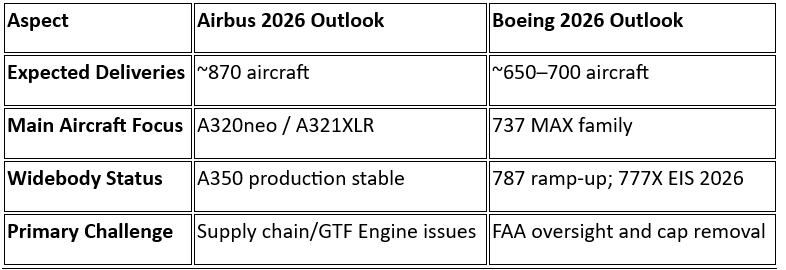

Airbus and Boeing enter 2026 from very different starting points. Airbus carries a record backlog and benefits from stable production of major programs such as the Airbus A350 and the high-volume Airbus A320neo family. This production stability allows the company to concentrate on deliveries, with a target of around 870 commercial aircraft in 2026, following 793 deliveries in 2025.

Boeing, on the other hand, is continuing a multi-year recovery under CEO Kelly Ortberg. The company’s priority remains restoring manufacturing stability and strengthening regulatory confidence after several years of disruption. While deliveries are still constrained, Boeing reclaimed the orders lead in 2025, indicating renewed airline confidence in its aircraft portfolio.

These differing positions become more visible when looking at aircraft deliveries.

Delivery Leadership: Airbus Maintains the Edge

Airbus leads narrowbody production, with the A321XLR now a fully operational asset strengthening long-range single-aisle routes. While Boeing is increasing 737 MAX output, FAA production caps and rigorous oversight continue to moderate the ramp-up.

Industry forecasts suggest Boeing could deliver around 650–700 aircraft in 2026, assuming the FAA lifts current production constraints. This would leave Airbus ahead by roughly 170–200 units. In the widebody segment, A350 production is stable, while Boeing focuses on the 787 Dreamliner ramp-up and the critical 2026 Entry into Service (EIS) for the 777X.

Orders and Deliveries: Two Sides of Market Leadership

Although Airbus leads in deliveries, Boeing’s recent order momentum reflects another important dimension of competition. Deliveries generate immediate revenue and expand airline capacity, while orders influence long-term production plans and market share.

Airbus is currently focused on converting its large backlog into aircraft that enter airline fleets. Boeing, meanwhile, is working to transform new orders into steady production growth without compromising quality or safety standards.

Source: Stratview Research

This comparison shows how the two companies are prioritizing different aspects of the market: Airbus emphasizing delivery output and Boeing concentrating on rebuilding production momentum.

Critical Factors Impacting 2026

Beyond orders and deliveries, several industry conditions will influence how the Airbus–Boeing competition develops in 2026. Certification timelines, supply chain reliability, and geopolitical relationships will all play an important role.

Certification challenges. Boeing continues working toward regulatory approval for the 737 MAX 7, 737 MAX 10, and the delayed 777X. Airbus is dealing with durability issues affecting engines used on part of the A320neo fleet.

Supply chain constraints. Aerospace manufacturers are still facing shortages of raw materials, cabin components, and titanium. Airbus is expanding assembly capacity in Toulouse and Tianjin as part of its longer-term plan to produce up to 75 A320-family aircraft per month by 2027. Boeing is focusing on stabilizing production systems and strengthening quality oversight.

Geopolitical influence. Aircraft purchasing decisions are increasingly connected to trade relations and government partnerships. Boeing has secured several large widebody agreements in the Middle East and Asia, while Airbus continues to benefit from long-standing commercial relationships across Europe and emerging Asian markets.

Quality Over Speed

Across the aviation sector, airlines and manufacturers are placing greater emphasis on reliability and execution. Boeing has repeatedly stressed a culture-focused approach to rebuilding manufacturing discipline, ensuring production increases do not compromise safety. Airbus, despite its current production advantage, must carefully scale output while maintaining supply chain stability.

Airlines are also paying closer attention to delivery reliability when making fleet decisions. Large aircraft orders from carriers such as Air India and Alaska Airlines reflect the need to support sustained travel demand while ensuring dependable aircraft availability.

In this environment, consistent production performance is becoming more important than headline-grabbing order announcements.

Industry Outlook

Together, these developments provide a clearer outlook for the Airbus–Boeing rivalry in 2026.

The rivalry reflects two different phases of the industry cycle. Airbus is benefiting from strong production momentum, while Boeing continues rebuilding its manufacturing base after several challenging years. Airbus currently leads in deliveries, but Boeing’s improving order activity suggests the balance could gradually shift as production strengthens.

Ultimately, the winner of 2026 will be the manufacturer that delivers on time without compromising on the industry's heightened safety standards.

TAGS: avionics