One of the most significant advances in green transport has come from power electronics. While battery capacity and motor output usually hog the spotlight, it is the 'back room' components – power electronics – that are essential for the performance, efficiency, and safety of electric vehicles (EVs). Even with a high-performing battery, a measurable share of system inefficiency originates within the electric drive itself.

As per the U.S. Department of Energy, the electric drive system accounts for roughly 18% of total energy losses in an EV. This directly places power electronics at the center of efficiency optimization, as they ultimately determine how effectively the electric drive system can perform. Even marginal improvements in conversion efficiency can translate directly into measurable gains in range, thermal stability, and overall vehicle economics.

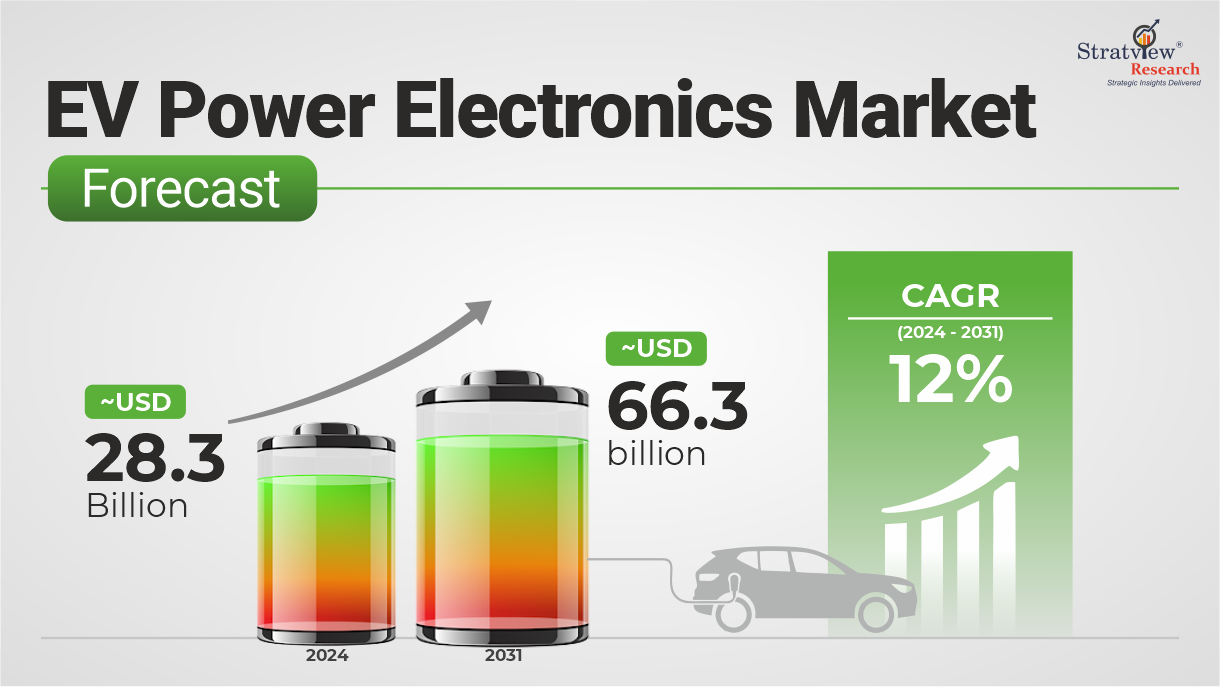

The power electronics industry is undergoing a major transformation as it adapts to the shifting demands of the electric vehicle market. Power Electronics market for Electric Vehicles is projected to scale over twofold by 2031, crossing a $66 billion market value.

Now, the question is: what is driving that expansion? It is certainly being driven by growing EV adoption, but also by a sharp increase in power electronics content per vehicle. While volume growth provides the baseline demand, the acceleration is further pushed by shifts in vehicle architectures, higher voltage platforms, policy support, and advancements in semiconductor technologies.

EV Fleet Expansion Emerging as One of the Key Drivers

Global electric vehicle fleet is expected to cross 240 million mark, growing by a factor of eight or more by 2030, from that of 2022 (excluding 2 and 3 wheelers), as per the International Energy Agency (IEA.org). The same organization also forecasts that the EV sales globally will cross 40 million in 2030.

This surge directly translates into proportional demand for power electronic components, as every EV integrates multiple systems such as inverters, onboard chargers, and DC-DC converters.

Consumer-driven factors are equally influential, range expectations have risen sharply, making efficiency gains in power electronics a direct lever for range improvement. Over the past decade, the average range of a battery electric vehicle (BEV) has expanded from ~135 km in 2014 to nearly 455 kilometers (km) in 2024. This further demands advancements in inverter efficiency and control strategies.

Take the Nissan Leaf, for instance. The best-performing 2014 variant (Leaf S) delivered a range of ~135.2 km, whereas the latest 2026 variant (Leaf Platinum+) now reaches up to ~416.8 km. This ~3× expansion is not just of larger battery capacities but also a shift in power electronics, especially the move from silicon-based to SiC systems.

The increasing adoption of dual-motor configurations (2 inverters), each requiring a dedicated inverter, is thus expanding the role of power electronics, particularly in premium and high-performance EV segments where torque control and drivetrain optimization are critical.

EV models such as the Tesla Model S, Mercedes-Benz EQE/EQS, Kia EV6, Audi e-tron, BMW iX, Volvo XC40/C40 Recharge, etc., deploy two motors, each paired with a dedicated inverter, enabling precise torque vectoring and real-time load optimization.

In 2025, dual-inverter configurations accounted for nearly 60% of EV power electronics adoption, reflecting a clear industry preference for balanced performance and efficiency. By enabling independent control of front and rear motors, this setup enhances traction and real-time torque distribution, making it the go-to architecture for both premium and mid-range EV platforms without significantly increasing system complexity.

BEVs Set to Overtake HEVs After 2027

Hybrid Electric Vehicles (HEVs) have a widespread installed base and represent early adoption across mature automotive markets. Owing to this scale, they remain the largest demand generators of power electronics today. Their dual powertrain architecture, combining internal combustion engines with electric propulsion, requires continuous power flow management between sources, increasing reliance on inverters and DC-DC converters.

Even with relatively smaller battery packs, usually in the range of 1–8 kWh, hybrids demand high-frequency switching and precise control systems to manage energy transitions efficiently.

In 2025, HEVs continued to lead the sector, contributing over $17 billion to the EV power electronics market. However, a significant shift is expected to occur in 2026. Our estimates suggest that from 2026 onward, BEVs will overtake HEVs in terms of market value.

This transition is driven by the deeper integration and higher complexity of power electronics required for pure electric platforms, positioning BEV-related demand as the primary value driver for the industry moving forward.

Think of it this way: as batteries get better, prices drop, and governments push for zero emissions, fully electric cars (BEVs) are going to be the top choice worldwide, especially across Europe and Asia. Because of that, car manufacturers are going to be scrambling for high-end, high-voltage power electronics to keep up with the demand.

Current & Emerging Trends Impacting EV Power Electronics

Emerging material systems and design approaches are impacting EV power electronics significantly, moving the focus from incremental efficiency gains to system-level optimization across size, weight, thermal management, and energy conversion efficiency.

A notable trend is the rapid adoption of silicon carbide (SiC) across EV power electronic systems. Building on the earlier example, the Nissan Ariya shows this industry shift, alongside multiple OEMs transitioning from silicon-based inverters to SiC systems, driven by the need to improve efficiency and reduce system losses. SiC devices offer up to 50% lower switching and conduction losses in certain applications, and inverters made using SiC weigh up to 40% lighter, 30% smaller in size.

Back in 2018, Tesla, Inc. used SiC metal-oxide-semiconductor field-effect transistors (MOSFETs) in an in-house inverter with the launch of Model 3, sourcing devices from STMicroelectronics. This shift enabled a significantly lighter inverter - around 4.8 kg, less than half the weight of comparable silicon-based systems such as those used in Nissan Leaf (~12kgs) and Jaguar I-PACE (>8kgs), highlighting the impact of SiC on power density and system efficiency.

Audi has even found that this technology, especially when paired with 800V systems, can boost efficiency by 60% during normal driving and add about 20 km of extra range just by reducing heat and weight. This trend is also gaining traction in high-performance models from Kia, Hyundai, and Lucid, offering really fast charging and extended range.

To achieve EV potential by squeezing more functionality into a given volume, OEMs are rapidly shifting toward Integrated Drive Units (IDUs), which combine the electric motor, transmission, and inverter into a single, compact housing.

Another innovative application of power electronics is now in the form of wireless charging for EVs. Using resonant inductive coupling, a principle based on Faraday's law of induction, power can be transmitted wirelessly from a charging pad on the ground to a receiver on the vehicle. Power electronics are vital in tuning the resonance between the transmitter and receiver and controlling the power transfer. This technology offers the convenience of cable-free charging and has the potential to be embedded in public infrastructure for seamless charging as the vehicle is parked or even while in motion.

Why the ‘Back Room’ is the Future of the Road

As we move toward a projected USD 66 billion market for EV power electronics by 2031, we are witnessing a fundamental shift in how energy is managed.

The push for fast charging and high-tech features is moving power electronics beyond the motor and into every part of the car's energy system. EVs hitting the mainstream is nothing short of a clear shift toward integrated, high-voltage designs – one that makes power electronics the absolute backbone of vehicle performance and manufacturing scale.

EV battery energy densities are projected to increase significantly over the next few years, with next-generation technologies like solid-state batteries (SSBs) aiming to double current energy levels to over 400–600 Wh/kg by 2026–2030, offering longer ranges and faster charging times. With power densities expected to double in the coming years, the ‘back room’ of the electric drive, comes forward.

All this seems clear, but while the path isn’t without its road-humps. The industry is currently navigating a complex ‘double-edged sword’ caused by global instability.

Geopolitical Roadblocks such as the Russia-Ukraine severely squeezed the supply of Nickel – a core component for high-performance batteries, and Neon gas, which is essential for the lasers used to make the very semiconductors power electronics rely on.

Secondly, the Middle East Tensions in the Red Sea and the Strait of Hormuz have sent shipping costs soaring.

Oil prices topping $100 per barrel actually improve the economic case for EVs. However, the current rerouting of vessels has added 10 to 15+ days to transit times, significantly extending delivery windows for critical batteries and components. These delays between Asia and Europe are straining just-in-time (JIT) manufacturing models across the industry."

Despite these challenges, it’s certain, that vehicle electrification won't be slowing down anytime soon. Automakers are taking more control by focusing on localizing production and moving toward advanced materials like SiC and GaN. By integrating systems like inverters and chargers more tightly, the goal has shifted from just ‘building more’ to ‘managing energy better’.

This move doesn't just boost range of EVs, it builds a much tougher, more resilient ecosystem that can keep the electrification trend going. And, this in turn, pushes the entire power electronics industry to a whole new level.

Authored by Stratview Research. Also published on – www.electronicsweekly.com

Subscribe to our newsletter

Related Articles:

Electric Drive Modules : Advanced Solution for Driving EVS Further

Didn’t find what you were looking for?

Tell us about your requirements

(Our team usually responds within a few hours)