Small satellites are reshaping the global space industry through mega-constellations, rapid miniaturization, and falling launch costs. Driven by players like SpaceX, Amazon, and China’s emerging programs, the sector is expanding across communications, Earth observation, and defense. With rising launches, regulatory shifts, and AI-powered innovation, the small satellite market is poised for sustained growth through 2032.

In recent years, small satellites have transformed the dynamics of the global space industry, opening doors to faster, cheaper, and more flexible access to orbit. These compact spacecraft range in mass from as light as a grapefruit (0.10 kg) to as heavy as a compact car (~1,200 kg), offering significant advantages over traditional satellites including lower costs, faster deployment, and seamless integration into large constellations.

This transformation has been enhanced by the rise of mega-constellations, most notably SpaceX’s Starlink, which has fundamentally reshaped the industry’s growth curve. Small satellites are advancing at an unprecedented pace, redefining how we connect, observe, and understand our world. From accelerating global communications to providing high-resolution Earth monitoring, these satellites are delivering capabilities that were once the exclusive domain of massive spacecraft. Here’s where the small satellite market stands today – and where it’s heading.

From Steady to Skyrocketing – The Speed of Small Sats

The small satellite market posted healthy growth, approx. 25% between 2015 and 2019. But everything changed with the arrival of SpaceX’s Starlink. After launching 397 small satellites in 2018, by 2019 the number rose to 424, with Starlink accounting for 30% of all launches, proving their expertise by deploying dozens of satellites within just two years of their inception. To be precise, by volume, there was a sharp 557% rise in the number of total small satellites launched from 2019 to 2024, with the majority of these launches attributed to Starlink and OneWeb.

As of October 30, 2025, Starlink alone operates over 8,811 satellites, with approximately 8,795 actively functioning in orbit – a figure that surpasses the combined satellite assets of many national space programs.

Apart from being the star of the small satellites industry, Starlink also plans to expand beyond 42,000 units by 2030. The scale and ambition have pushed every major player to reassess their goals.

Amazon’s Project Kuiper, for instance, has moved from promise to performance. Amazon's Project Kuiper is accelerating its satellite deployment, with over 100 satellites now in orbit and plans for > 80 launches to complete its constellation.

Meanwhile, China is asserting its presence. The country has undertaken several ambitious projects, including the Three-Body Computing Constellation, which launched 12 AI-powered satellites in May 2025 to build an orbital supercomputer. Private firm Orienspace marked a milestone in October 2025 by launching 3 small satellites from a floating barge in the Yellow Sea, ground-breaking ocean-based commercial launches. The Shiyan experimental series continues to expand with new test satellites, Shiyan-29 and Shiyan-31, launched in late 2025 for advanced orbital experiments. Additionally, China collaborated with Mexico’s ThumbSat to place two ultra-light satellites into orbit, signaling the nation’s growing participation in international small satellite ventures.

Globally, different analyses predict thousands of small satellites will be launched annually through 2030. For example, as many as 70,000 low earth orbit (LEO) satellites are expected to be launched over the next five years, according to Goldman Sachs. Stratview Research estimates that >19,400 units of small satellites are likely to be installed globally during the 2024-2030 timeframe. SpaceX, OneWeb, and Planet lead the pack.

Amidst this, several other players have laid out ambitious launch plans and strategic initiatives that highlight the dynamic nature of the small satellite sector. Here are a few –

- Rocket Lab Corporation has secured multi-launch contracts with Japanese firms, highlighting the growing demand for commercial satellite launch services.

- Bengaluru-based startup GalaxEye is set to launch ‘Drishti’ in the first quarter of 2026. This is India's largest privately built commercial satellite.

- Thales Alenia Space, in collaboration with Italy's space agency, is set to inaugurate a satellite manufacturing facility near Rome, aiming to produce approximately 100 satellites annually.

- AST SpaceMobile's Partnership with Verizon: AST SpaceMobile has partnered with Verizon to provide direct-to-cell satellite connectivity, expanding mobile coverage to underserved areas.

What’s fuelling this growth? The answer lies in the demand coming from everywhere: rapid prototyping and turnaround, the growth of mega-constellations for global coverage, advances in AI-powered analytics on satellite data, and the drive to cut launch and manufacturing costs.

But the overwhelming majority, nearly 80% of small satellites focus on communication, especially global broadband and internet. Earth observation, technology testing, and science missions make up the rest, with remote sensing, disaster monitoring, and geospatial intelligence in escalating demand.

Fig. 1. Communications Take the Lead in Smallsats Launches 2020 Onwards

Miniaturization: Making Satellites Smarter and Cheaper

The rising trend is miniaturization, as satellites shrink from ‘mini’ to ‘micro’, ‘nano’, and even smaller, all becoming compact hubs for data and communication. Smaller size means lighter weight, better energy efficiency, and dramatically lower power requirements.

This shrinking footprint comes with huge cost savings. Small satellites can be up to 90% cheaper to build and launch than classic space hardware. Today, building and deploying a satellite (like those from OneWeb or Rocket Lab) can sometimes be achieved for around $1 million or less, depending on size and mission.

3D printing in small sats industry is also accelerating the gains. Recent advances, like Mitsubishi Electric’s on-orbit 3D-printed antennas or SpaceX and Rocket Lab’s mass-produced lightweight structures, slash manufacturing times, boost strength, cut costs further, and even allow for on-demand production in orbit. Another giant – Boeing has also announced that it has begun 3D printing the structural panels that form the backbone of satellite solar arrays, a step the aerospace giant says will cut production times in half and help it keep pace with demand for faster spacecraft deployment.

Industry leaders including Maxar Technologies, and Northrop Grumman, etc. are also integrating additive manufacturing to enhance satellite performance.

Regional Hotspots: US, China, and the Global Race

The United States, home to major players such as SpaceX, Amazon, Rocket Lab, and Planet Labs, remains well ahead, accounting for over 75% of global small satellite launches, with more than 9,550 out of 12,636 satellites launched worldwide between 2015 and 2024 – as per BryceTech. Strong public-sector backing from agencies like NASA and the Department of Defense underpins this dominance.

Europe is expected to hold its position as the second-largest market for small satellites till 2030. The UK’s OneWeb has already launched over 450 satellites to power its broadband network. As of October 2025, several notable small satellite launches have taken place in Europe, highlighting the region's growing capabilities in space technology.

For instance, the European Space Agency (ESA) is set to launch the HydroGNSS mission, which involves two small satellites. The NAOS satellite, developed by OHB Italia for the Luxembourg Directorate of Defence, was launched aboard a SpaceX Falcon 9 rocket.

A few upcoming launches include – the EU-funded ‘Mauve’ satellite is scheduled for launch in October 2025. Arianespace plans to launch the Sentinel-1D satellite using the Ariane 6 rocket. The Ariane 6 rocket is scheduled for multiple missions in 2025, including launching the MetOp-SG A1/Sentinel-5A satellite. These developments highlight Europe's strategic focus on enhancing its space capabilities through the deployment of small satellites.

Meanwhile, Asia-Pacific is emerging as the fastest-growing region. China, though, is rapidly narrowing the gap, ramping up state and commercial investments, launching dozens of Guowang satellites in 2025 alone, and setting sights on mega-constellation parity. Other APAC countries like India, Japan, etc., are investing significantly in small satellite projects for various applications such as military surveillance, asset tracking, weather predictions, and disaster monitoring.

Is There Still 'Space' in Space?

It won’t be wrong, if we say that the space industry is witnessing a period of rapid transformation, marked by both opportunities and rising challenges.

With launch volumes accelerating, the mounting concern over ‘space debris’, a growing cloud of defunct satellites and fragments, is becoming a serious threat to both current and future missions. In response, global regulators are tightening oversight to prevent orbital overcrowding and ensure safer space operations. Initiatives like ISRO’s ‘Debris-Free Space Missions (DFSM)’ by 2030, the U.S. ‘ORBITS Act’ aimed at strengthening debris management, and Japan’s plan to align international rules for debris removal by 2026 highlight this global regulatory momentum.

At the same time, new technological trends are driving the small satellite boom. The rise of digital twinning for remote industrial sites, dependence on interconnected devices, and the anticipated surge in bandwidth demand from metaverse ecosystems like Meta’s Horizon Worlds by 2032 are fueling the need for enhanced satellite connectivity. These developments are expected to further accelerate small satellite launches, unlocking new opportunities for innovation and data-driven services.

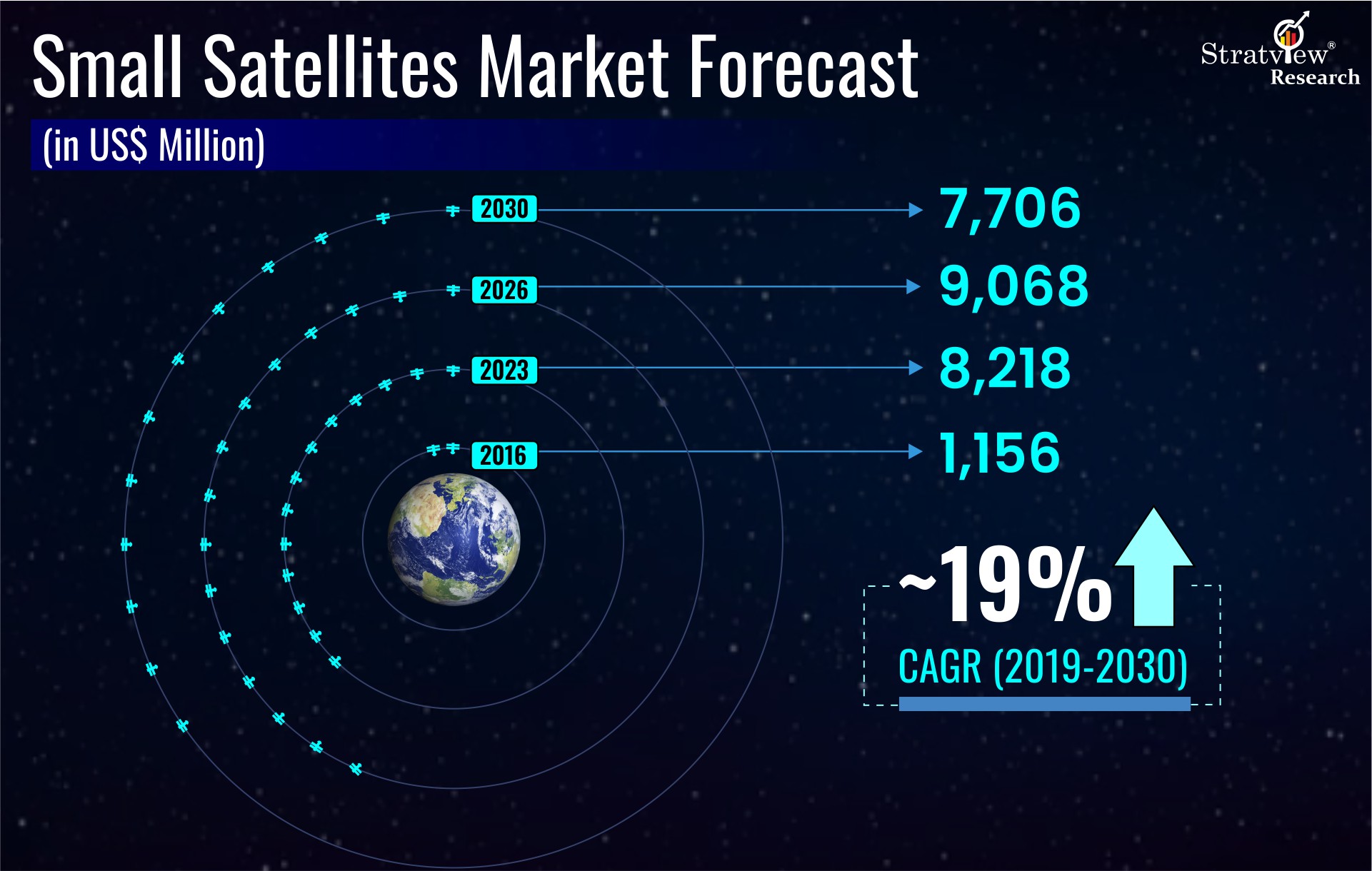

Fig 2. Small Satellites Market Forecast

As innovation continues to redefine what ‘small’ satellites can achieve, the small satellite market is set to hit a ‘big’ inflection point, with small satellites moving from rapid growth to even broader adoption and fierce competition for orbital positions. The global market’s annual value is set to climb from USD 6.8 billion in 2024 to over USD 8.0 billion by 2032, unlocking >USD 63 billion in sales potential for the sector, during the period from 2025 to 2032.

Subscribe to our newsletter

Related Articles:

Small Satellites : Insights From Space, Decisions on Earth

Didn’t find what you were looking for?

Tell us about your requirements

(Our team usually responds within a few hours)