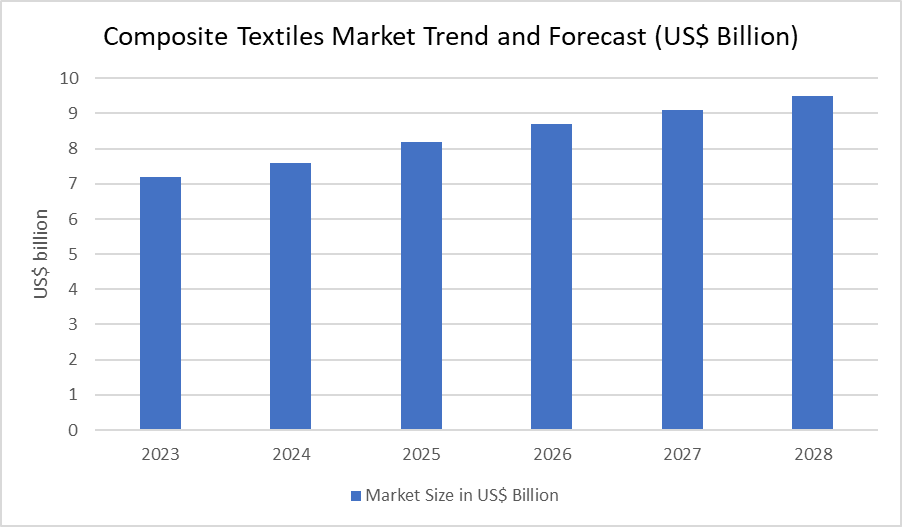

Composite textiles are expected to see demand of about $7.2 billion in 2023, rising to $9.5 billion by 2028, as noted by Stratview Research. While automotive, aerospace, and marine use continues to grow, wind energy and electrical/electronics remain the largest contributors, together generating nearly half of the global demand.

When we hear the word 'textile', the first few words that usually pop into our minds are fabrics, suits, texture, or maybe even our favorite clothing brand. But, the advancement of technology has broadened both the scope and the applications of textiles so much that starting from the circuit board in your mobile phone, to complex parts of an aircraft, everything today is being made using textiles. However, not every textile is capable of offering the flexibility of being used in such a wide range of applications, and hence composite textiles have been the ‘go-to’ material across several industries for quite some time now.

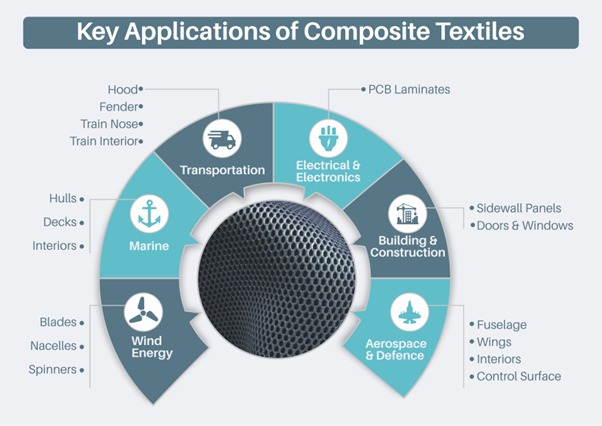

Every Industry that Requires lightweighting, Requires Composites:

Known for their exceptional structural properties combined with their lightweighting capabilities, composite textiles find applications in every industry where durability and lightweighting are the key design requirements. This includes the entire mobility sector because of their common aim of achieving reduced emissions and better fuel efficiency, the wind energy sector, construction, electronics, and many other industries. Listed below are some key applications of composite textiles across these industries.

Fig. 1: Key Applications of Composite Textiles

The industries combinedly have the potential to generate a demand of ~$7.2 bn worth of composite textiles in 2023, which would scale up to $9.5 bn by 2028, according to Stratview Research. Although the focus on increasing the penetration of composites is more in the automotive, aerospace, and marine industries; the biggest share of the demand for composite textiles is generated by the Wind Energy sector, followed by the Electrical and Electronics sector, currently and in the coming years as well. Close to 50% of the current demand for composite textiles in the market is generated by these two industries alone according to an analysis from Stratview Research.

Fig. 2: Composite Textiles Market Trend and Forecast (US$ billion)

Some key driving forces behind the demand emanating from the major industries are:

Increase in the demand for Printed Circuit Boards (PCBs):

Owing to the increased demand for consumer electronics and the surge in the integration of connected technologies into automobile and aerospace, the PCB market itself experienced a growth of roughly 20% in the past two years, from an estimated value of $65.2 bn in 2020 to ~$84.6 bn in 2022. Since PCB laminates are largely made of fibreglass, the corresponding demand for composite textiles will also increase.

Continuous transition towards clean energy:

According to the Global Wind Energy Council (GWEC), the global cumulative wind energy installations would cross the 1,000 GW mark in 2023, which would ultimately lead to the installation of more wind turbines. Since turbine blade manufacturers are now focusing on increasing the length of the blades for enhanced energy output, the demand for the materials would also increase subsequently. In September 2022, China-based Lianyungang Zhongfu Lianzhong Composites Group Co., Ltd. (LZ Blades) rolled out a 123-metre-long wind turbine blade, which the company claimed to be the world’s largest. In 2021, the record was held by the 115.5-meter-long vestas V236-15.0 MW

Increasing penetration of composites in the aerospace industry:

The penetration of composites in aircraft programs has increased from <10% in the Boeing 737, to more than 50% in some of the recent programs like the Boeing 787 and all major aircraft OEMs are following the same trend. Not to overlook the next big innovation in the aerospace industry, i.e., Electric Vertical Take-off and Landing Aircraft (eVTOLs), which would be ~70% composites. In eVTOLs,

Apart from these, the marine and automotive industries will also have a significant role to play on the demand side and it would be safe to say that the composite textiles industry would remain an all-growing industry for a very long time since it has become an inevitable part of the supply chain for so many growing industries.

The Economic and Durable Solution: Glass Fibre

Of the mentioned industries in Table 1, only the aerospace industry has carbon fibre as the dominant material for all its applications, and the requirements of all other industries are well-handled by glass fibre. Though the properties of fibres vary largely depending upon the manufacturer, the process, and the grade of raw material used, a high-level comparison of carbon, aramid, and glass fibre can be presented as follows:

| Fibre | Avg. Fibre Lenghth | Avg. Laminate Strength |

| Carbon | 4,127 | 1,600 |

| Aramid | 2,757 | 1,430 |

| Glass (E Glass) | 3,450 | 1,500 |

Table 1: High-Level Comparison of Different Fibre Types

Despite having the highest fibre strength and laminate strength across all the commercially available fibres, carbon fibre isn’t at the top of the OEMs’ list because of its comparatively high price. The process of producing carbon fibre is also much more intensive than fibreglass and the conversion into prepreg in case of carbon fibre, increases both the cost and the complexity further.

While the average cost of glass fibre usually ranges between $2.2-$3.0/kg, carbon fibre is about 10x costlier. This is the reason why more than 80% of the reinforcements across the industry are done using glass fibre.

Within glass fibre too, there are different grades namely A-glass, C-glass, E-glass, and R, S, or T-glass (R, S, and T signify different manufacturer trademarks). The applications and properties of which, can be described as follows.

| Type | Properties and Primary Applications |

| Alkali Glass ( A-Glass) |

|

| Electrical Glass (E- Glass) |

|

| Chemical Glass ( C- Glass) |

|

| R, S or T Glass |

|

Table 2: Different Types of Fibreglass and Their Properties

Of all the commercially available fibres, E-glass is the most common form of reinforcing fibre used in polymer matrix composites and is available in the form of strands, yarns, and rovings.

It All Comes Down to the Orientation and Interlocking:

Since the properties of composite fabrics depend not only on the selection of fibre, but also on the fibre’s orientation and the way individual fibres in the fabric are held together, the industry exploits this flexibility at the design level to achieve textiles with the desired properties.

Of the available fabric types, woven yarn and multiaxial fabrics currently surpass the demand for other fabric types by a significant margin and own a combined share of >50% in the market. Yarn-based fabrics are generally the preferred choice because they provide better strength per unit weight than rovings. Hence, the fabrics produced are both stronger and lighter than those produced with rovings. Roving-based fabrics on the other hand are comparatively less expensive to produce but can only be used where thicker and heavier laminates are required.

Multiaxials are also witnessing wide adoption owing to factors like the flexibility of achieving more fibre orientations. Additionally, multiaxial fabrics are capable of offering better mechanical properties since the fibres used remain straight and non-crimped. It is because of this flexibility and excellent mechanical properties that multiaxial fabrics are heavily used in the biggest application of composite textiles, i.e. wind turbines.

Crimps in the growth curve and the way ahead:

Although the applications of composite textiles are multi-directional, there are several factors that may slow down the growth pace. High cost of raw materials and the requirement for skilled manpower are among the biggest roadblocks for this industry.

In the past few years, factors like worldwide lockdowns and Russia’s invasion of Ukraine have contributfibed significantly to the increasing price of raw materials for this industry. Apart from these temporary events, there’s also the long-standing issue of increased seaport congestion around the world, which is another challenge for the supply chain.

Furthermore, manufacturing composite fabric requires a skilled workforce. Since the quality of the fabric depends largely on the placement of fibres and laminates, the quality becomes directly proportional to the skill of the individual. The necessary expense behind hiring skilled professionals thus sometimes muddles the profit margins of the suppliers.

Despite these challenges, the increased inclination towards lightweighting across the whole mobility sector, accompanied by large-scale government programs like the target Net Zero Emissions and several others, will act as huge accelerators for this market and will help maintain unprecedented growth in the coming years.

Authored by Stratview Research. Also published on – Textile Technology

Subscribe to our newsletter

Related Articles:

5G Unlocking the True Potential of IoT

Didn’t find what you were looking for?

Tell us about your requirements

(Our team usually responds within a few hours)