These are not peripheral materials. They directly shape battery cost structures and supply exposure.

Between 2015 and 2023, rapid EV deployment effectively created a distributed reserve of critical minerals embedded within vehicles already in operation. Retirement unlocks that embedded inventory.

Currently, around 97% of batteries entering recycling streams are lithium-ion systems, ensuring chemistry consistency. Approximately 58% originate from passenger vehicles and 41% from electric buses, the latter reflecting higher utilization intensity and earlier replacement cycles.

Economics Will Be Chemistry-Sensitive

Recovered material value is unevenly distributed. Cobalt accounts for roughly 30% of recycled material value, copper about 25%, and lithium approximately 8%. This distribution matters.

TAGS: Automotive