404

+1-313-307-4176

Aircraft Fuel Containment Market Growth Analysis | 2019-2024

Aircraft Fuel Containment Market Size, Share, Trends, Dynamics, Forecast, & Growth Analysis: 2019-2024

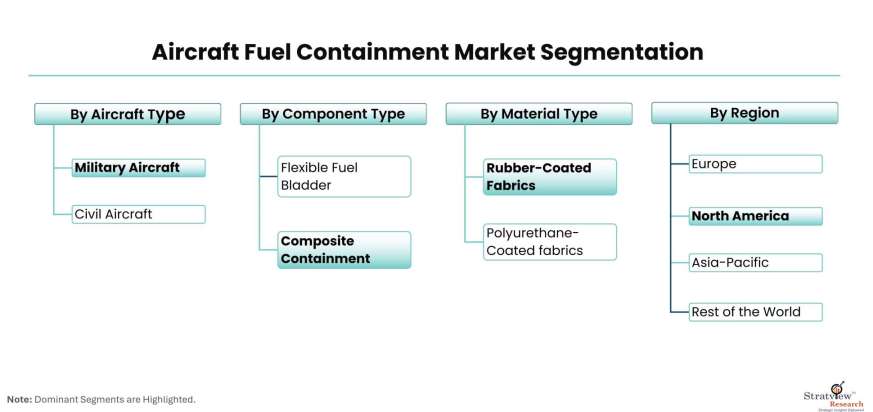

Aircraft Fuel Containment Market is segmented by Aircraft Type (Military Aircraft and Civil Aircraft), by System Type (Rotorcraft System and Fixed Wing System), by Component Type (Composite Containment and Flexible Fuel Bladder), by Material Type (Rubber Coated Fabric, Polyurethane, and Others), by Containment Type (Self Sealing/Ballistic Resistant/Crash Resistant Bladder, Fuel Bladder and Fuel Tank), and by Region (North America, Europe, Asia-Pacific, and Rest of the World).

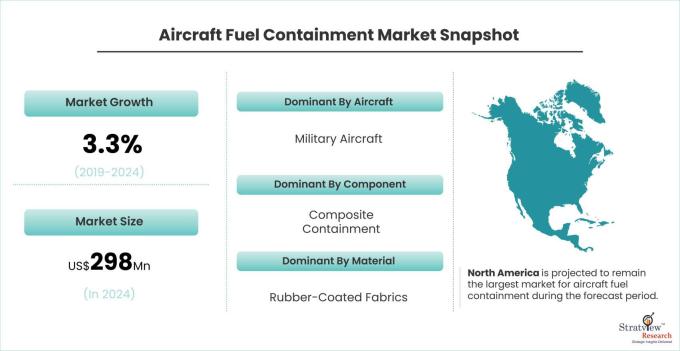

The aircraft fuel containment market is likely to grow at a CAGR of 3.3% during 2019-2024 to reach a value of USD 298 million in 2024.

Want to have a closer look at this report? Click Here

|

Segmentations |

List of Sub-Segments |

Segments with High Growth Opportunity |

|

Deployment Model Type Analysis |

Military Aircraft and Civil Aircraft |

Military aircraft are likely to remain the dominant segment of the market during the forecast period. |

|

Component Type Analysis |

Composite Containment and Flexible Fuel Bladder |

Composite containment is projected to remain the most dominant component type in the aircraft fuel containment market over the next five years. |

|

Material Type Analysis |

Rubber Coated Fabric, Polyurethane, and Others |

Rubber-coated fabrics are likely to remain the dominant segment of the market during the forecast period. |

|

Regional Analysis |

North America, Europe, Asia-Pacific, and Rest of the World |

North America is projected to remain the largest market for aircraft fuel containment during the forecast period. |

The aircraft fuel containment market is segmented based on the aircraft type as military aircraft and civil aircraft. Military aircraft are likely to remain the dominant segment of the market during the forecast period. Both military fixed-wing and rotorcraft are likely to generate sizeable opportunities for market participants in the coming five years. There is a growing interest among defense communities in the development of efficient fuel containment that substantially mitigates aircraft vulnerability.

Based on the component type, the market is segmented as composite containment and flexible fuel bladder. Composite containment is projected to remain the most dominant component type in the market over the next five years. Rubber-coated fabric is the major type of material used in such containments. The demand for flexible fuel bladders is largely driven by the military aircraft segment, which generally has such types of fuel containment. Meggitt, Safran SA, and GKN Aerospace are leading players, supplying fuel bladders.

Based on the material type, the market is segmented as rubber-coated fabric, polyurethane-coated fabrics, and others. Excellent resistance to petroleum fluids and chemicals, superior heat resistance, and high strength-to-weight ratio are some key factors that have led to the mass adoption of rubber-coated fabrics in the aircraft fuel containment market. ContiTech and Colmant Coated Fabrics are leading suppliers of rubber-coated fabrics for aircraft fuel containments.

In terms of regions, North America is projected to remain the largest market for aircraft fuel containment during the forecast period, largely driven by massive demand from defense organizations such as the U.S. Department of Defense (DoD) and Defense Logistics Agency (DLA). Asia-Pacific currently represents a relatively small market opportunity; however, is subjected to grow at a handsome rate in the coming years, largely driven by China. China is projected to add a growth propulsion engine to the global demand for fuel containments.

Get the full scope of the report. Register Here

The supply chain of this market comprises raw material suppliers, aircraft fuel containment manufacturers, airframers, and end-users.

Some of the key players in the aircraft fuel containment market are:

Strategic collaborations, the formation of long-term contracts, and the development of highly efficient and lightweight products are the key strategies adopted by major players to gain a competitive edge in the market.

Note: The above list does not necessarily include all the top players in the market.

Are you the leading player in this market? We would love to include your name. Write to us at [email protected]

This report provides market intelligence in the most comprehensive way. The report structure has been kept such that it offers maximum business value. It provides critical insights into market dynamics and will enable strategic decision-making for existing market players as well as those willing to enter the market. The following are the key features of the report:

This report studies the market covering a period of 12 years of trend and forecast. The report provides detailed insights into the market dynamics to enable informed business decision-making and growth strategy formulation based on the opportunities present in the market.

The aircraft fuel containment market is segmented in the following ways.

By Aircraft Type

By System Type

By Component Type

By Material Type

By Containment Type

By Region:

Click Here, to learn the market segmentation details.

With this detailed report, Stratview Research offers one of the following free customization options to our respectable clients:

Company Profiling

Market Segmentation

Competitive Benchmarking

Custom Research: Stratview Research offers custom research services across sectors. In case of any custom research requirement related to market assessment, competitive benchmarking, sourcing and procurement, target screening, and others, please send your inquiry to [email protected].

Aircraft fuel containment refers to the design and implementation of systems and structures within an aircraft to prevent the uncontrolled release of fuel in the event of a rupture or damage to fuel tanks. These systems are crucial for enhancing safety by minimizing the risk of fuel-related fires or explosions during emergencies, such as crashes or accidents. Aircraft fuel containment measures typically include the use of robust tank materials, fuel tank liners, and structural reinforcements to ensure that fuel remains securely contained within designated compartments, protecting both the aircraft and its occupants from the potential hazards associated with fuel leakage.

Increasing aircraft deliveries to support rising air passenger traffic, rising military expenditure, and increasing demand for self-sealing fuel bladders are the major factors that are escalating the demand for fuel containments in the aircraft industry.

The market is marked by a handful of players, who are currently enjoying their healthy shares. These players own extraordinary capabilities in the market, securing their vanguard in the market. The market is registering further consolidation because of a fair number of mergers & acquisitions over a period of time. All the major players that hold a large chunk of the market, gained expertise in the market by acquiring core fuel containment manufacturers. For instance, Meggitt gained expertise by acquiring Engineered Fabrics Corporation, which originally gained the expertise from Goodyear. Similarly, Amfuel gained expertise from Uniroyal, which originally gained it from US Rubber. In the past few years, there has been a series of acquisitions including the acquisition of the advanced composite business of Cobham plc by Meggitt PLC, the acquisition of GKN Aerospace by Melrose Industries, and the acquisition of Zodiac Aerospace by Safran SA.

Want to have a closer look at this market report? Click Here

The report is delivered digitally through our online portal. Buyers receive login credentials from our team to access the report and may update their credentials at any time after the initial login.

Delivery timelines depend on the status of the report:

For the most accurate delivery timeline, please contact us to confirm the current status of the report.

Yes. You may request a complimentary preview of the report through a video conference with our team.

Yes. The scope of the report can be fully customized to align with your specific research objectives and information requirements.

Please contact us at [email protected], and our team will be happy to discuss your requirements and propose a tailored solution.

Yes. Selected sections of the report can be purchased separately based on your requirements. Please contact us at [email protected] to discuss your needs.

Yes, AI can help gather publicly available information, but its outputs are only as reliable as the data it accesses. Stratview Research reports are built using validated data, extensive primary interviews with industry stakeholders, and the expertise of our experienced research team.

Additionally, many critical insights, including market dynamics, competitive intelligence, and industry-specific trends, are not publicly available and therefore cannot be captured through AI alone.

Aircraft fuel containment refers to the design and implementation of systems and structures within an aircraft to prevent the uncontrolled release of fuel in the event of a rupture or damage to fuel tanks. These systems are crucial for enhancing safety by minimizing the risk of fuel-related fires or explosions during emergencies, such as crashes or accidents. Aircraft fuel containment measures typically include the use of robust tank materials, fuel tank liners, and structural reinforcements to ensure that fuel remains securely contained within designated compartments, protecting both the aircraft and its occupants from the potential hazards associated with fuel leakage.

The aircraft fuel containment market is likely to grow at a CAGR of 3.3% during 2019-2024.

The aircraft fuel containment market is likely to reach a value of USD 298 million in 2024.

Meggitt PLC, Safran SA, GKN Aerospace, Marshall Aerospace, Amfuel, and Floats & Fuel Cell Inc. are among the top players in the market.

Composite containment is expected to remain the most dominant component type in the market over the next five years.

North America is expected to remain the largest market during the forecast period.

Military aircraft is expected to remain dominant in the market in the coming years.

WE ACCEPT