404

+1-313-307-4176

Geomembrane Market Analysis | 2022-2028

Geomembrane Market Size, Share, Trends, Dynamics, Forecast, & Growth Analysis: 2022-2028

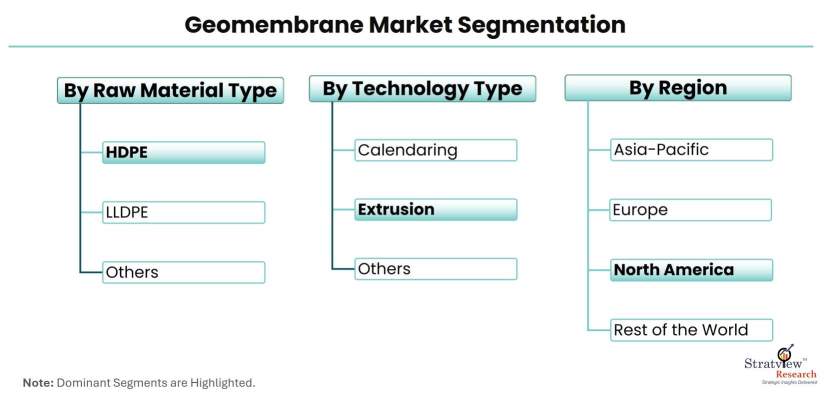

Geomembrane Market is segmented by Raw Material Type (High-Density Polyethylene (HDPE), Linear Low-Density Polyethylene (LLDPE), Polyvinyl Chloride (PVC), Ethylene Propylene Diene Monomer (EPDM) and Polypropylene), by Technology Type (Extrusion, Calendaring and Others), by Application Type (Mining, Water Management, Agriculture, Tunnel Liners & Civil Engineering, Marine and Waste Management High-Density), and by Region (North America [The USA, Canada, and Mexico], Europe [Germany, France, The UK, Russia, and Rest of Europe], Asia-Pacific [China, Japan, India, South Korea, and Rest of Asia-Pacific], and Rest of the World [Brazil, Saudi Arabia, Israel, and Others]).

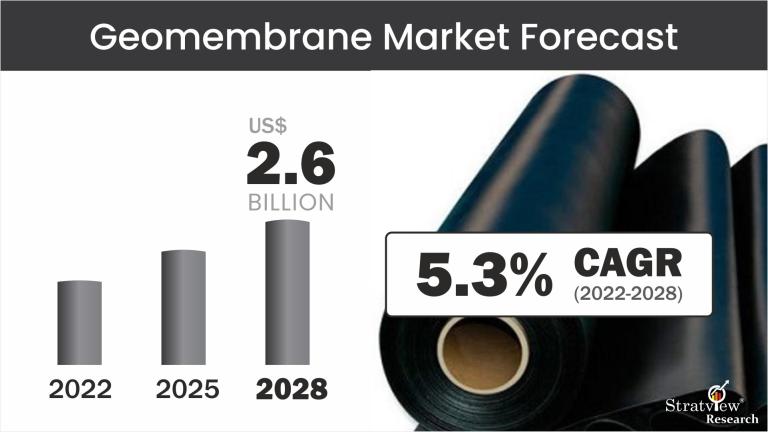

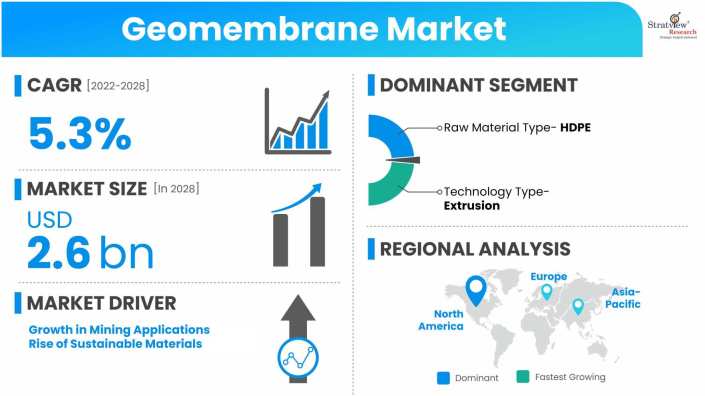

The geomembrane market was estimated at USD 1.9 billion in 2021 and is likely to grow at a CAGR of 5.3% during 2022-2028 to reach USD 2.6 billion in 2028.

Want to know more about the market scope? Register Here

Geomembranes are synthetic materials used in the construction industry to control the flow of fluids and gases in a variety of applications, such as the lining of ponds, landfills, reservoirs, canals, and tunnels. The geomembrane market has grown significantly over the years due to its high performance, durability, and cost-effectiveness.

These trends demonstrate how geomembranes are becoming more and more significant in resource management, environmental protection, and sustainable development in a variety of industries.

Want to have a closer look at this market report? Click Here

Here are some recent examples of investments in the geomembrane industry:

These examples highlight the significant investments being made by companies in the geomembrane industry to expand their production capacity, acquire new capabilities, and strengthen their market position.

Some of the key players in the geomembrane market include

Note: The above list does not necessarily include all the top players in the market.

Are you the leading player in this market? We would love to include your name. Write to us at [email protected]

|

Segmentations |

List of Sub-Segments |

Dominant and Fastest-Growing Segments |

|

Raw Material Type Analysis |

High-Density Polyethylene (HDPE), Linear Low-Density Polyethylene (LLDPE), Polyvinyl Chloride (PVC), Ethylene Propylene Diene Monomer (EPDM) and Polypropylene |

HDPE is the most commonly used raw material in the geomembrane market, accounting for the largest share of the market. |

|

Technology Type Analysis |

Extrusion, Calendaring and Others |

The extrusion segment is likely to account for the largest market share. |

|

Regional Analysis |

North America [The USA, Canada, and Mexico], Europe [Germany, France, The UK, Russia, and Rest of Europe], Asia-Pacific [China, Japan, India, South Korea, and Rest of Asia-Pacific], and Rest of the World [Brazil, Saudi Arabia, Israel, and Others] |

North America accounted for the largest market share. |

"The HDPE segment accounted for the largest market share."

The market is bifurcated into HDPE, LLDPE, PVC, EPDM and Polypropylene. HDPE is the most commonly used raw material in the geomembrane market, accounting for the largest share of the market. HDPE geomembranes offer excellent chemical and UV resistance, high tensile strength, and durability, making them ideal for a wide range of applications such as waste containment, mining, and water management.

EPDM geomembranes are used in applications where high flexibility and low permeability are required. EPDM geomembranes are commonly used in pond liners, decorative water features, and irrigation canals.

"The extrusion segment is likely to account for the largest market share."

The geomembrane market can also be segmented based on the technology used in their manufacturing process. The main technologies used for producing geomembrane include extrusion, calendaring, and others. Extrusion is the most common technology used in the production of geomembranes. In this process, the raw material is melted and extruded through a die to form a continuous sheet.

HDPE and LLDPE geomembranes are mostly produced using the extrusion process. Extrusion offers excellent control over the thickness and width of the geomembrane and can produce geomembranes with thicknesses ranging from 0.5 mm to 3 mm. In calendaring technology, the raw material is passed between two or more rollers to create a continuous sheet of the required thickness.

The calendaring process is used mainly for producing PVC and PP geomembranes, which have a lower melting point than HDPE and LLDPE. Other technologies used in the production of geomembranes include spread coating, lamination, and hot-air welding. Spread coating technology involves applying a liquid or semi-liquid material onto a substrate using a spreader or roller.

"North America accounted for the largest market share."

In terms of regions, North America is a significant market for geomembranes, driven by stringent regulations for waste management and the construction of new landfill sites. The United States is the largest market for geomembranes in this region, accounting for the majority of the demand. Canada is also a significant market for geomembranes, with a growing demand for these products in mining and water management applications.

The European geomembrane market is driven by the increasing demand for sustainable waste management practices and the rising focus on environmental protection. Germany, France, and the UK are the largest markets in Europe, with a significant demand for geomembranes in the construction and mining sectors.

Know the high-growth countries in this report. Register Here

This strategic assessment report, from Stratview Research, provides a comprehensive analysis that reflects today’s geomembrane market realities and future market possibilities for the forecast period of 2022 to 2028. After a continuous interest in our geomembrane market report from the industry stakeholders, we have tried to further accentuate our research scope to the geomembrane market to provide the most crystal-clear picture of the market. The report segments and analyses the market in the most detailed manner to provide a panoramic view of the market. The vital data/information provided in the report can play a crucial role for the market participants as well as investors in the identification of the low-hanging fruits available in the market as well as to formulate the growth strategies to expedite their growth process.

This report offers high-quality insights and is the outcome of a detailed research methodology comprising extensive secondary research, rigorous primary interviews with industry stakeholders, and validation and triangulation with Stratview Research’s internal database and statistical tools. More than 1000 authenticated secondary sources, such as company annual reports, fact books, press releases, journals, investor presentations, white papers, patents, and articles, have been leveraged to gather the data. We conducted more than 15 detailed primary interviews with the market players across the value chain in all four regions and industry experts to obtain both qualitative and quantitative insights.

This report provides market intelligence in the most comprehensive way. The report structure has been kept such that it offers maximum business value. It provides critical insights into market dynamics and will enable strategic decision-making for existing market players as well as those willing to enter the market. The following are the key features of the report:

This report studies the market, covering a period of 12 years of trends and forecasts. The report provides detailed insights into the market dynamics to enable informed business decision-making and growth strategy formulation based on the opportunities present in the market.

The geomembrane market is segmented into the following categories:

By Raw Material Type

By Technology Type

By Application Type

By Region

Click Here, to learn the market segmentation details.

With this detailed report, Stratview Research offers one of the following free customization options to our respectable clients:

Company Profiling

Competitive Benchmarking

Custom Research: Stratview Research offers custom research services across sectors. In case of any custom research requirement related to market assessment, competitive benchmarking, sourcing and procurement, target screening, and others, please send your inquiry to [email protected]

The report is delivered digitally through our online portal. Buyers receive login credentials from our team to access the report and may update their credentials at any time after the initial login.

Delivery timelines depend on the status of the report:

For the most accurate delivery timeline, please contact us to confirm the current status of the report.

Yes. You may request a complimentary preview of the report through a video conference with our team.

Yes. The scope of the report can be fully customized to align with your specific research objectives and information requirements.

Please contact us at [email protected], and our team will be happy to discuss your requirements and propose a tailored solution.

Yes. Selected sections of the report can be purchased separately based on your requirements. Please contact us at [email protected] to discuss your needs.

Yes, AI can help gather publicly available information, but its outputs are only as reliable as the data it accesses. Stratview Research reports are built using validated data, extensive primary interviews with industry stakeholders, and the expertise of our experienced research team.

Additionally, many critical insights, including market dynamics, competitive intelligence, and industry-specific trends, are not publicly available and therefore cannot be captured through AI alone.

Geomembranes are synthetic materials used in the construction industry to control the flow of fluids and gases in a variety of applications such as the lining of ponds, landfills, reservoirs, canals, and tunnels. The geomembrane market has grown significantly over the years due to its high performance, durability, and cost-effectiveness.

The geomembrane market was estimated at USD 1.9 billion in 2021.

The forecasted value of the geomembrane market is expected to be USD 2.6 billion in 2028.

The geomembrane market is likely to grow at a CAGR of 5.3% during 2022-2028.

Some of the key players in the market include Agru America Inc., Anhui Huifeng, New Synthetic Material Co., Atarfil SL, Carlisle Syntec Inc., Colorado Lining International Inc., Environmental Protection Inc., Firestone Building Products Company, LLC, Geofabrics, GSE Environmental LLC, Naue GmbH, Nilex Inc., Officine Maccaferri Spa, Plastika Kritis S.A., Rowad, Solmax International Inc.

The growth of the geomembrane market is driven by factors such as the increasing demand for water management solutions, the rising need for environmental protection, and the growing mining activities in developing countries.

HDPE is the most commonly used raw material in the geomembrane market, accounting for the largest share of the market. HDPE geomembranes offer excellent chemical and UV resistance, high tensile strength, and durability, making them ideal for a wide range of applications such as waste containment, mining, and water management.

North America is a significant market for geomembranes, driven by stringent regulations for waste management and the construction of new landfill sites.

WE ACCEPT