Heat exchangers are becoming essential across modern industries as energy efficiency, waste heat recovery, and emission reduction take center stage. From chemicals and power generation to HVAC and renewables, advanced thermal management systems are driving operational performance. With strong demand from Asia Pacific and rapid technological innovation, the global heat exchanger market is set for steady growth through 2030.

Thermal management has moved from being just a consideration to utmost priority now for a majority of industries across the globe. As energy costs climb, emission targets tighten, and efficiency becomes a competitive advantage, industries worldwide are rethinking how they manage heat. The goal is clear – cut waste, lower carbon impact, and boost performance without compromising reliability or scalability.

This is where heat exchangers come as a support to industrial equipment. From keeping turbines cool in power plants to regulating server temperatures in data centers, and from optimizing chemical processes to enhancing HVAC systems, heat exchangers are quietly but decisively transforming how sectors approach thermal optimization.

Not just by increasing energy demands, but a combination of region-specific adoption patterns, rapid technological advancements, and the diverse applications of different types of heat exchangers across various industrial settings are anchors behind this growth.

Breaking Down Heat Exchanger Variants and Their Dominance

There are a few widely used technologies: plate heat exchangers, shell-and-tube systems, and air-cooled configurations. Each offers a unique balance of efficiency, durability, and application-specific viability.

Plate Heat Exchangers (PHE) have emerged as the go-to solution for industries that demand precision thermal control with minimal spatial footprint. Currently, Gasket Plate & Frame HE, Welded Plate HE, Brazed Plate HE, all three types of PHEs combinedly own over 25% revenue share of the global market, generating ~USD 4.1 billion in 2024. Their dominance reflects a shift toward cleanable, scalable, and thermally agile systems that can keep pace with rapidly evolving process requirements.

Shell-and-Tube Heat Exchangers (STHEs), on the other side, have long been the industry’s trusted workhorse. They are well-suited for power generation, oil refining, chemical production, and marine applications, in short, anywhere thermal efficiency must be delivered under physically taxing conditions. Despite growing competition from compact designs, STHEs maintained a solid ~24% share of global revenue in 2024.

While the above two require water to process, in geographies where water is scarce or regulatory frameworks mandate conservation, air-cooled heat exchangers (ACHEs) offer a compelling alternative. While they tend to require more physical space and command higher up-front capital investment than their liquid-cooled counterparts, their long-term operational savings are considerable. ACHEs represented approximately 23% of market revenues in 2024.

Key Industries Driving Heat Exchangers’ Demand

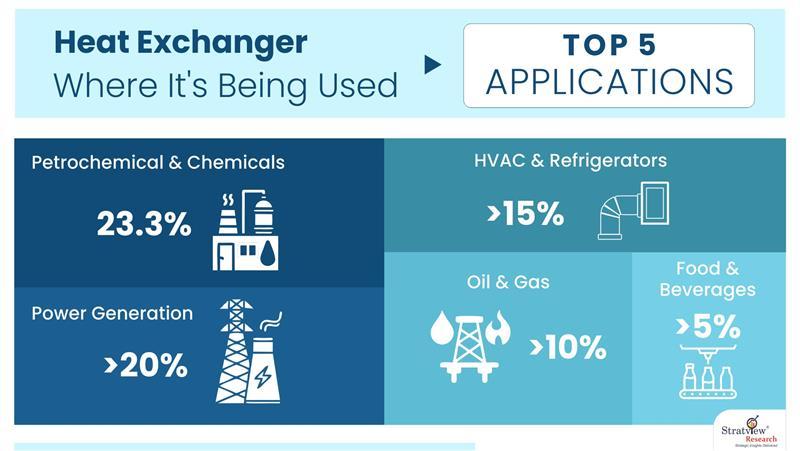

The growing demand for everyday essentials, right from plastics and fertilizers to pharmaceuticals and clean energy materials, is pushing the chemical and petrochemical industries to operate at higher intensity than ever before. In this sector, a reliable heat exchanger works as a backbone. Majority of the global demand for HEs comes from this industry.

The power generation industry isn’t far behind. With the surge in renewables, and advanced thermal cycles, thermal management is under the spotlight. When nearly one-third (32%) of the world’s electricity is now supplied by renewables, their reliance on precise and efficient thermal management becomes even more critical.

Both, Chemicals & petrochemicals and Power generation sector combinedly account for nearly 50% of the total HE requirements globally.

HVAC systems have become standard infrastructure in commercial buildings, data centers, airports, and even homes. Hence, a significant share of HE's demand stems from the HVAC and refrigeration sectors. As energy efficiency regulations tighten, these systems increasingly rely on high-performance heat exchangers to manage thermal loads with minimal energy waste.

Fig 1. Top 5 Applications of Heat Exchangers

The Marine and Shipbuilding industry, Pharmaceuticals, Water and Wastewater Treatment plants, Food and Beverage industry, etc. are a few other end use sectors to name. Though these sectors operate at a smaller scale in terms of HE market’s share, they play a vital role in expanding the application footprint of heat exchangers across a diverse range of use cases.

Geographical Outlook on Heat Exchangers Demand

Asia‑Pacific, with countries such as China, India, Japan, South Korea, has emerged as the epicentre of global heat exchangers’ demand. APAC accounted for >30% of global HE revenues in 2024.

It is no news, that the aforementioned APAC nations lead some major refining, chemical, power and renewable energy projects, all of which rely heavily on robust thermal management systems. As of early 2025, China’s operating solar and wind capacity – alone – has reached 1.4 TW, more than 40% of the global total and more than the combined capacity of the European Union, United States, and India.

China’s industrial sector alone accounts for nearly 70% of the nation’s total energy consumption. What’s more, estimates indicate that 20-30% of the energy used in these industries is lost as waste heat, representing an enormous untapped resource. The nation aims to reduce industrial energy waste by at least 30%, with waste heat recovery expected to prevent 200 million tons of CO₂ emissions annually by 2035. The Chinese government is taking proactive measures to drive heat conservation and recovery initiatives.

India has emerged as a global manufacturing hub and its power sector has expanded rapidly. As per the International Energy Agency (IEA), India posted the fastest electricity-demand growth among major economies, demand rose 7% in 2023 and is expected to grow above 6% on average annually until 2026. The Press Information Bureau (PIB) of India has also reported an increase in electricity generation – from 1,168 BU in 2015–16 to an estimated 1,824 BU in 2024–25.

Japanese government also supports renewable heat and waste‑heat recovery through a 2025 subsidy program for system upgrades. Meanwhile, mega‑renewable projects like Japan’s largest offshore wind farm (Ishikari Bay New Port, 112 MW, commissioned in 2024), and geothermal development using advanced heat‑recovery technology under the New Energy and Industrial Technology Development Organization (NEDO) initiatives are expanding the footprint of infrastructure requiring high‑performance heat‑exchangers.

Taken together – strong demand, higher generation, rapid renewable additions and rising domestic manufacturing, industrial expansion in APAC will increase demand for thermal-management equipment across power plants, manufacturing lines and renewables-adjacent systems.

Though North America and Europe remain significant, APAC’s growth trajectory strengthens its role as the primary driver of future heat‑exchanger demand.

Closing Insights on Heat Exchangers and their Powerful Future

Governments across the globe are mandating tighter energy efficiency norms, such as the EU’s Ecodesign Directive and the U.S. Department of Energy’s performance standards, forcing industries to recover and reuse waste heat. Different sources estimate that energy recovery systems like heat recovery or exchanger setups can save somewhere between 5%-40% of energy consumption across most industrial processes.

Secondly, International Energy Agency (IEA.org) predicts that in 2025, renewables-based electricity generation will overtake coal-fired generation. This surge in renewable energy systems depends heavily on high-efficiency heat transfer equipment to function optimally.

Meanwhile, a few technological advancements, like compact microchannel exchangers, 3D-printed designs, and smart monitoring, etc. are adding power to the performance of heat exchangers, while reducing space and maintenance needs.

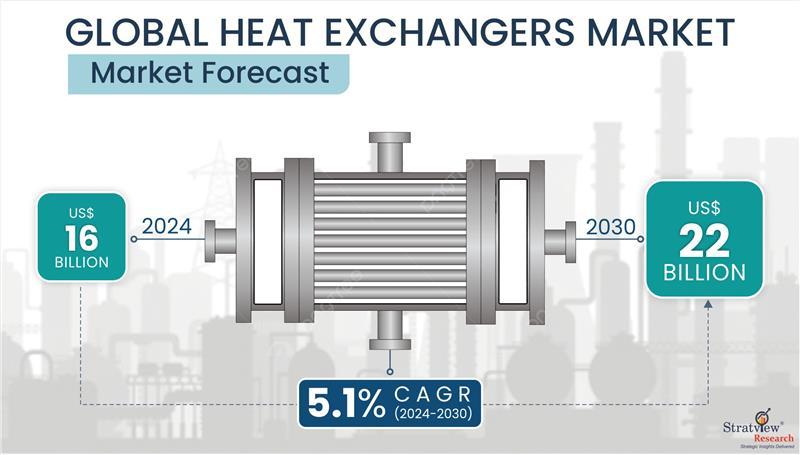

Fig 2. Global Heat Exchangers Market Forecast

All the above factors collectively are driving the demand for advanced heat exchangers. As heavy industries, petrochemical facilities, and power generation infrastructure scale to meet rising global energy and production needs, the global heat exchanger market is projected to expand from ~USD 16 billion in 2024 to USD 22 billion in 2030 growing at a healthy annual rate of >5%.

Subscribe to our newsletter

Related Articles:

The Growing Role of Heat Exchangers

Didn’t find what you were looking for?

Tell us about your requirements

(Our team usually responds within a few hours)