404

+1-313-307-4176

Digital Health Market Growth Analysis | 2023-2028

Digital Health Market Size, Share, Trends, Dynamics, Forecast, & Growth Analysis - 2023-2028

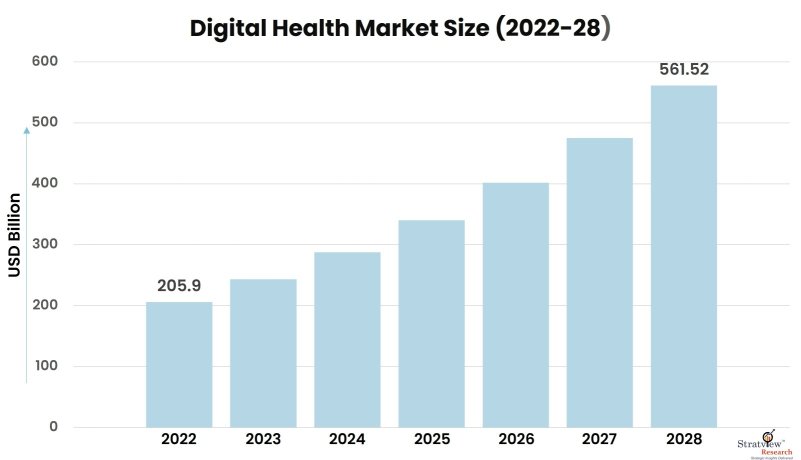

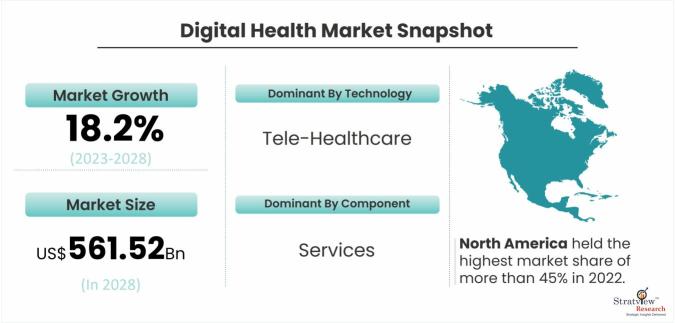

The digital health market was estimated at USD 205.9 billion in 2022 and is likely to grow at a CAGR of 18.2% during 2023-2028 to reach USD 561.52 billion in 2028.

Want to know more about the market scope? Register Here

What is digital health?

Digital health is defined as the incorporation of electronic communication and information technology used in managing different healthcare processes for people’s health and well-being. This concept is an umbrella term for mHealth apps, wearable devices, electronic health records, electronic medical records, telemedicine, telehealth, etc.

According to the Data Protection Report, 2021, there was a 73% increase in healthcare cybercrime and data breaches in 2020, exposing 12 billion units of healthcare information.

Smartphones or mobile phones have evolved from communication and entertainment devices to health and wellness monitoring devices. According to the Pew Research Center, by 2021, 97.0% of U.S. residents will own smartphones.

Companies are developing innovative mobile applications to track daily activities such as well-being, exercise, nutrition, and development, thereby providing excellent medical services and comfort to customers.

Besides, users can acquire data from mobile applications about clinical requests, plan arrangements, track interviews, store their medical care data, and track and request their clinical solutions.

Additionally, For the past 5 to 6 years, the Internet of Things (IoT) has become one of the most prominent digital platforms in healthcare. IoT has evolved to the point where it is significantly transforming the healthcare sector by facilitating various activities such as efficient tracking of staff, patients, and inventories; optimizing drug prescription; ensuring availability of critical medical equipment; and addressing chronic diseases.

The evolution and deployment of big data play a significant part in enabling an uninterrupted tailored digital experience by assisting a service provider in optimizing resources and time to provide superior healthcare services.

COVID-19 IMPACT

The COVID-19 pandemic has radically altered people's daily lives, workplaces, and the surrounding environment. According to the market forecast for digital health, the current estimate for 2028 is expected to be higher than pre-COVID-19 estimates. The COVID-19 outbreak has had little impact on the growth of the market because the COVID-19 lockdown enabled the widespread adoption of digital health. The pandemic has compelled the development of safer and more efficient methods of constructing offices and homes.

|

Digital Health Market Report Highlights |

|

|

Market Size in 2022 |

USD 205.9 billion |

|

Market Size in 2028 |

USD 561.52 billion |

|

Market Growth (2023-2028) |

18.2% CAGR |

|

Base Year of Study |

2022 |

|

Trend Period |

2017-2021 |

|

Forecast Period |

2023-2028 |

The growth of the digital health market is primarily driven by

Furthermore, digital health policies are ambiguous and differ among countries and regions. Increasing smartphone penetration, improved internet connectivity with the introduction of 4G/5G, advancement in healthcare IT infrastructure, growing need to minimize healthcare costs, rising prevalence of chronic diseases, and increased access to virtual care.

The increased usage of the internet and smart gadgets in the healthcare sector is raising cybersecurity concerns. The number of incidences of hacking and accessing personal information via linked and smart devices has significantly increased.

Because of data security issues regarding healthcare information, governments, healthcare organizations, and experts are hesitant to implement digital health solutions on a bigger and national scale.

Want to have a closer look at this market report? Click Here.

The World Health Organization (WHO) has recognized the potential of digital health solutions to improve healthcare access and outcomes and has provided some statistics on the digital health market. Here are some key stats on the digital health market from the WHO:

Mobile Health (mHealth): The WHO reports that more than 325,000 mobile health apps are available in app stores, with around 3.4 billion smartphone users globally. mHealth technologies provide healthcare information and services, remote patient monitoring, and appointment reminders.

Telemedicine: According to the WHO, telemedicine can help to overcome geographical barriers, increase access to care, and reduce the cost of healthcare. Telemedicine services have been increasingly used during the COVID-19 pandemic, and the WHO has reported that telemedicine consultations have increased by up to 500% in some countries.

Electronic Health Records (EHRs): The WHO recognizes the importance of EHRs in improving healthcare outcomes and reducing medical errors. EHRs enable the sharing of patient data between healthcare providers and can help to ensure that patients receive the right care at the right time.

Digital Health for Universal Health Coverage (UHC): The WHO has identified digital health as a key enabler for achieving universal health coverage. Digital health solutions can help to improve healthcare access and quality, reduce healthcare costs, and promote health equity.

Overall, the WHO recognizes the potential of digital health solutions to transform healthcare and improve health outcomes, and supports the adoption of these technologies to achieve universal health coverage.

The tele-healthcare segment is projected to maintain its dominance by owning more than 35% of the market share in 2022.

The market is segmented as tele-healthcare, mHealth, health analytics, and digital health systems. It is owing to the increasing geriatric population, growing prevalence of chronic diseases, improving accessibility to the internet, and absence of skilled healthcare professionals.

The market is segmented into hardware, software, and services. The services segment is expected to remain the most dominant in the market over the forecast period owing more than 45% share in 2022 due to the growing demand for remote patient monitoring, synchronous services, and asynchronous services.

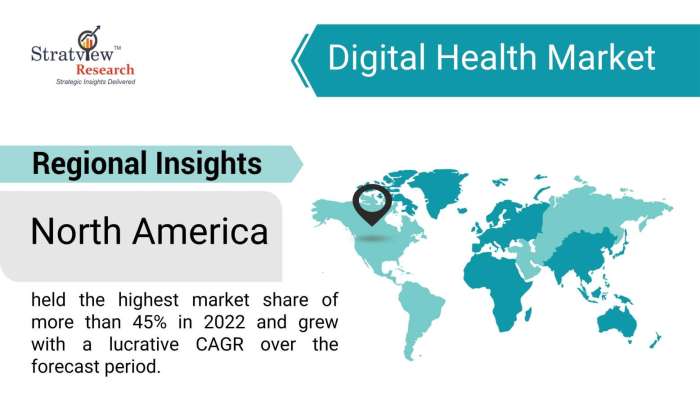

North America held the highest market share of more than 45% in 2021 and grew with a lucrative CAGR over the forecast period, owing to a well-developed healthcare infrastructure, huge healthcare expenditure, high adoption of advanced technology, and the presence of a tech-savvy population.

Know the high-growth countries in this report. Register Here.

Critical Questions Answered in the Report

This report studies the market covering a period of 12 years of trend and forecast. The report provides detailed insights into the market dynamics to enable informed business decision-making and growth strategy formulation based on the opportunities present in the market.

The market is segmented into the following categories.

By Technology Type

By Component Type

By Region

Click Here, to learn the market segmentation details.

Key players operating in the market are-

This report provides intelligence in the most comprehensive way. The report structure has been kept such that it offers maximum business value. It provides critical insights into the dynamics and will enable strategic decision-making for the existing players as well as those willing to enter the market.

What Deliverables Will You Get in this Report?

|

Key questions this report answers |

Relevant contents in the report |

|

How big is the sales opportunity? |

In-depth Analysis of the Digital Health Market |

|

How lucrative is the future? |

Market forecast and trend data and emerging trends |

|

Which regions offer the best sales opportunities? |

Global, regional, and country-level historical data and forecasts |

|

Which are the most attractive market segments? |

Market Segment Analysis and Forecast |

|

Which are the top players and their market positioning? |

Competitive landscape analysis, Market share analysis |

|

How complex is the business environment? |

Porter’s five forces analysis, PEST analysis, Life cycle analysis |

|

What are the factors affecting the market? |

Drivers & challenges |

|

Will I get the information on my specific requirements? |

10% free customization |

The target audience of the market includes-

This report offers high-quality insights and is the outcome of a detailed research methodology comprising extensive secondary research, rigorous primary interviews with industry stakeholders, and validation and triangulation with Stratview Research’s internal database and statistical tools.

More than 1,000 authenticated secondary sources, such as company annual reports, fact books, press releases, journals, investor presentations, white papers, patents, and articles have been leveraged to gather the data.

We conducted more than 10 detailed primary interviews with companies across the value chain in all four regions and with industry experts to obtain both qualitative and quantitative insights.

With this detailed report, Stratview Research offers one of the following free customization options to our respectable clients:

Company Profiling

Market Segmentation

Competitive Benchmarking

Custom Research: Stratview Research offers custom research services across sectors. In case of any custom research requirement related to market assessment, competitive benchmarking, sourcing and procurement, target screening, and others, please send your inquiry to [email protected].

July 2022, Facebook co-founder's VC firm eyes digital health tech and fintech for the investment. It is also looking to invest in logistics and supply chains, helping industries to scale up digitization.

In July 2022, Altera Digital Health signed a new agreement with SingHealth to enhance healthcare delivery, The continued partnership will support SingHealth in streamlining its clinical workflows to enhance care coordination.

The report is delivered digitally through our online portal. Buyers receive login credentials from our team to access the report and may update their credentials at any time after the initial login.

Delivery timelines depend on the status of the report:

For the most accurate delivery timeline, please contact us to confirm the current status of the report.

Yes. You may request a complimentary preview of the report through a video conference with our team.

Yes. The scope of the report can be fully customized to align with your specific research objectives and information requirements.

Please contact us at [email protected], and our team will be happy to discuss your requirements and propose a tailored solution.

Yes. Selected sections of the report can be purchased separately based on your requirements. Please contact us at [email protected] to discuss your needs.

Yes, AI can help gather publicly available information, but its outputs are only as reliable as the data it accesses. Stratview Research reports are built using validated data, extensive primary interviews with industry stakeholders, and the expertise of our experienced research team.

Additionally, many critical insights, including market dynamics, competitive intelligence, and industry-specific trends, are not publicly available and therefore cannot be captured through AI alone.

The digital health market was estimated at USD 205.9 billion in 2022.

The digital health market is likely to reach USD 561.52 billion in 2028.

The digital health market is likely to grow at a CAGR of 18.2% during 2023-2028.

Digital health is defined as the incorporation of electronic communication and information technology used in managing different healthcare processes for people’s health and wellbeing. This concept is an umbrella term for mHealth apps, wearable devices, electronic health records, electronic medical records, telemedicine, and telehealth, etc.

AdvancedMD Inc., Allscripts Healthcare Solutions Inc., Biotelemetry Inc., iHealth Lab Inc., McKesson Corporation, Koninklijke Philips N.V., AT & T, Cerner Corporation, Cisco Systems. are the key players in the market.

Rising smartphone or mobile phone penetration & integration of advanced technologies, such as the internet of things (IoT) & artificial intelligence (AI)., Advancing healthcare IT infrastructure., Increasing demand for remote patient monitoring services.

The study period of the market is 2017-2028.

The tele-healthcare segment is projected to maintain its dominance by owning more than 35% of the market share in 2022.

WE ACCEPT