404

+1-313-307-4176

Aircraft Surface Treatment Market Report

Aircraft Surface Treatment Market Size, Share, Trend, Forecast, & Competitive Analysis: 2021-2026

Aircraft Surface Treatment Market is Segmented by Aircraft Type (Narrow-Body Aircraft, Wide-Body Aircraft, Regional Aircraft, General Aviation, Military Aircraft, Helicopter, and UAV), by Chemical Type (Cleaners, Deoxidizers and Desumutters, Conversion Coatings, Paint Strippers, and Others), by Treatment Type (Pre-treatment, Chemical Milling, Depaint and Repaint, and Engine Maintenance), by Application Type (Fuselage, Wings, Engine, Landing Gears, and Others), by Substrate Type (Aluminum, Titanium, Steel, and Others), and by Region (North America, Europe, Asia-Pacific, and Rest of The World)

Aircraft components are exposed to harsh environments that may critically damage the surface of the components. Surface treatment plays a pivotal role in surviving these parts from such harsh environments. The purpose of surface treatment is not only to protect aircraft parts from such a challenging environment, but also protect them against oxidation, corrosion, wear, erosion, and fouling. In addition to these, surface treatment reduces energy, reduces product consumption, and reduce chemical waste at the time of coatings. In an aircraft, different types of surface treatments are applied on different substrates. For example, conversion coatings performed using chromate or phosphate materials, are majorly used on the fuselage to prevent the formation of an oxide layer on the surface.

The Aircraft industry roughly holds less than a 15% share of the total surface treatment market. The aircraft surface treatment market flourished at an impressive rate from the past decade till 2018 and got slightly dwindled in 2019 mainly due to B737 Max grounding after two fatal accidents of the aircraft. The impact of the COVID-19 pandemic further deepened the wounds of the industry. As a result of that, the market recorded its biggest-ever plunge of over 20%, shrunk the global market size close to US$ 470 million figure in 2020. Despite such a graver situation faced by the industry, strong industry fundamentals, such as a huge pile of order backlogs and expected revive in air traffic and recovery of aircraft production (especially for short-haul aircraft), are estimated to rejuvenate the demand in the years to come.

Additional noticeable trends that are substantiating the demand are an increasing M&A and rebranding activities at the airlines level, greater need for chemically treated surfaces with excellent durability and longer maintenance cycle, stringent government emission regulations, such as REACH (Registration, Evaluation, Authorization, and Restriction of Chemicals) and Euro Zone Crisis 2012, and rising demand for eco-friendly surface treatment chemicals. Also, lucrative long-term growth of the market is compelling industry trendsetters to increasingly perform strategic alliances with an aim to remain at the driving seat of the market.

Wish to get a free sample? Register Here

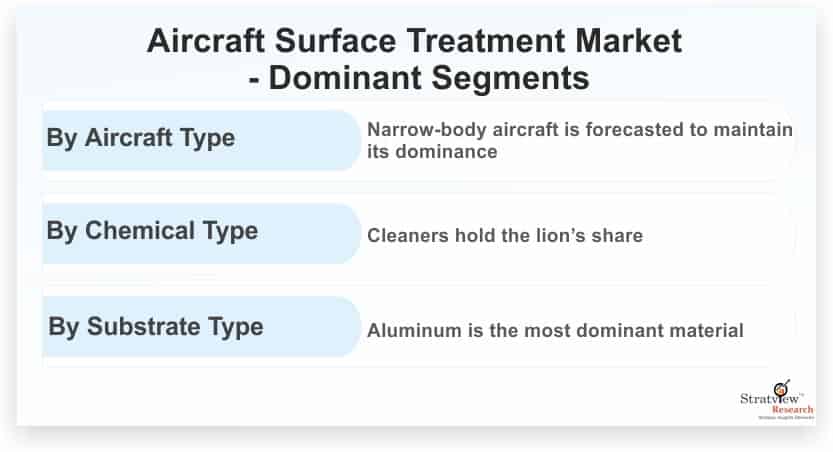

To assist the industry stakeholders in building their profitable strategies efficaciously, the report segments the market in six ways in which aircraft type segmentation (Narrow-Body Aircraft, Wide-Body Aircraft, Regional Aircraft, General Aviation, Military Aircraft, and Helicopter) is exceptionally crucial. Among different aircraft types, narrow-body aircraft is forecasted to maintain its dominance in the market over the next five years, propelled by an expected recovery in the production rate of major aircraft, faster rebound of short-haul aircraft, expected entry of upcoming aircraft, such as COMAC C919; rising aircraft fleet; and higher M&A and re-branding activities in the airline industry.

Aircraft Surface Treatment Market Share by Chemical Type

Analogously to the aircraft types, the report also provides a deep-dive analysis of the different chemicals used for surface treatment. A wide array of surface treatment chemicals including cleaners, deoxidizers and desumutters, conversion coatings, and paint strippers are used for surface treatment out of which cleaners hold the lion’s share and are also likely to grow at the above industry average growth rate by 2026. Cleaners are widely adopted by airframe manufacturers, tier players, as well as airlines in order to prepare the surface for pre-treatment as well as post-treatment.

The relation of surface treatment type with the type of substrates is imperative for the market participants to expedite their growth process. Currently, a wide array of metals including aluminum, steel, nickel, and titanium are used in different aircraft applications based on the performance requirements. Aluminum is by far the most dominant material used in all legacy aircraft with fuselage and wings, the two largest applications, made with aluminum only. However, this trend is precipitously shifting with composite materials and titanium seem the winners in the latest aircraft construction, because of their excellent track record and mechanical properties. Changing dynamics in materials is imprinting a huge impact on the demand for surface treatments as these treatments are preferably performed in metals. In the aircraft surface treatment market, titanium will remain the fast-growing material type in the coming five years, propelled by its exponential use in the newer variants of engines such as LEAP (powering B737 Max, A320neo, and C919) and GE9x (powering B777x).

In terms of region, North America is estimated to maintain its unassailable lead in the global market with the USA being the engine’s propeller. The USA is the manufacturing powerhouse of the aerospace industry, creating a humongous demand for surface treatment chemicals in the country. Canada and Mexico are catching the attention of global companies, driven by their advantages. Airbus’ acquisition of Bombardier’s C-Series invigorated the entire supply chain of the Canadian market, whereas attractive government policies, high proximity to the USA, and low-labor cost are attracting tier players to open their plants in Mexico. However, the maximum long-term growth opportunities continue to lie in Asia-Pacific, particularly in China, Japan, India, and Singapore.

Know which region offers best growth opportunities. Register Here

|

Research Scope |

|

|

Trend & Forecast Period |

2015-2026 |

|

Size in 2026 |

US$ 671.6 million |

|

Regions Covered |

North America, Europe, Asia-Pacific, Rest of the World |

|

Countries Covered |

The US, Canada, Mexico, France, Germany, the UK, Russia, China, Japan, India, Middle East, Latin America and Others |

|

Figures & Tables |

>150 |

|

Customization |

Up to 10% customization available free of cost |

The market is segmented into the following categories:

Want to know the most attractive market segments? Register Here

The supply chain of the market seems quite convoluted with the presence of many stakeholders including raw material suppliers, surface treatment chemicals suppliers, distributors, tier players, aircraft and engine OEMs, MRO companies, and airlines.

Key aircraft surface treatment companies are-

Stratview Research’s voyage towards publishing extremely niche market subjects containing disruptive growth potential continues. This time, we have come up with another such market report on Aircraft Surface Treatment Market, a niche but fast-growing material in the aircraft industry. The report segments and analyzes the market in the most comprehensive manner to provide the different market angles, ensuring thoroughgoing market understanding and future market directions. All the major players are covered during the analysis with their current positioning and market shares. This report provides market intelligence most comprehensively. The report structure has been kept such that it offers maximum business value. It provides critical insights into the market dynamics and will enable strategic decision-making for the existing market players as well as those willing to enter the market.

The following are the key features of the report:

This strategic assessment report, from Stratview Research, is one of the exclusive reports from the shelf of surface treatment family of market reports. The report estimates the short- and long-term repercussions of the COVID-19 pandemic on the aircraft surface treatment market at the global, regional, and country levels. Also, the report provides the possible loss that the industry will register by comparing pre-COVID and post-COVID scenarios. The vital data/information provided in the report can play a crucial role for the market participants and investors in the identification of low-hanging fruits available in the market and formulate growth strategies.

Report Customization Options

With this detailed report, Stratview Research offers one of the following free customization options to our respectable clients:

Company Profiling

Market Segmentation

Competitive Benchmarking

Custom Research: Stratview Research offers custom research services across sectors. In case of any custom research requirement related to market assessment, competitive benchmarking, sourcing and procurement, target screening, and others, please send your inquiry at [email protected].

The report is delivered digitally through our online portal. Buyers receive login credentials from our team to access the report and may update their credentials at any time after the initial login.

Delivery timelines depend on the status of the report:

For the most accurate delivery timeline, please contact us to confirm the current status of the report.

Yes. You may request a complimentary preview of the report through a video conference with our team.

Yes. The scope of the report can be fully customized to align with your specific research objectives and information requirements.

Please contact us at [email protected], and our team will be happy to discuss your requirements and propose a tailored solution.

Yes. Selected sections of the report can be purchased separately based on your requirements. Please contact us at [email protected] to discuss your needs.

Yes, AI can help gather publicly available information, but its outputs are only as reliable as the data it accesses. Stratview Research reports are built using validated data, extensive primary interviews with industry stakeholders, and the expertise of our experienced research team.

Additionally, many critical insights, including market dynamics, competitive intelligence, and industry-specific trends, are not publicly available and therefore cannot be captured through AI alone.

The aircraft surface treatment market is expected to witness an impressive CAGR to reach US$ 671.6 million in 2026.

Henkel AG & Company, KGaA.; Chemetall (BASF SA); PPG Industries, Inc.; Nihon Parkerizing Co., Ltd.; Solvay SA; Socomore, The Surface Company; Quaker Chemical Corporation; Oerlikon Group; and Fokker Technik (GKN Aerospace) are among the key players in the aircraft surface treatment market.

North America is expected to maintain it lead in the aircraft surface treatment market during the forecast period of 2020-2025.

Narrow-body aircraft is expected to remain dominant in the aircraft surface treatment market in the coming years.

WE ACCEPT